SPY S&P 500 ETF, Fed Forecast, Dollar and USDJPY Talking Points

- US factor inflation hit a record high but the true update on monetary policy this past session was the concerted messaging from FOMC members

- Even the most dovish members of 2021 are warning of possible accelerated rate hikes which raises my expectations for a March rate hike sharply

- A S&P 500 and risk asset retreat on a hawkish shift is to be expected, but the Dollar’s extended slide is creating confusion – though USDJPY may be the outlier

A Risk Trend Correction That is As Much a Range Move as a Fundamental Shift

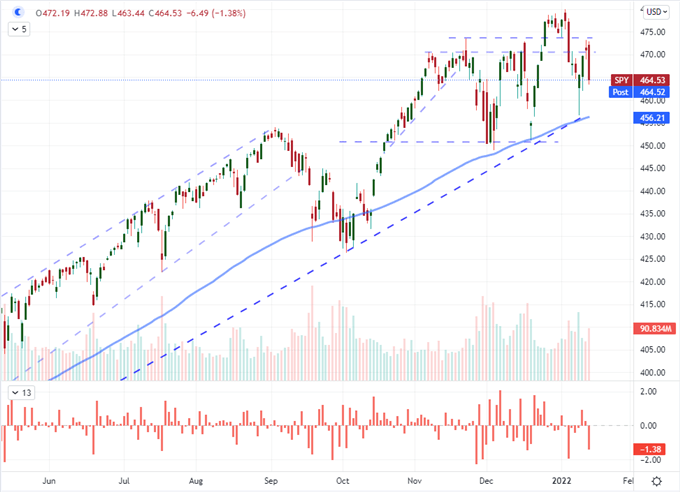

Risk appetite seems to have fallen apart before we had to seriously contemplate any serious technical developments. That may surprise those that are incessant bulls; but for everyone else, this was a natural ebb for a market unwilling to commit to systemic trends, bullish or bearish. There is fundamental justification to follow this latest swoon in capital markets, but I would argue that even the exceptionally hawkish US rate forecast is subordinate to conditions whereby avoidance of a full escalation or unwinding of exposure is preferrable. Looking to the balance of performance in benchmark ‘risk assets’ heading into Friday trade, there may be a strong correlation in the retreat, but there is just as reliable technical congestion to lower the technical ‘cost’ of the about face. While there was a retreat in rest-of-world equities (VEU ETF), emerging market assets (EEM ETF), junk bonds (HYG ETF) and carry pairs; the most noteworthy move in my books was the S&P 500’s reversal. The SPY SPDR ETF of the index dropped -1.4 percent to hold up a ‘shoulder line’ resistance and is still well within the range down to support on a channel that is approximately two years in the making.

Chart of SPY S&P 500 ETF with 100-Day SMA and Volume (Daily)

Chart Created on Tradingview Platform

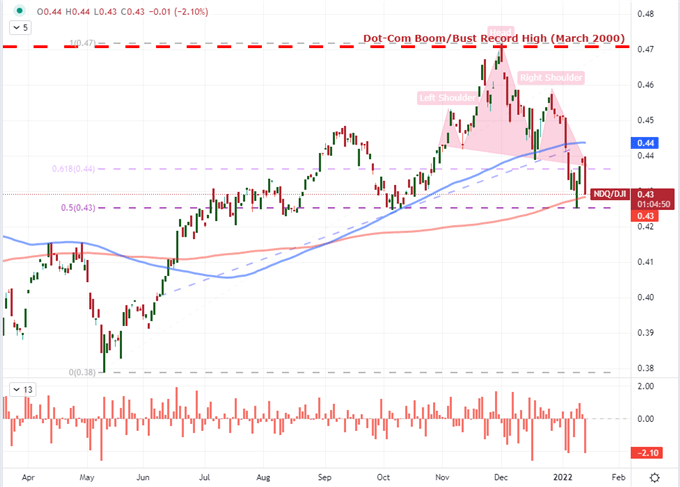

While there is a breadth to the pullback in risk trends this past session, I find there is more value for subsequent trade by evaluating the nature of the speculative shift for the broader market. Notably, the more exaggerated risk assets of the past year – meme stocks, cryptocurrencies, SPACs – were all off in Thursday trade. Yet, there was more acute intention to be found within the US equity market. While there are already problems for breadth in the stock market, I think the ‘growth versus value’ measure from the Nasdaq-to-Dow ratio is more accessible. As it happens, the ratio dropped -2.1 percent Thursday for the third biggest daily loss in eight months. This doesn’t fundamentally change the course nor tempo of the market, but it adds further weight to a more gradual turn in the market’s appetites. With earnings on tap, there will be a corporate element to consider in the equation of hold out confidence. The focus Friday will be earnings data from JPMorgan, Citi, Wells Fargo and BlackRock. This group poses greater weight for the blue chip Dow over other major indices; but there is a macro angle to draw from these figures as well. These major financial institutions general benefit from higher interest differentials and elevated volatility. Did they see those benefits these past three months?

