Talking Points:

- Extreme accommodation through monetary policy helped to promote risk appetite alongside more virtuous economic growth

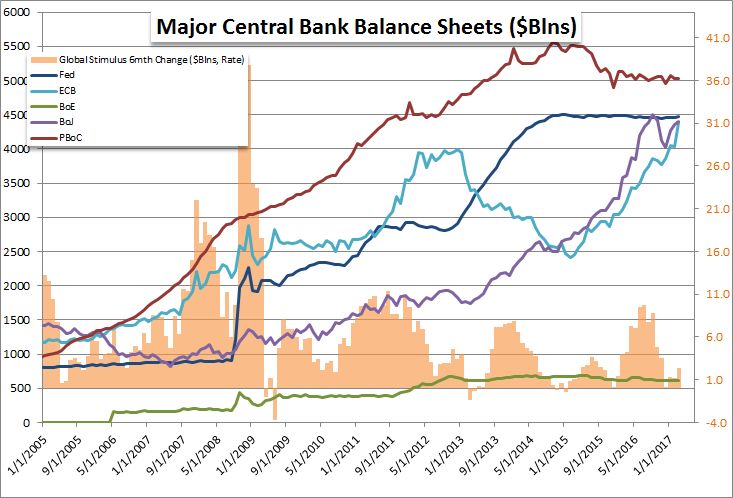

- While the Fed's rumination of a plan to work off its $4.5 Tln holdings grabbed attention, others have started as well

- As with rates, relative balance sheet adjustment can offer FX opportunity; but it can also redefine broad risk trends

See how retail traders are positioning in the majors using the DailyFX SSI readings on the sentiment page.

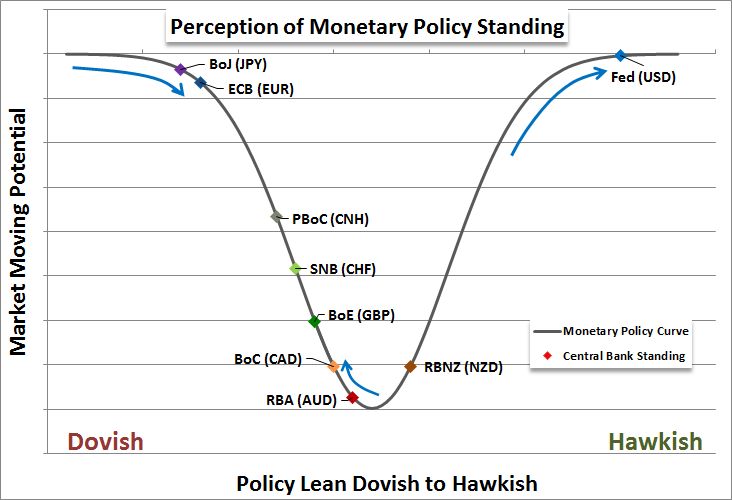

Monetary policy lost much of its overwhelming influence in the years between the Great Financial Crisis and through the opening half of 2015. Yet, this fundamental theme may cycle back to the forefront in the weeks and months ahead as the conversation changes. The discussion around central banks' foray into the market is changing. Previously, the amplitude for the market was found in relative engagement: a growing disparity between dovish and hawkish bearings amongst the majors. That yields massive rallies for the Yen crosses from 2012 to 2015, an impressive rally for the Dollar from 2014 to 2015 and collapse for the Euro from 2014 to 2015. While there will remain motivation to rise and fall at the advantage/disadvantage of counterparts moving forward, that is not worth the true amplitude will originate.

The last impressive move in the scales of monetary policy arguably comes from EUR/USD. For the ECB, late to the game with quantitative easing, the early warning of a stimulus program promoted a sharp decline for the shared currency starting in mid-2014. The same anticipation at the other end of the spectrum motivated the Greenback to rally as the promise of hikes set bulls out to get ahead of the wave. Yet, by the time the ECB implemented it QE program and the Fed secured its first hike; the pair had relegated itself to a broad range. Having hit extremes, the gaps were narrowing and opportunities fading. With other central banks banking off their extreme drive to QE-their-way-to-recovery coming to an end, all shifted to a neutral stance at basement level rates. Yet, in this collective position, we incurred a much more prolific reality whereby a global pursuit of return translated into extreme risk taking.

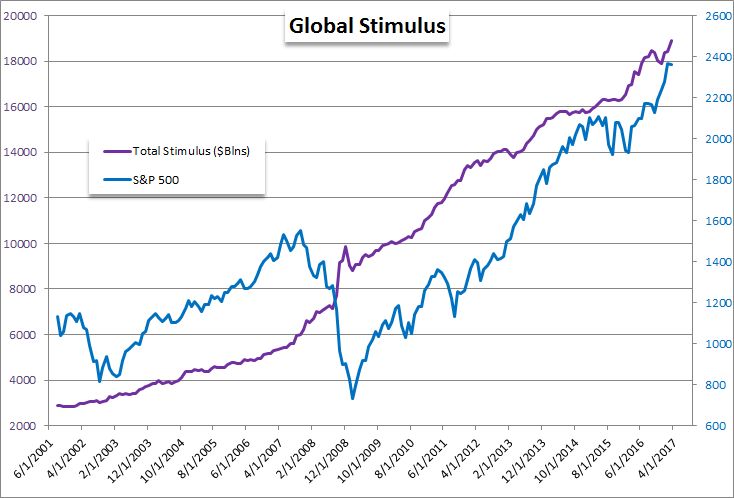

There was little choice by investors over the years other than to expose themselves to greater risk. Whether using notional leverage or moving into riskier assets, the absolute absence of meaningful yield meant market participants had to to accept ever greater risk for even meager returns. That seemed an acceptable trade off with volatility deflated in the market. Yet, that stability was established through the precarious and ultimately limited support of central banks. The monetary policy authorities couldn't keep playing the role of unlimited buyer and provide the capital gains necessary to offset the lack of income/dividend/yield. And, that eventual moderation seems to be at hand. Though a slow change, it will be an enormous one for the global financial system and will lead to considerable movement. We discuss why we should be more mindful of global monetary policy in this weekend Trading Video.

To receive John’s analysis directly via email, please SIGN UP HERE