S&P 500, Nasdaq 100, Dollar, EURUSD and USDJPY Talking Points

- The Trade Perspective: S&P 500 Bearish Below 4,000; AUDJPY Bearish Below 90; EURUSD Bullish Above 1.0650

- The rally from the S&P 500 and other risk-leaning assets through the end of last week stalled out to start Monday with fundamentals offering a ready-threat

- EURUSD and USDJPY are threatening reversal, but Dollar-favorable growth and rate forecasts may be throttling the move – Fed speakers and US data may break the balance

A Critical Point to Lose the Speculative Thread

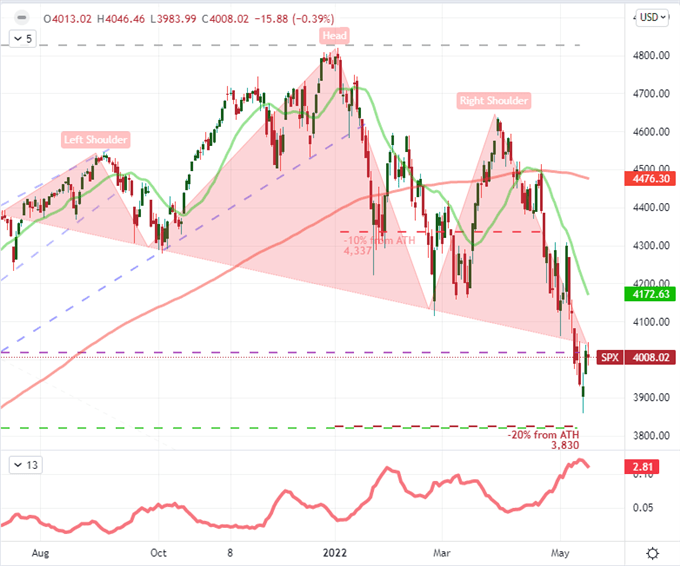

There was a strong charge of hope among the wayward bullish rank through the end of this past week, but the speculative charge looks to be falling apart before conviction could gain any significant foothold. Fundamentally, it would be a reach to rouse a serious run into a full-blown bullish leg. There is certainly room for relief around the worst of expectations in growth, inflation and interest rate projections; but there isn’t a full-blown turn in these trends nor has the market fully flushed its conviction. That makes us much more likely to experience temporary rallies but not genuine trends. That same struggle was made manifest in one of my favorite, imperfect singular measures of risk: the S&P 500. On the back of Friday’s 2.4 percent rally – putting distance between spot and the dread of an official ‘bear market’ (3,830 on my chart) – Monday presented a stall out with a -0.4 percent slip that has reflected struggle at the ‘neckline’ of the head-and-shoulders pattern we broke just over a week ago. Chop higher is possible, but I believe conviction is more likely to build a head of steam if bulls take over the yoke.

Chart of S&P 500 with 20 and 200-Day SMAs and 10-Day ATR as Percentage of Price (Daily)

Chart Created on Tradingview Platform

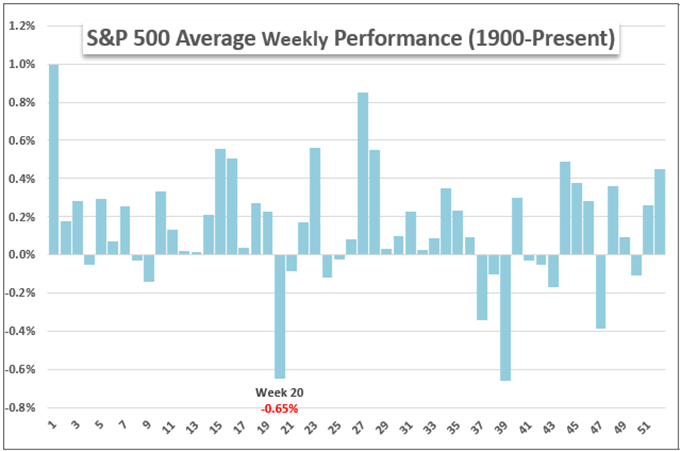

While the technical picture of ‘risk’ is loaded and fundamentals present a distinct skew in bears’ favor, there is also a statistical consideration to add into the mix. We are currently in he 20th week of the trading year, and history suggests that there may be some serious weight associated to this period. Looking back to 1900, the S&P 500 has averaged a remarkable -0.65 percent loss through this particular time frame. That may not seem like a lot, but averaged out over such a long time frame, it is a serious deviation from the norm and the second worst week of the calendar year. I don’t take statistics at face value because there are always unique circumstances to each new iteration; but in this case, the technicals and fundamentals don’t exactly suggest a strong counterpoint to the average.

