Fed, S&P 500, Dollar USDJPY and GBPUSD Talking Points

- The Federal Reserve deferred the start of its taper, but its language was as definitive of an imminent move by the central bank since the pandemic and rate hikes are on the radar

- A risk relief rally has been slow to follow the FOMC extension and reports of actions to offer relief to Evergrande’s looming financial straights

- Top scheduled event risk for Thursday is still dense between further rate decisions including the Bank of England and a September PMIs for a growth update

The Fed Delivers a ‘Hawkish Hold’ and Market Uncertainty

How did this week’s most anticipated event risk play out? A rally for the Dollar and a hesitant charge from the S&P 500 heading into Thursday trade gives a mixed view of how the FOMC decision is registering among market participants – and that is not a good sign. To overcome the rising concern around a number of fundamental issues, questions over stretched values and the inherent expectations associated to seasonality; the bullish camp could use a definitive risk appetite booster. That said, it is perhaps not surprising that the markets were not particularly enthusiastic following the Fed’s update this past session. First and foremost, there was immediate relief in the news that the group did not see fit to announce the start of its taper at the end of its two-day meeting. The most aggressive of the probable scenarios was averted and we have another six weeks until the pressure returns. Yet beyond the immediate stay, the event was still couched in hawkish warning.

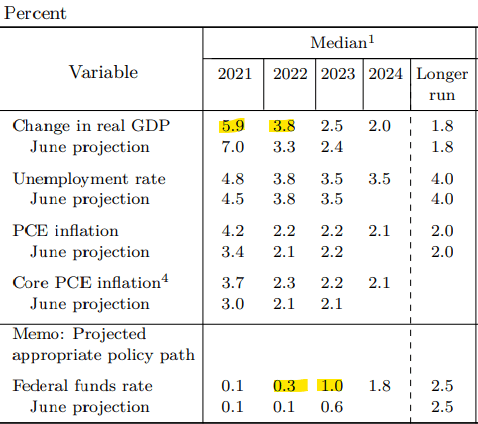

FOMC Summary of Economic Projections Table

Chart from FOMC SEP for September 22, 2021

Immediately after recognizing that the Fed had not pulled the trigger on tapering its asset purchases, a quick scan of the Monetary Policy Statement revealed the group believed a reduction “may soon be warranted” if the current trajectory were maintained. Further, in Chairman Jerome Powell’s press conference, the central banker reported that the inflation threshold was “more than met” while “many” in the group believed the employment objective was met. That suggests the decision to defer was extremely narrow. Further adding to the hawkish outlook was the ‘dot plot’ which showed a 9-9 split where half of the group expected the first rate hike to take place in 2022 and the other half later. Considering that the annual rotation of voting members will see four hawks earn a vote next year, the chances seem to increase significantly. Powell would also suggest that the taper could wind down by mid next year which would align to a year-end hike as well. Perhaps the remark that left the biggest impression on me was the Chairman’s suggestion that asset purchases’ usefulness had decreased significantly. Of course, the question is: how critically will the market reflect on this event going forward?

