S&P 500, Fed, FANG, GDP and China Talking Points

- The S&P 500 managed to tag a record high this past week, but the picture looks as much a reversal risk as it does a bullish achievement

- Monetary policy is a key theme this week with Fed forecasts nearing certainty of two 2022 rate hikes and the ECB, BOC and Brazilian central banks on tap

- Other top market-moving themes ahead include FANG earnings, US and Euro-area 3Q GDP releases and the lingering threats from China’s Evergrande troubles

Is That a Bullish Confirmation or Bearish Warning?

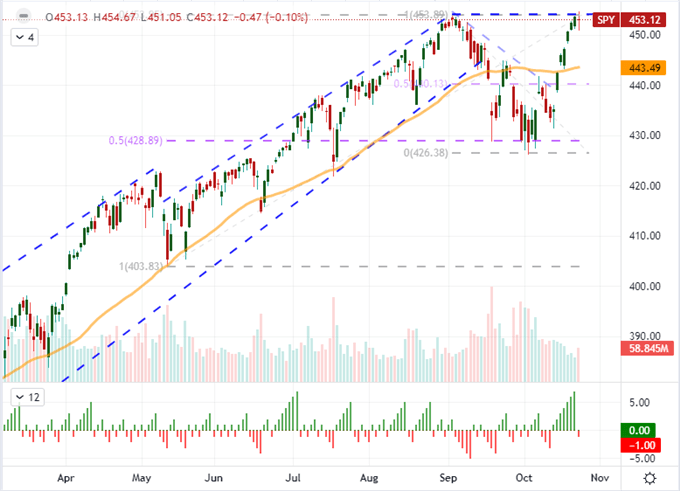

If we were to evaluate this past week’s sentiment purely on a week-over-week assessment of top ‘risk’ benchmark, I could appreciate the interpretation that we are on firm bullish footing. For the S&P 500, the week registered a 1.6 percent advance and a record high close. However, that was about as far as the enthusiasm would stretch. On a shorter time frame, the asset with the heaviest derivative footprint ended out Friday with its first bearish close in eight trading sessions. That would also come with a very prominent doji candle that looks dangerously like indecision at a possible double top with the early September high. With a loaded docket for the coming week from growth updates to rate forecasts to tech earnings, there is serious capacity for the markets to succumb to any ill-fated winds that sweep into seemingly unflappable sentiment.

Chart of SPY S&P 500 ETF with 50-Day SMA, Volume and Consecutive Candles (Daily)

Chart Created on Tradingview Platform

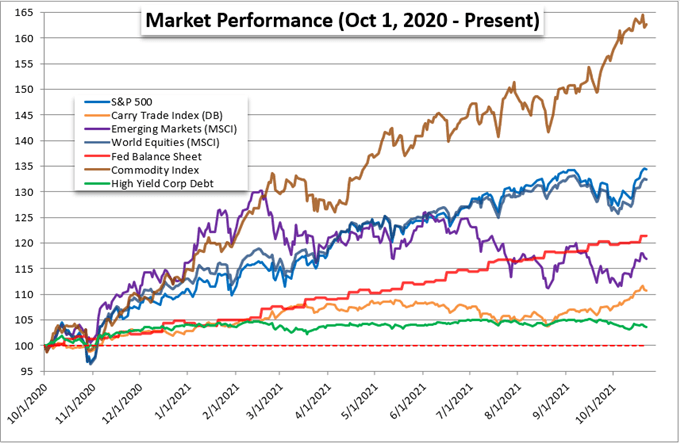

From a ‘risk’ perspective, it is important to point out that the future is not simply dictated by the SPX or the US indices in general. Sentiment is a financial matter that is agnostic to region or asset class. When appetite for greater return genuinely swells across the system, we find a correlation and intensity across assets that generally tend to do better when speculators are on the hunt for capital gains (buy low, sell high). Taking stock of sentiment this past week, there was a notable disparity between US and rest of world equities which is a concern given how closely related they happen to be. For the likes of carry trade, emerging market assets and junk bonds; the past week was actually bearish. I don’t consider this to be the foundation of a stealthy bear trend for the week ahead, but it will at least trip up progress for the more ambitious assets.

Chart of Year-Over-Year Relative Performance of Risk-Sensitive Assets (Daily)