Chart of the Nasdaq 100 to Dow Ratio with 200-Day Moving Average and 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

It is Looking More and More Like the Fed Is Warning of a March 16th Rate Hike

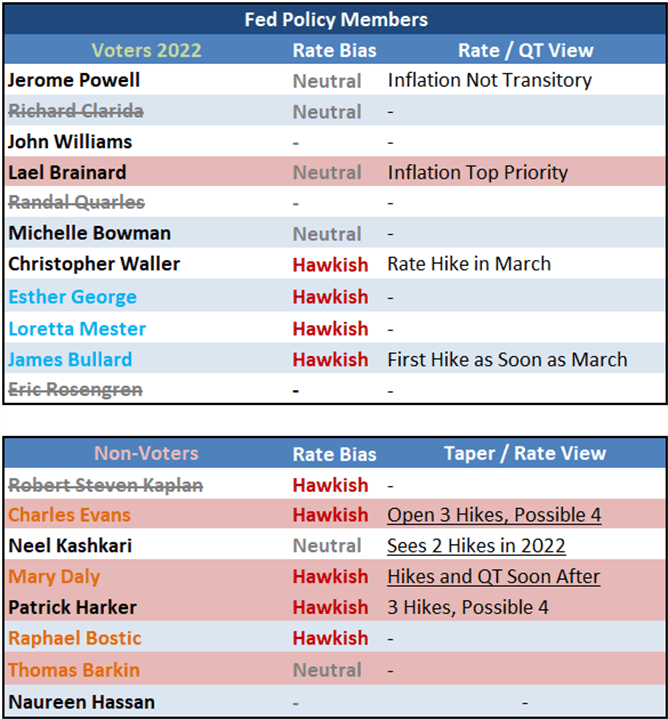

While earnings session will continue to punch onto the US financial headlines, my principal fundamental interest remains the status of US and global monetary policy. This past session, we had a run of Fed members speaking; and the message seemed to be the same. Vice Chair Lael Brainard was arguable the most dovish member at present and she testified in her renomination hearing that inflation at four decade highs was priority. Meanwhile, other officials such as Charles Evans, Patrick Harker, Richard Clarida, Thomas Barkin and Mary Daly were all voicing materially more-hawkish views than what we had seen from these in previous months. I was particularly surprised by San Francisco President Mary Daly’s remarks that anticipation of a March rate hike was ‘quite reasonable’. We are about to pass into the standard media blackout that precedes rate decisions by a week and a half. If you intended to announce a semi-official warning that a hike was coming on March 16th at the January 26th policy meeting, you would first want to signal to the market the possibility of such as shift in the preceding gathering.

FOMC Member Policy Stance

Table Made by John Kicklighter

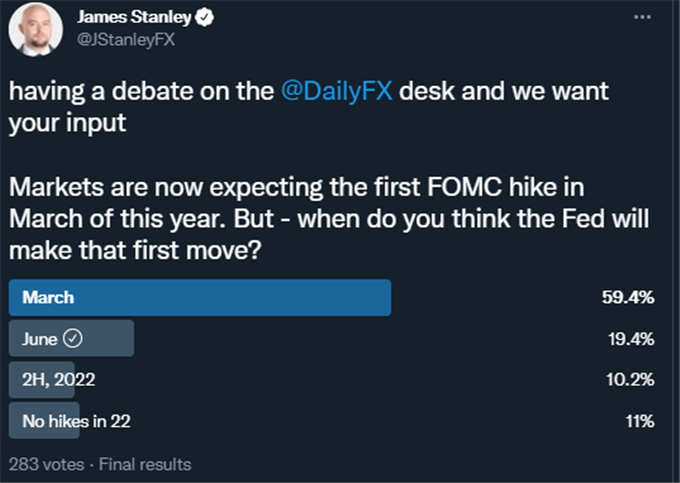

Anticipation for a March rate hike has surged in the past weeks. Unofficially and anecdotally, my college James Stanley conducted a poll on Titter asking participants to vote on when they believed the Fed would announce its first tightening of the benchmark rate. Nearly 60 percent voted for March. From the market itself, we have US 2-year Treasury note yields to trade, but the rate forecast derived from Fed Fund futures is a more direct for interest rate focus. These products are currently pricing in 83 basis points of easing. Further, the CME’s Fed Watch tool pegs a March rate hike as an 86 percent probability. I was previously skeptical of this aggressive forecast, but the Fed’s messaging over the past few weeks leads me to believe that they are using this flexible tool on purpose.