Chart of Average Weekly Performance Through Calendar Year for S&P 500

Chart Created by John Kicklighter

What’s Moving the Markets This Week

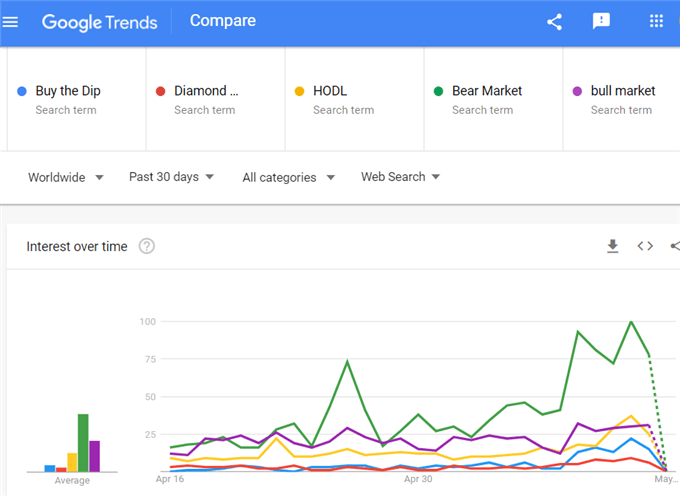

Sentiment isn’t always just an ‘ends’ in itself. It can also be the ‘means’ to its own destination. It does seem that the markets are of a particularly dour disposition where the negative is metabolized far more readily than any positives. I am particularly mindful of the designation of a ‘bear market’ itself of the benchmarks that carry greater weight in the financial system. The Nasdaq 100 slipped into the technical designation two months ago, but the broader S&P 500 and value-based Dow Jones Industrial Average have held back from the quicksand thus far. That said, if the S&P 500 were to slide below 3,830, it is not hard to appreciate the significant deterioration in confidence that would come with that troubling milestone ping-ponged across the headlines. The markets are on constant watch for the threat as if evidenced by search habits across the world, and so should we be vigilant.

Google Trends Traffic for Key Trading Terms

Calendar Created by John Kicklighter

In the more traditional veins of fundamentals, the fear around inflation and monetary policy never really dissipated; but it seemed to be overridden by a more pressing matter. Through scheduled and unscheduled means, the opening session of this week managed to present a uniformly troubling view of the economic forecast. It began in China where the run of April (industrial production, retail sales, unemployment, fixed asset investment) all managed to significantly disappoint versus expectations. From the second largest single economy in the world to one of the largest collective economies, the European Commission’s Spring update lowered its 2022 growth expectations by 1.3 percentage points to 2.7 percent – and even that seems generous relative to other projections. And then there is the US, where former Fed Chairman Ben Bernanke warned about the risks of stagflation amid a critique of the US central bank’s slow response to inflation.