Chart Created by John Kicklighter with Data from Bloomberg Terminal

Top Event Risk Over the Coming Week

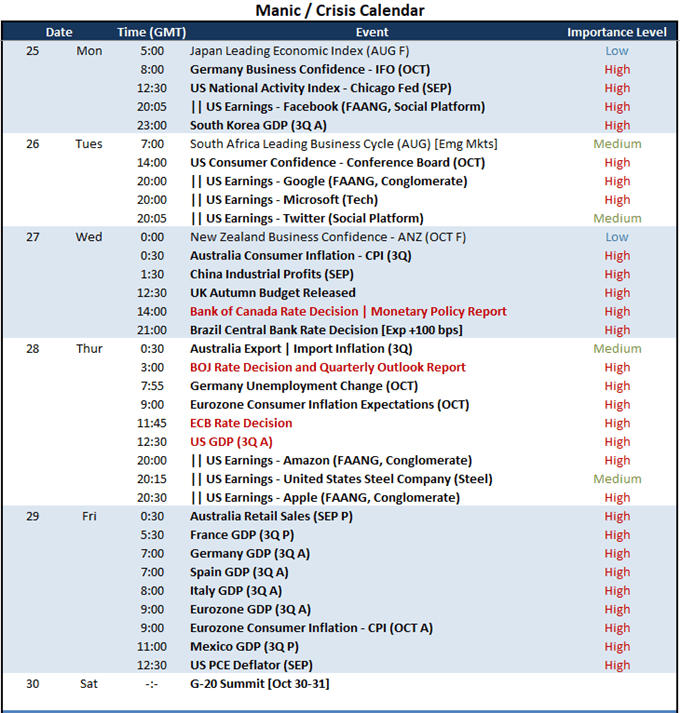

As far as scheduled event risk goes, the docket for the coming week is overloaded. There are plenty of one-offs that I suspect can generate isolated pockets of heavily volatility. However, the capacity of technical breaks that can transition into follow through is a much shorter list. From the long list of scheduled events, I would only consider the US GDP release a practical lever for a systemic drive based on its own merits. Sure, many of the top events on the docket below could start the ball rolling, eventually gaining enough of a snowball effect to eventually tip the scales on speculative intent. Yet, that would fully depend on the market’s general sense of intention. From the US government’s official third quarter GDP update, we will be given insight into the health of the world’s largest economy which will be explicit influence in capital allocation, the Fed’s monetary policy options and the contentious debate in Washington DC over the fate of the Biden administration’s stimulus bills.

Calendar of Major Macro Event Risk for the Week

Chart Created by John Kicklighter

Top Fundamental Theme: Monetary Policy

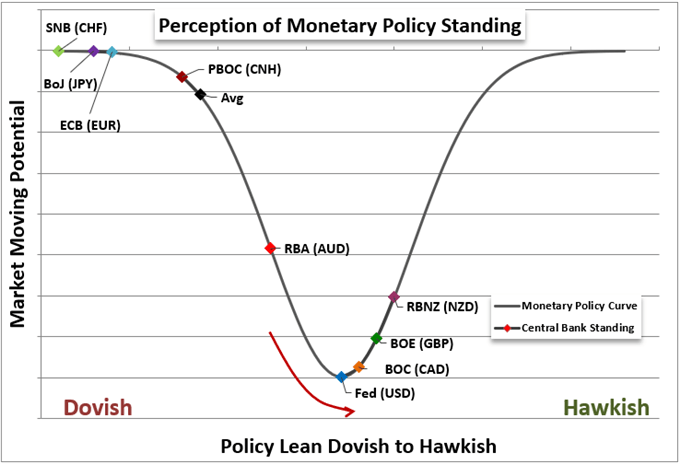

From the various themes that I will monitor for market moving potential, monetary policy remains one of the most loaded concerns on my list. The long-term implications of shifting from seemingly unlimited accommodation to a slow withdrawal of support may prove unprecedented after more than a decade of support from deep pocketed buyers. However, given how systemic this relationship is, recognition from an aloof and ‘hungry’ market is likely to take time. In the meantime, there is plenty of isolated volatility to monitor in the meantime. There are a few high profile central banks due to weigh monetary over the coming week. The forecast for most severe change rests with the Brazil authority which is expected to hike rates 100 basis points to combat high inflation. The European Central Bank (ECB) is the top billing for scope, but it is most likely going to follow a long path to curb the market’s emergent speculation of normalization in the foreseeable future. The wildcard is the Bank of Canada (BOC) where the market is pricing in four full rate hikes over the coming year.

Chart of Relative Monetary Policy Standing of Major Central Banks

Chart Crated by John Kicklighter

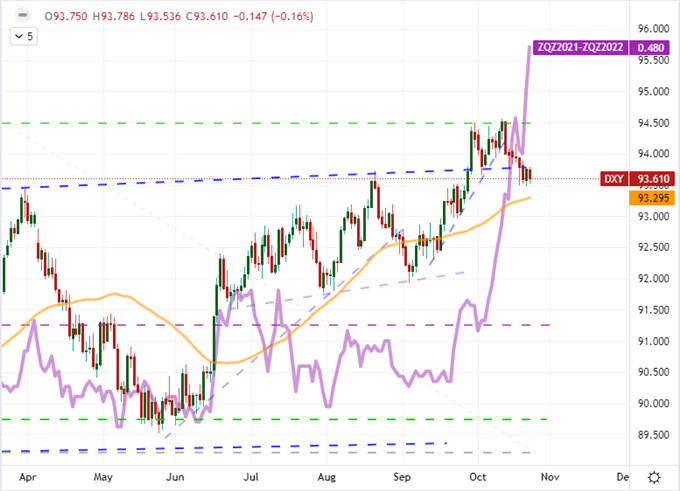

Another monetary policy watch item for the coming week is the Fed forecast. The next FOMC rate decision is not scheduled until November 3rd (the following Wednesday), but speculation is extraordinarily high. According to Fed funds futures, the markets are close to fully pricing in two, 25-basis point rate hikes through the coming year – much more aggressive than the central bank itself has allowed for in its forecasts. From the docket, there is event risk that can contribute to this forecast in the form of Friday’s PCE deflator, the Fed’s favorite inflation stat. All of this considered, the Dollar has very notably failed to take advantage of the monetary policy charge.