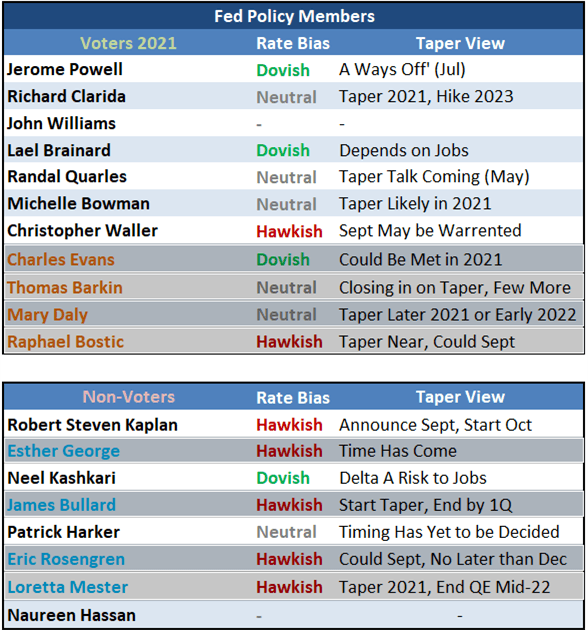

Federal Reserve Policy Members

Table Created by John Kicklighter

Post FOMC Risk Appetite

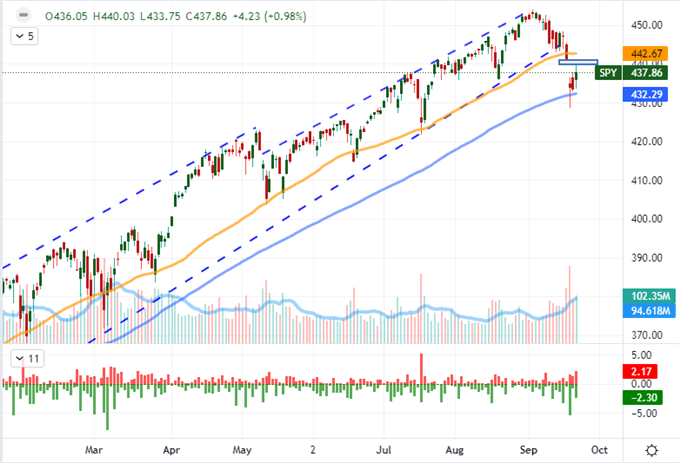

Evaluating speculative appetite in the aftermath of the US central bank decision, I don’t think the markets have settled on their collective view for the next phase. Of course it is critical to monitor Asian and European markets, but unless there is a surprising development not on the docket (more likely to be a negative scenario), global investors may wait on the US to evaluate its interpretation of the landscape. I will be watching the S&P 500 in particular as it has technical milestones that seem to align to the nuanced balance on the fundamental side. Wednesday’s session found healthy volume but the post-Fed chop curbed serious momentum and capped the effort to close the ‘gap’ that we started the week with. The daily tails reflect the immediate indecision while the 50 and 100-day simple moving averages offer a fairly distinct range – between which we are hovering directly in the middle.

Chart of SPY S&P 500 ETF with Volume, 50 and 100-Day SMAs and ‘Tails’ (Daily)

Chart Created on Tradingview Platform

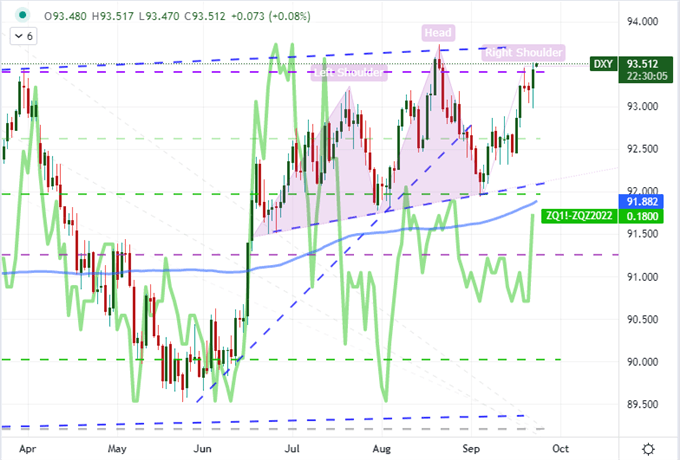

The Dollar’s own technical bearings are more pressing and that seems to better suit its own sensitivity to the relative monetary policy position of the Fed to its counterparts. Interest rate (yield) forecasts are an important pricing element to FX, and after the central bank’s remarks we found Fed Funds futures pricing through the end of 2022 jump 3 basis points (or 20 percent). For the Greenback’s part, the DXY trade-weighted index charged to within easy reach of the 11 month swing high set last month. Perhaps an additional push from scheduled event risk Thursday can help the market overtake its technical boundary; but liquidity is not deep enough to simply guarantee a break without a strong point of motivation.

Chart of DXY Dollar Index with 100 SMA and Fed Fund Change Forecast Through Dec 2022 (Daily)

Chart Created on Tradingview Platform

As I watch the Dollar’s efforts to sort out its fundamental health, I am going to be monitoring certain pairs more closely than others. EURUSD for example is not at the top of my list. The world’s most liquid currency cross is less motivated to mark a critical break without a decisive backdrop even if the ECB made its dovish position clear two weeks ago and given there is a Eurozone PMI ahead. For USDJPY, the monetary policy intent contrast is just as prominent, but this pair also abides a sense of risk trends. Interestingly, both currencies are treated as safe havens; but the monetary policy contrast may alter the balance for the cross. Another Dollar pair of interest in these particular fundamental circumstances is USDBRL. Brazil’s central bank announced, after a delay, that it had increased its benchmark Selic rate 100 basis points to 6.25 percent. That was exactly in line with economist expectations. However, the warning that another 100 basis point hike could come next month was less certain. The BRL doesn’t trade 24 hours, so we will see its response when trade resumes.

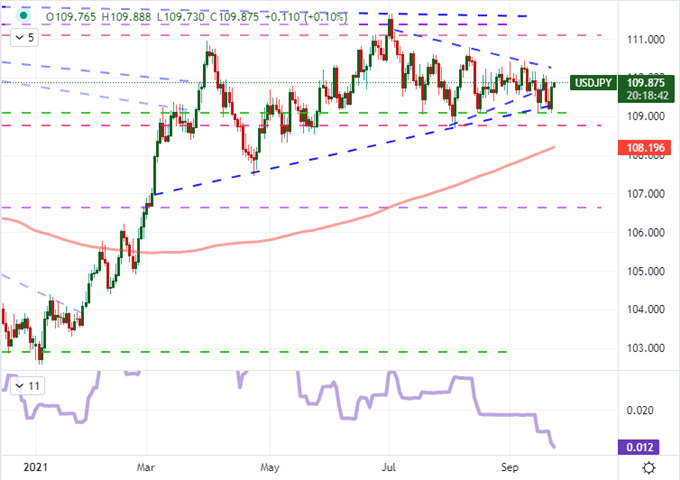

Chart of USDJPY with 200-Day SMA and 30-Day Range (Daily)

