Talking Points:

- Despite the uniform presence of critical support across assets (equities, EM, Dollar, etc), the market staved off a break

- June NFPs and the Fed's semi-annual monetary policy release Friday intensify the Dollar focus but don't provide bearing

- Top event risk ahead is Janet Yellen's testimony; while Dollar, Yen, CAD and Gold present the most pointed opportunities

The Dollar held a steady bear trend through the first half of 2017. What is in store for the currency heading into the third quarter? Reversal recovery or an extension of the pain? Download the 3Q USD forecast to see my views.

The markets were once again pushed to the technical brink, but speculators came back down from the ledge as they found a little more time to ignore their anxiety. While there was a modest pickup in risk oriented assets through the close of this past week, we are not far from the important technical milestones that could individually upgrade the threat of a systemic risk aversion if broken. The S&P 500's proximity to 2,400 serves as one of the more recognizable boundaries for the stretched position of the speculative rank, but it is far from the only one. European indexes (FTSE 100 and DAX), the Nikkei 225, the EEM emerging market ETF, the HYG high yield fixed income ETF, the DBV carry trade harvest ETF and more are all facing nearby support of their own. The week-ending event risk (including the first day of the G20) didn't trigger the ultimate break, but neither did it offer serious backing for a lasting rebound.

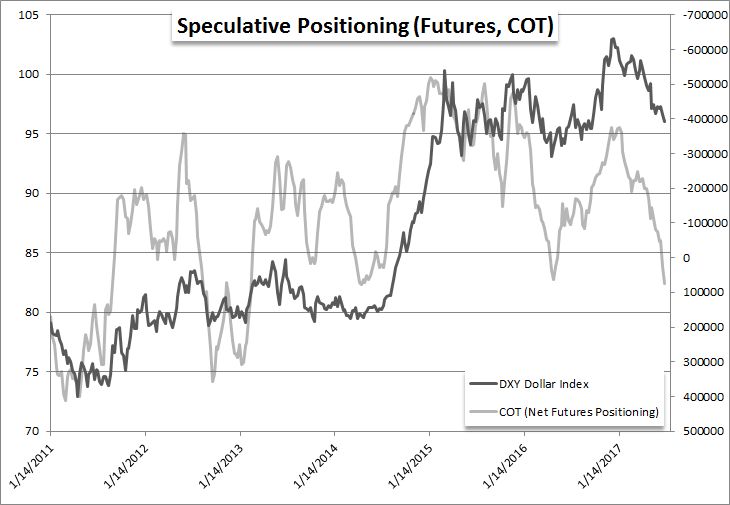

From the first day of the G20 leader's summit, we were reminded of the tension that is building in critical foundation for the financial system. German Chancellor Angela Merkel remarked that the view on trade was difficult - a not-too-subtle reference perhaps to the policy view that US President Donald Trump has expressed with vows to address a perceived imbalance in the world. In a limited impact, this could see the Dollar and US assets eventually marginalized in global capital flows; but if it mixes with deeper issues of speculative reach, it could very well disrupt the speculative rotation and hasten an overdue risk aversion. Another key event to close out the past week was the US June employment data. Nonfarm payrolls beat the tame consensus enough to temporarily lift risk trends, but the underlying statistics (jobless rate, participation, wage growth) neither offer motivation for a new phase of investor confidence nor charge US rate speculation anew for the Dollar. The Greenback remains just above the midpoint of a three decade range while EUR/USD, GBP/USD NZD/USD and AUD/USD are just below the upper bounds of their respective ranges (from multi-month to multi-year).

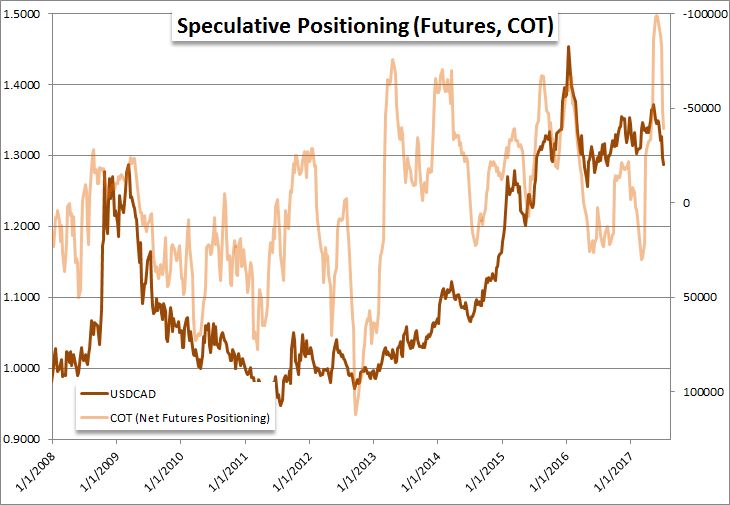

The Dollar will be put to the test again this coming week. Top event risk will be Fed Chairwoman Janet Yellen's two days of testimony before Congress for the semi-annual update. The FOMC released the Monetary Policy Statement that precedes this visit to Washington, and the group maintained the same cautious optimism for growth, inflation and policy that we have seen in statements and speeches. If this testimony is to have serious impact on the Greenback or speculative asset range, it will likely be through commentary on the Chair's view of financial excess and the need/effectiveness of accommodation. The Fed noted that despite the reach of financial assets, the productive translation to lending and economic activity was not readily transmitting. They would also suggest that financial risks are low and there were no liquidity concerns ahead - dubious assessments. Aside, from the Dollar focus and broad sentiment implications; there is opportunity with Canadian Dollar pairs (with the BoC decision), Yen crosses and Kiwi pairs. We discuss what is ahead and how best to approach it in today's Trading Video.

To receive John’s analysis directly via email, please SIGN UP HERE