Poll Asking When the First Fed Rate Hike Will Occur

Poll from Twitter.com, @JStanleyFX

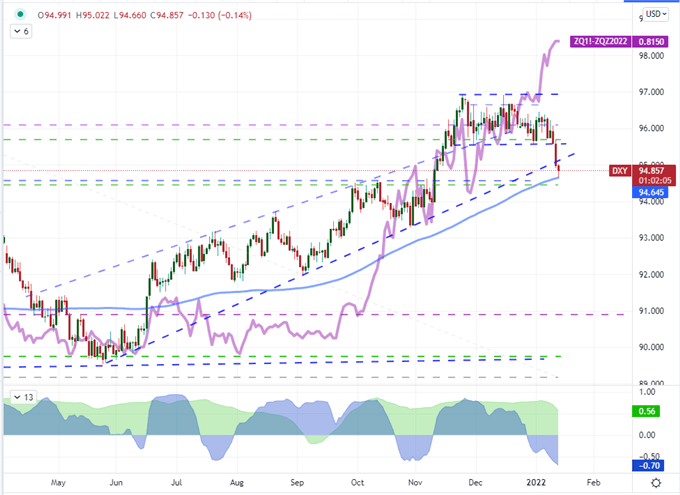

Why Does the Dollar Continue to Drop as Rate Forecasts Rise?

The probability of a rate hike in two months is the highest it has been in post-pandemic period. Nonetheless, the Dollar is still following the fundamental rails. While the Fed rate forecast has indeed advanced, it has been a far more restrained climb in the past few weeks. Further, the Greenback seemed to have already disconnected to the hawkish costs throughout December. While there has been a hawkish about face, I do believe that the markets have already priced this shift through the US Dollar – those equities are more of a ‘from my cold dead hands’ asset type. There is still capacity for the rate forecast to push beyond what the market was willing to consider for hikes, but that would likely venture into the territory of unnerving investors. It was Philly Fed President Harker who remarked that the central bank would act in a significant slide from capital markets. The only question in my mind is: where is the tipping point?

Chart of DXY Dollar Index with 100-Day SMA and Implied 2022 Rates with 20 and 60 Day Correl (Daily)

Chart Created on Tradingview Platform

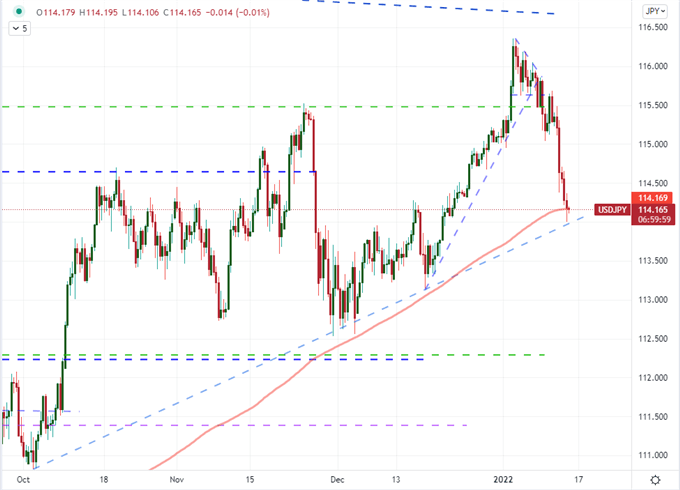

It is possible that the Dollar still has some untapped reserves for relative yield, but I believe the risks point lower. Whether growth flags, inflation peaks or speculative trends have an adverse reaction to the same monetary policy; there are natural counterbalances to a persistent Dollar bullish theme. It will ultimately be difficult for the Fed to outpace its major counterparts over time, so a moderation seems practical – though a groundswell in global monetary policy trends is also possible so long as omicron risks level out. The question of bearish momentum is an issue for pairs like EURUSD, GBPUSD, USDCAD and NZDUSD; but it is far from a deal breaker for USDJPY. Should US rate forecasts drop or risk trends stumble, this pair will benefit the course correction. Should the same motivation that cuts US rate forecasts also spill over to risk aversion, it will compound the bearish pressure on this cross.

Chart of USDJPY with 200-Period Moving Average (8-Hour)

Chart Created on Tradingview Platform