Talking Points:

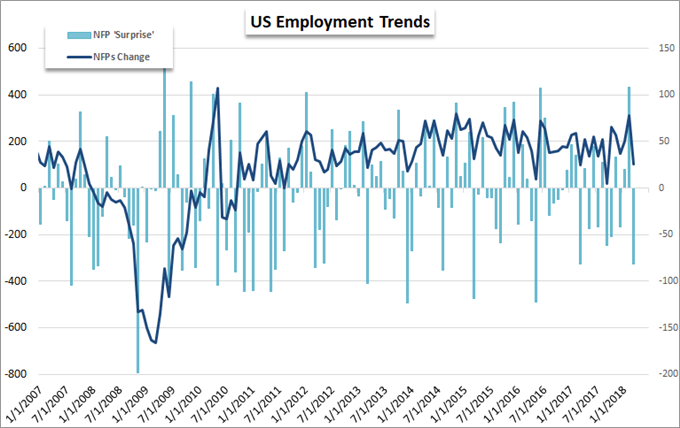

- April US NFPs is top event risk for Friday, with forecasts for 193,000 jobs added and slide in the jobless rate to 4.0%

- Given years of general improvement and numbed enthusiasm, more impact would follow a 'miss' than a 'beat'

- For the Dollar, the multi-week rally will hang on average hourly earnings while the Dow and risk trends register payrolls

Are you trading the Dollar or US-based markets? Keep tabs on how NFPs alters risk trends and monetary policy expectations for the Fed. Join us as we cover the employment release live. Sign up on the DailyFX Webinar Calendar.

Why NFPs are Important this Go Around

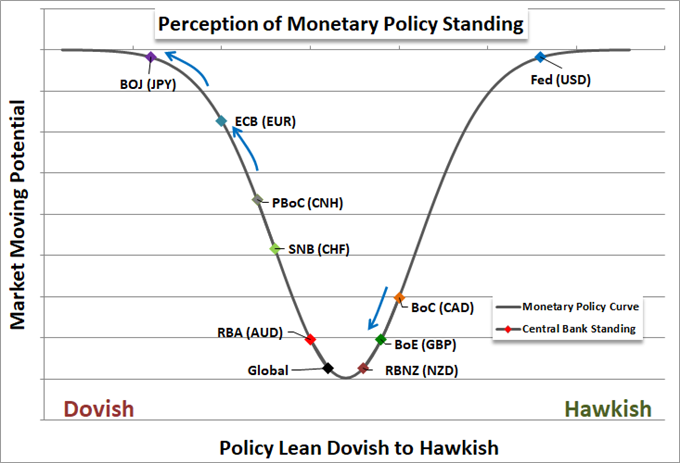

With any data or piece of event risk, to establish how much market-moving potential it has; we need to establish why - or even if - it matters. For the monthly US jobs report, there are the natural considerations for traditional economic activity. However, we have registered very little connection between growth projections and a particular payrolls report, much less see it drill all the way down to produce a definitive capital market or Dollar move through that venue. Far more capable a conduit between this set of data and systemic market moves are monetary policy and general risks trends. Both of these themes will likely register with the April statistics along with a general bias derived from the recent rally from the US Dollar. Following the Fed's hold earlier this week along with its modest adjustments on growth and inflation expectations, there is a finer point on the debate over four, three or less total hikes in 2018. Yet, it is the notable downgrade in ECB, BoE and BoJ monetary policies that truly have leveraged the US currency to its recent performance.

Dollar is Watching for Any Cracks in a Hawkish Facade

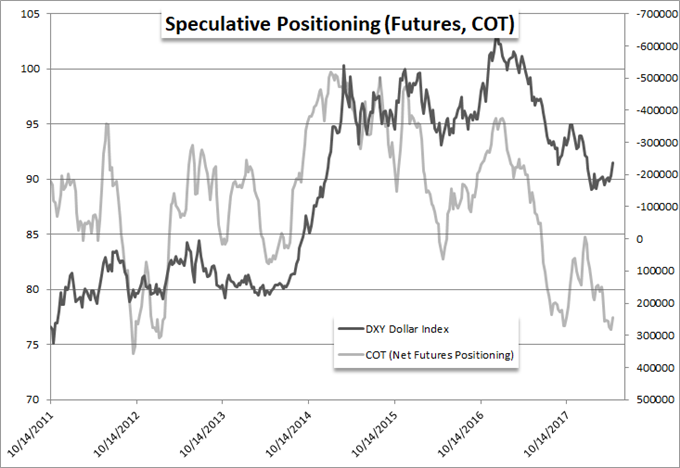

There are different aspects and implications in these April labor statistics from which the currency and capital markets will draw from. For the Dollar, the still-fledgling reversal is likely split between a natural unwind of a heavy short position by the market and a revived appreciation for the unique monetary policy position the Fed currently occupies. Looking to the CFTC's net speculative futures positioning data, the market has just these past few weeks started to back off its heaveist net short holdings on the Greenback in five years. The is a deep well from which to draw, but there needs to be some degree of fundamental motivation to keep it moving. Turning the focus back on established imbalances in central bank bearings can offer that drive. The actual Fed decision on Wednesday did little to acclerate or decelerate the pace of tightening moving forward between a softening of rhetoric surrounding growth and a more optimistic tone on inflation pressures.

That said, there is presently debate between three or four total hikes that will be accumulated in 2018. Adding weight to a fourth hike can help sustain the currency's climb. That said, the true weight comes should the data disappoint. After three weeks of productive climb, there is now a short-term 'overbought' reading behind the currency. Practically-speaking, even if the Fed's course cools to a three-hike-in-2018 pace, it would still far outstrip any of its predecessors. That said, 2017 proved that this is not about what the current policy imbalance or even the fully-priced forecast carries. Rather, the course is set by the rise or fall in expectations. As such, if there is a downshift in the labor data; the Dollar can be put into a position of quick retreat. This can arise from a miss in net payrolls or unexpected uptick in the jobless rate, but the inflation element in wage growth is really where the pressure rests. If there is a dimming in the data though, it is unlikely to systemically change the outlook for employment statistic and the Dollar. A wavering therefore should not be immediately registered as a reversal.

The S&P 500 Will Focus First and Foremost on Payrolls

Just as with the Dollar, it is easier to disappoint US equity indices than it is to beat their inherent expectations. While there has been limited enthusiasm in price action over the past weeks - and even months - there is still a hefty premium behind the market's current standing following literal years of complacent yield reach. The sharp drop in February with volatility and range since has stood as a signal that a passive bid is no longer status quo. A strong jobs report could bolster growth expectations, but does that necessarily fill in the optimistic pricing behind the US equities as a speculative 'risk' champion? It is unlikely. That said, a miss can draw greater attention to either the moderate pace of growth set moving forward. As we focus on the data, make sure to appreciate the status of the market benchmarks in question. Both the S&P 500 and Dow are holding just above medium-term support, and their respective 200-day simple moving averages are within reach of Thursday's close. If fact, for the Dow, we have run 465 trading days with spot above the 200-day SMA - the longest stretch in over 30 years. We discuss the NFPs but keep the focus on unique circumstances with market conditions in today's Quick Take Strategy Vido..

To receive John’s analysis directly via email, please SIGN UP HERE.