December FOMC Preview:

- It’s widely anticipated that the FOMC will accelerate its QE taper, looking to end asset purchases by the end of 1Q’22.

- The release a new Summary of Economic Projections (SEP) will have markets scrutinizing the ‘dot plot’ for clues for when the first rate hike will arrive in 2022.

- We’ll discuss how markets may react to the December Federal Reserve rate decision starting at 13:45 EST/18:45 GMT. You can join live by watching the stream at the top of this note.

Market Expecting a Hawkish Fed

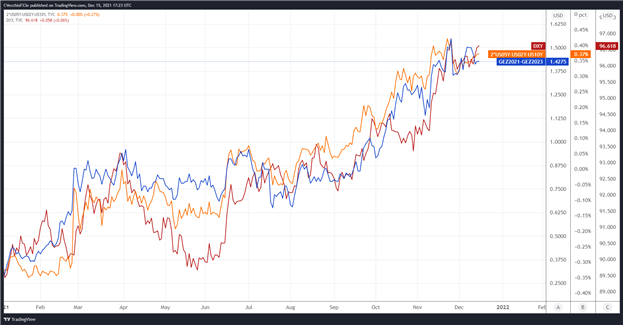

Per Eurodollar spreads, there are 142.75-bps of rate hikes discounted through the end of 2023 while the 2s5s10s butterfly is just off of its widest spread since the Fed taper talk began in June (and its widest spread of all of 2021). Ahead of the December Fed meeting, rates markets are effectively pricing in a 71% chance of five 25-bps rate hikes over the next two years – not significantly changed from prior to Thanksgiving, when Fed Chair Jerome Powell’s more hawkish commentary (retiring the term ‘transitory’ from the Fed’s inflation lexicon) emerged.

EURODOLLAR FUTURES CONTRACT SPREAD (NOVEMBER 2021-DECEMBER 2023) [BLUE], US 2S5S10S BUTTERFLY [ORANGE], DXY INDEX [RED]: DAILY CHART (JANUARY 2021 TO DECEMBER 2021) (CHART 1)

In order to achieve such a rate lift off, the Federal Reserve will likely need to begin rate hikes by mid-2022. Consistent with comments made by Fed Chair Powell as well as incoming Fed Vice Chair Lael Brainard, it seems more likely than not that the FOMC will announce an accelerated timeline to taper its QE program, increasing the rate of tapering from $15B/month to $30B/month beginning in January 2022. This would end the Fed’s QE program in March 2022, allowing for the first 25-bps rate hike by June 2022.

Taper and Rate Hike Timeline

Considering that the tone by Fed Chair Powell has become notably more hawkish in recent weeks, it is interesting that markets have not become more aggressive in their rate expectations. In a sense, the market has been doing the work for the Fed, already discounting the hawkish pivot for several weeks now.

- November 2021 = taper targets announced, reduction by $15B/month beginning immediately from $120B in asset purchases in October to $105B in asset purchases

- December 2021 = $90B in asset purchases

- January 2022 = $60B in asset purchases

- February 2022 = $30B in asset purchases

- March 2022 = $0B in asset purchases

- April through June 2022 = window opens for first 25-bps rate hike

Herein lies the wrinkle for today: rates markets are pricing in over two hikes for 2022 and nearly four hikes for 2023. But if the Fed’s ‘dot plot’ only shows one rate hike for 2022, regardless of the tone and narrative deployed by Fed Chair Powell at his press conference, this may constitute a dovish outcome for markets. There is thus a high bar for the Fed to meet if today’s meeting is going to be hawkish in the aftermath.

We’ll discuss how markets may react to the December Federal Reserve rate decision starting at 13:45 EST/18:45 GMT. You can join live by watching the stream at the top of this note.

Read more: Weekly Fundamental US Dollar Forecast: Will Fed Increase QE Taper?

--- Written by Christopher Vecchio, CFA, Senior Strategist