Talking Points:

- Much of the Dollar's moves over the past months has been based on the Fed's monetary policy standings relative to its peers

- Another short-term driver that has eased back in influence is a more complex relationship through the currency's 'risk' standings

- Perhaps the most long-lasting, systemic and overlooked consideration for the Greenback is the risk of further credit downgrade

Retail traders are more focused on short-term opportunities rather than long-term trends. See how retail traders are positioned in the most liquid Dollar based pairs such as EUR/USD, GBP/USD and USD/JPY on the DailyFX Sentiment Page.

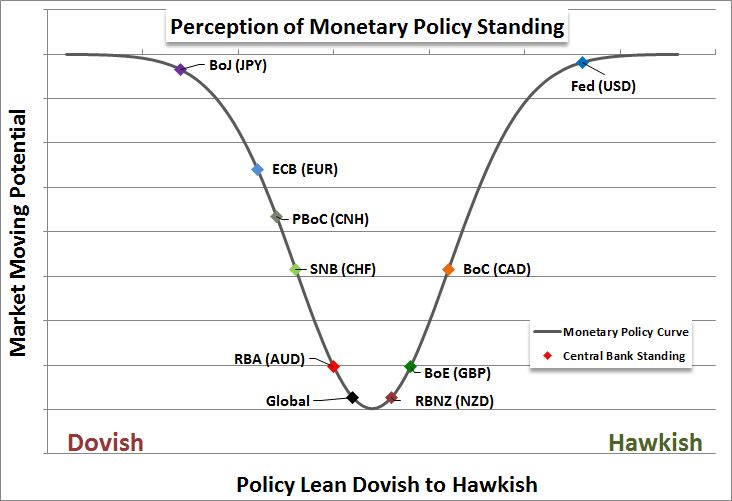

Over the past few weeks, the Dollar made a dramatic move to reverse one of the most prominent trends of 2017 - its own tumble. The late October break through the ICE Dollar Index's 94 'neckline' was a major technical development for those that watch for chart patterns. And yet, that effort has since completely fallen apart; leaving conviction for neither recovery or reinforced tumble. The motivation for this charge was typical fundamental fare for recent months and years. Relative monetary policy is one of the most proactive and frequent course determinants for the Dollar. That said, it is not the easy read as so many make it out to be as current rates are not as critical as relative rate forecasts. On that front, we are operating with efforts of express transparency and speculation in nuance rhetoric. This theme will continue to provide volatility and even trend to the Dollar, but its long-term implications are somewhat dubious.

Another shorter-term factor for the Dollar is the currency's safe haven status. As the world's most liquid currency backing the largest economy, the Dollar defaults to absolute safety when panic seizes the market. Yet here again are issues for engagement. Risk trends have been mired in complacency for months which drains conviction and thereby trend. In this vague situation, the Dollar can be treated like a high yield currency amid the Fed's policy regime which would in turn make it prone to slide should risk trends falter. Alternatively, the safety feature won't kick on in earnest unless we witnessed a full scale unwind in global investments. Naturally, the US benchmark earns its roles with very explicit appeal, but the situation itself creates confusion.

With the proper prompting either or both of these themes could provide the Dollar with a strong charge. In an assessment of extremes on both accounts, the currency would more likely fare very well. Yet, there are issues threatening to trouble the Greenback - and over the longer-term specifically. One of the most troubling - and overlooked - threats is the possible reduction of the United States' credit quality. Following news that the US House of Representatives this past session passed its version of the tax reform, a full adoption at these requests would translate into a large increase in the country's deficit. That financial prolificacy would likely raise the concern of credit companies. Standard & Poor's has already marred the United States' pristine credit rating, but all three (including Fitch and Moody's) have negative oulook fot the US's financial and fiscal house. If course settings for higher debts in the US leads the credit leaders to further cut the United States' sovereign debt level, the impact would be a systemic threat to the Greenback. The S&P's downgrade back in 2011 was tolerated as it was billed as a one-off. Traders and Investors should keep tabs on the markets with these considerations in mind. We discuss this and more in the DailyFX Quick Take Videos.

To receive John’s analysis directly via email, please SIGN UP HERE