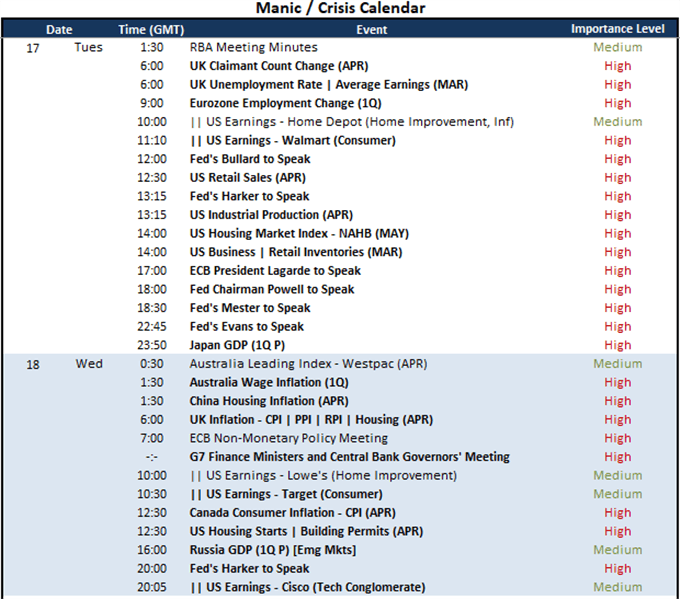

Economic Calendar of Major Event Risk

Calendar Created by John Kicklighter

Interest Rate Expectations and the Markets that Reflect Them

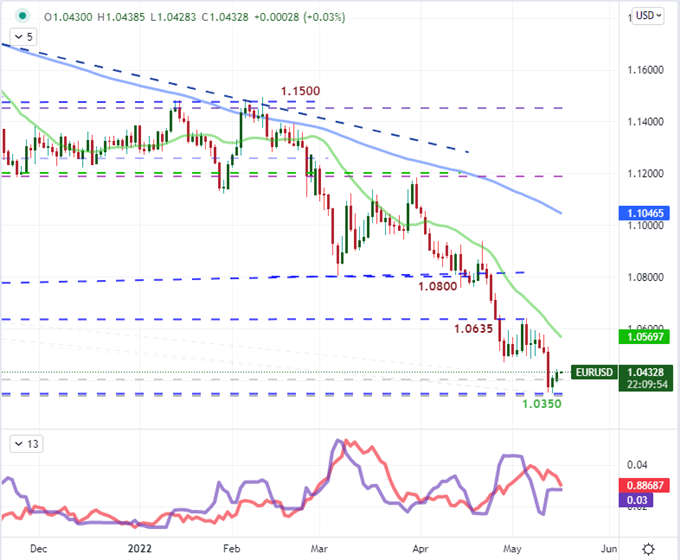

I believe the serious downgrade in growth forecasts is something the market will continue to digest fully for some time, but that doesn’t mean we will be caught up on the matter with full disregard to other influences. Particularly for economic activity, the US docket’s run of retail sales, industrial production and housing sector health will give macro milestone while corporate earnings from Walmart and Home Depot will give a forecast from key players in the economy. Alternatively, monetary policy seems like it may pick up the torch for volatility. In particular, there are a run of key Fed speakers on tap later today including Fed Chairman Powell, Bullard, Mester, Evans and Harker. I doubt this group is moving forward without an objective to shape market expectations. Another high level central bank speaker to take note of is ECB President Largarde who speaks just an hour before for Powell. With EURUSD offering a weak bounce thus far from the tentative two-decade double bottom with the January 2017 low, there is a lot at stake in this pair.

Chart of EURUSD with 20 SMA, 8-Day Range and 8-Day ATR (Daily)

Chart Created on Tradingview Platform

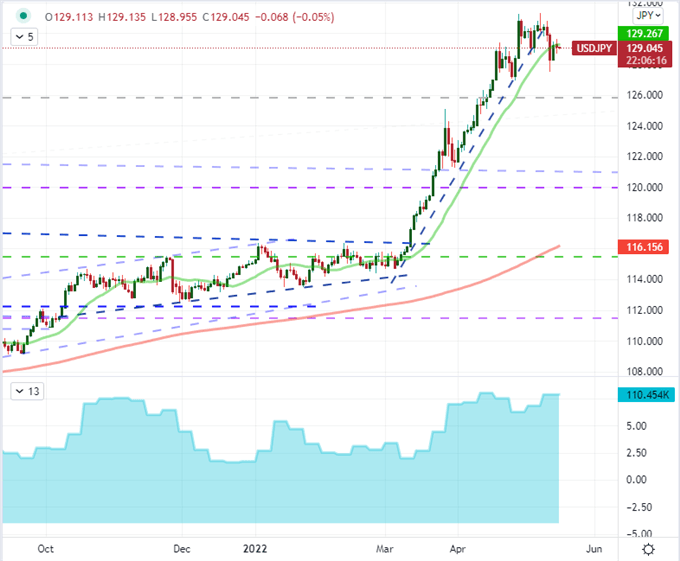

Generally speaking, the outlook for monetary policy and growth favors the Dollar over the Euro through the intermediate future; but there is a significant discount to the point where it seems their economic projections seem on completely opposite courses. That is highly improbable and seems to open this pair up to relief rallies spurred by a furthering of the message from the ECB that the first rate hike is in the near future. For another Dollar-based pair, USDJPY, there seems to be a concerted effort to keep the prevailing winds blowing. The pair slipped below its 20-day simple moving average for the first time in 48 trading days last week as the pressure on risk trends cut into the carry trade appeal the Yen crosses traditionally represent. Yet, with BOJ Governor Kuroda reiterated the importance of supporting the economy with ‘powerful monetary policy’ easing. Whether he intends this to be a currency lever or not, the pressure is there. That said, if risk appetite continues to deteriorate more broadly moving forward; it can and will eventually override the appeal of a slowly building carry trade.

Chart of USDJPY with 20 and 200-Day SMAs and Net Spec Futures Positioning (Daily)

Chart Created on Tradingview Platform