Chart of DXY Indexwith 50-Day SMA, Overlaid with Fed Forecasts 2022 (Daily)

Chart Created on Tradingview Platform

The Other Themes: GDP; Earnings and China

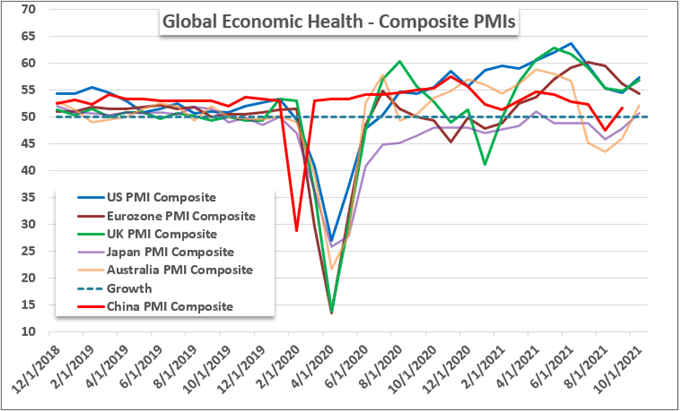

Among the other fundamental landmines ahead, official 3Q GDP figures will be distinct events to keep tabs on. The week starts with South Korea reporting Monday evening / Tuesday morning. This may not be a top economy relative to the US or the Eurozone, but it offers a better reading of Asia’s general health than the previously release Chinese official growth update. Later in the week, the US GDP update is scheduled for release Thursday (after the ECB decision), but it may take a significant deviation from forecasts to seriously rouse the markets. I will be watching risk trends more than the Dollar for response to this report. On Friday, the European 3Q figures are due alongside the Mexican release.

Chart of Major Economies Composite PMIs (Monthly)

Chart Created by John Kicklighter with Data from Markit

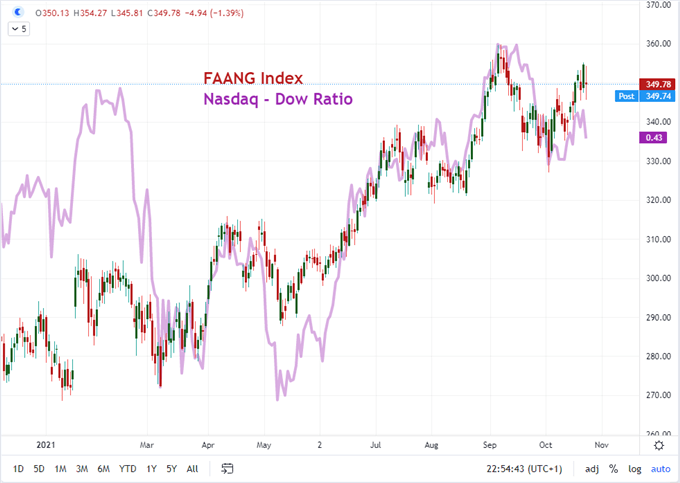

On the earnings front, we are moving from a thin week to a heavy one. There are more than a few heavy hitters on tap including GE, UPS, Twitter, General Motors, Boeing, Caterpillar, United Steel and Exxon Mobil. However, the theme amid this heavy flow of corporate data will center on the tech giants. In addition to Microsoft, Twitter and AMD; we have most of the FAANG members scheduled to present their performance numbers. Facebook reports Monday; Google on Tuesday; Amazon and Apple on Thursday. While the profile of this grouping has faded this year; its performance relative to the Nasdaq 100 remains intense – which is subsequently an outperformer of general US stocks that are themselves a top speculative asset type. In short, this is the pinnacle of risk appetite.

Chart of FAANG Index Overlaid with the Nasdaq-to-Dow Ratio (Daily)

Chart Created on Tradingview Platform

Finally, a word on the health of China. I have tried to keep this in the conversation consistently over the past weeks because it represents the uncertainty around the world’s second largest economy and perhaps one of the greatest and vaguest threats to the global financial system. At the end of this past week, it was reported that Evergrande moved $83.5 million to a trust held by Citibank that will be used to pay foreign investors who are due repayment after a missed debt interest payment back on September 23rd. If the company didn’t make the funds available, it would have constituted a technical default. A ‘foreign’ default could have been contested by the Chinese government, but it would have raised global tensions over financial stability dramatically. For now, the situation has been kept to a controlled boil.

Chart of USDCNH with 20-Day SMA Overlaid with FXI China Large Cap ETF (Daily)

Chart Created on Tradingview Platform