Talking Points:

- A rebound in risk appetite was registered across a wide range of assets, but a move founded on Italy will not persist

- The Dollar's multi-week bull trend slipped thanks to the Euro's rally, will the USD forge its own path on rate forecasts?

- A BoC surprise sparks a Loonie rally, Oil holds trend at $66 and China's fundamentals grow in stature

See how retail traders are positioning in EUR/USD and US Oil after their respective bounce as well as US and European Indices as they try to revive a wayward bull trendusing the DailyFX speculative positioning data on the sentiment page.

The Leap from Rebound to Trend for Risk Italy Can't Bridge

Just as intense as the wave of risk aversion was on Tuesday, the rebound in sentiment this past session proved equally charged. The quick turn in speculative bearing would insinuate that a great risk had suddenly been lifted from the market's shoulders. And, if we were to insinuate from the bounce a trend, it would further suggest that an important fundamental theme was just starting to gain traction for a lasting momentum ahead. Is that what the past session's performance reflects? It is certainly true that the rebound in risk assets was a broad one. Global indices, Treasury yields, Yen crosses and emerging assets all caught the bid. And yet, there were some cracks in progress. Seeing the S&P 500 jump back above 2,700 short circuits a key breakdown, but US equities have a clear bias towards buoyancy. Further, despite having not joined in the retreat Tuesday, the Nasdaq couldn't break the upper end of its two-week range and FAANG didn't charge to a new intraday record high even though it would take only a modest advance to achieve the milestone. Conviction depends on motivation, and the spark for this nascent enthusiasm was of dubious source. If an easing of Italian political fears was the boon, then there is little pervious discount to buy. Meanwhile, trade wars, monetary policy and growth still present plenty of concern for investors keeping tabs on market potential. This is not to say that risk appetite cannot gain further traction, but it will require more than an abatement of Italy's issues.

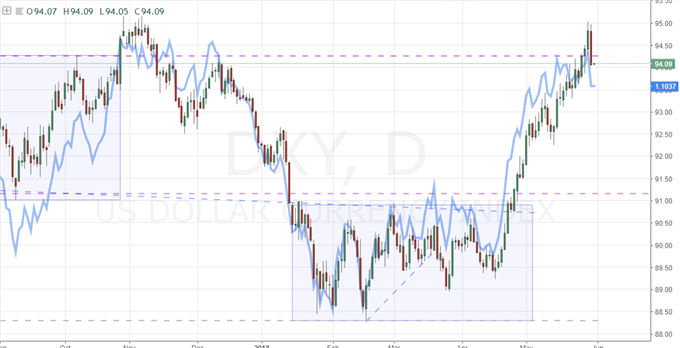

Dollar is Getting its Cues from the Euro, Will Rate Forecasts Change That?

The Dollar certainly was not excluded from the volatility of this past session. The Greenback posted is an intense, single-day decline that should be kept in the context of its multi-week trend whether we intend to pick a top or just see a pullback in a prevailing trend. Considering the top standard economic release for the US on the day was a better-than-expected trade balance figure, it was clear the local docket was not driver for the day. Considering the global rebound in risk, it is tempting to label the currency's response evidence that it has once again taken on its role as a safe haven currency. There may be some weight to that attribution, but it would need to be a uniquely sensitive measure of still-emergent concern to build upon a six-week trend that has not shown through in Yen crosses, volatility measures and other standards for sentiment. It is more likely that the Dollar has simply acted as the foil to a more active Euro. EUR/USD has marked pace on a strong bear trend as capital leaves the second most liquid currency with few alternatives with the ability to absorb the outpour. A comparison of a trade-weighted Dollar index (such as the DXY) and an equally-weighted version shows both slid Wednesday. Yet, the performance in May's rally is markedly different. If the Dollar is simply playing counterpart to more active majors, keep a watchful eye on EUR/USD. That said, the upcoming PCE deflator (Fed's favored inflation measure) and the jobs data on Friday can attempt to wrest the influence back into the Dollar's hands.

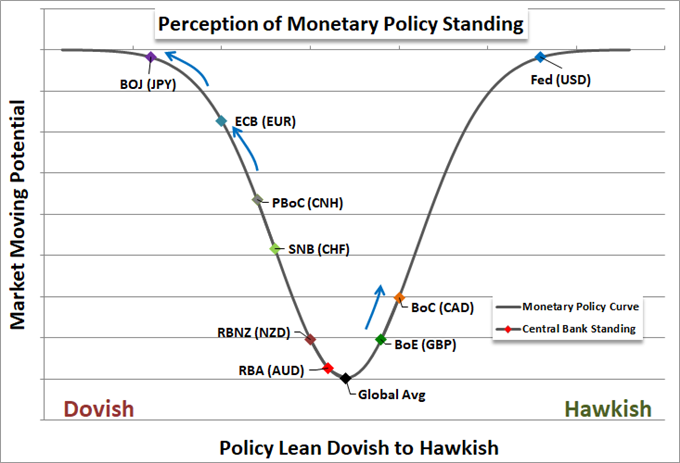

A BoC Surprise Leverages a Strong Loonie Charge

I was preparing for a heavy bias and unbalanced range of scenarios for the Bank of Canada's rate decision on Wednesday. They instead caught me and many others by surprise. We have seen interest rate expectations from the Canadian authority drop steadily over the past few months as data softened and concern over trade wars spread to the group's own public evaluations. To further add to the skew, the general bearing of global monetary policy has cooled whether we reference the central banks' own assessments (like the BoJ scrapping its time frame for returning to its inflation target) or the market's assessment as with Fed Funds futures. It was therefore, the safest path for the BoC to follow to conform to caution and halt all expectations for hikes. Instead, the group emphasized inflation at seven-year highs, maintained its optimism for growth and struck its 'cautious' language for trade. Not only was this a surprise, but it fosters a serious contrast to global monetary policy. The Canadian Dollar's rebound considering this is more than reasonable. However, is it trend material? The contrast is certainly distinct, but to support a steady bull trend, it would suggest there is an appetite for a 25 basis point hike sometime over three months - and that is a very small yield advantage to chase. Weigh your convictions in the theme before you set expectations for the individual player.

Oil and China Weigh Conviction and Focus as Themes Compete

With favorable risk winds to the market's back, it came a little surprise that some of the atypical risk-oriented assets would enjoy the move as well. In commodities, crude oil took advantage of its technical hold at $66 (trendline support, the 100-day moving average and a few other confluent factors) as a springboard to a rebound. We can add to this move attribution from the headlines as sources at OPEC walked back the suggested production increase suggested to compensate for Iran and Venezuelan reductions earlier this month. However, this looks more likely it aligns to a general nature for crude. Short-term, intense moves are fairly common and the past year has posted a general bull trend. Yet, we haven't seen a medium-term multi-week swing in some time. This suits the stop and turn nature of this market well. Meanwhile, the standings of China on the risk spectrum are indisputable at the extreme, but its standings and influence are hard to gain clear assessment on due to its data and disconnection from the system - not to mention is central point in rising trade wars. That said, the USD/CNH slip this past session wasn't nearly as impressive as the Shanghai Composite's sharp drop. The IMF's Article IV review of China carried the veneer of confidence about the future with a core of concern over trade and financial stability. Ahead, the start of the MSCI's purchase of A-shares and the expiration of the US metals tariff delay will factor into this sleeping giant's health. We discuss all of this and more in today's Trading Video.

If you want to download my Manic-Crisis calendar, you can find the updated file here.