Chart Created on Tradingview Platform

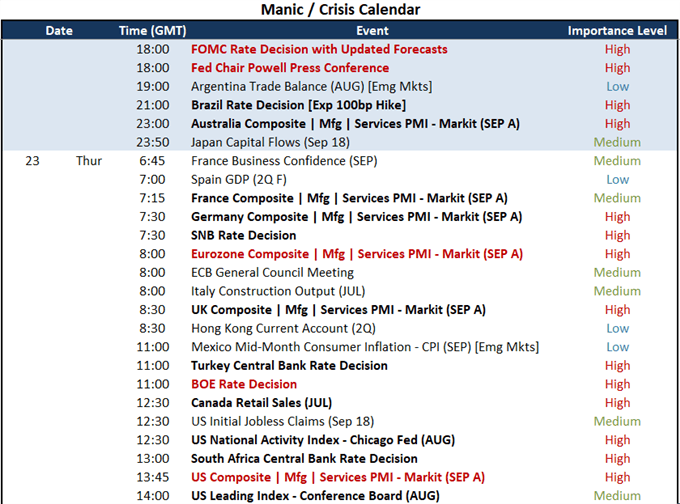

Top Event Risk for Thursday

While the Fed rate decision was the top event risk on my docket for potential market impact, there is still a range of important fundamental fodder ahead and an environment that doesn’t seem to have a clear bead on its views of market confidence. While there are various indicators worthy of note – like Canadian retail sales and the Chicago Fed’s US national activity index – there are two themes to monitor over the next session: monetary policy and economic health.

Economic Event Risk for Thursday

Calendar Created by John Kicklighter

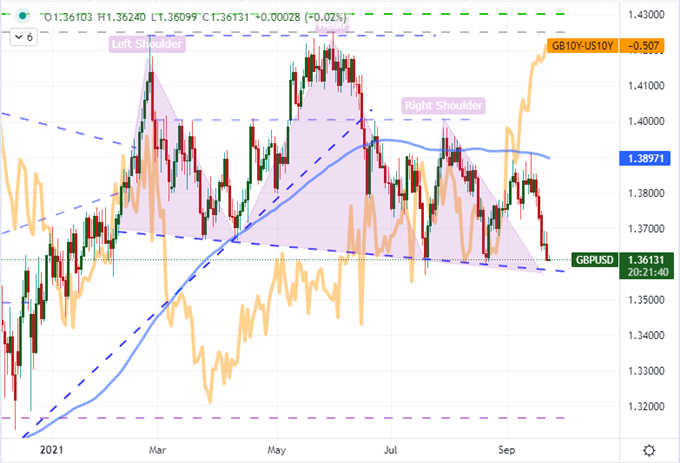

In addition to the Fed, Bank of Japan and Brazilian central bank decisions that are already behind us; we are due policy insight from the Bank of England, Swiss National Bank, Turkish central bank and South African Reserve Bank. Of these four, the BOE carries the greatest global punch. In the hierarchy of policy standing, I consider this group to be a relatively hawkish relative to the likes of the ECB and BOJ; and it may be on the same level as the Fed. Markets are pricing in the first hike from this group sometime in the spring of next year and UK 10-year yields have rallied noticeably these past few weeks. This may, if anything, stage for a more probable downside surprise; which makes GBPUSD near support look particularly interesting.

Chart of GBPUSD with 100-Day SMA and UK-US 10-Year Yield Differential (Daily)

Chart Created on Tradingview Platform

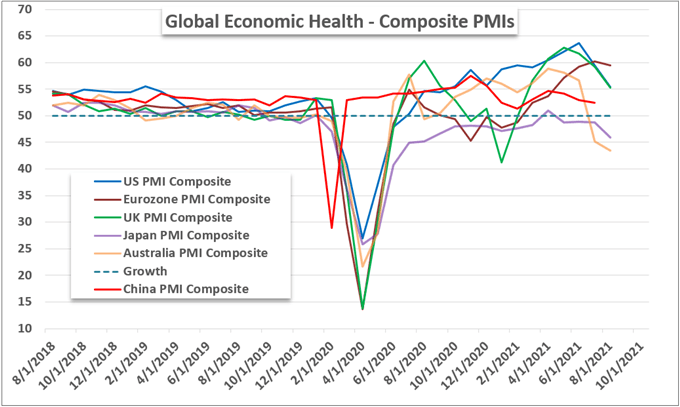

On a different fundamental thread, the September preliminary PMIs are going to offer a less prominent but arguably more important insight. The past few months have seen a notable slowing of the post-pandemic recovery pace of economic expansion, but that is to be expected. It isn’t practical to keep running at that same pace of expansion. However, that normalization may rouse greater concern from market participants if they are already registering a sense of risk and looking for reasons to unwind excessive exposure.

Major Economies’ PMI Growth Measures (Monthly)

Chart Created by John Kicklighter with Data from Bloomberg, Markit