Bank of England Monetary Policy Report Due 07:00BST, BoE Governor Press Conference Released at 10:00BST

- Bank of England to Stand Pat on Monetary Policy

- Raised Likelihood for Short-Term Growth Projections to be Upgrade

- Negative Rate Commentary Key to Near-Term GBP Direction

Overview

The Bank of England is not expected to make any major changes to the current monetary policy after QE had been expanded by GBP 100bln at the prior meeting. As such, with a 9-0 vote expected for the Bank Rate at 0.1% and APF at GBP 745bln, with the Bank of England opting to keep the powder dry. That said, the focus will be on the accompanying statement for any hints over negative interest rates and the macroeconomic projections.

So Far, So V

Economic Data: Since the last monetary policy report (May), the economy looks to be tracking somewhat better than the MPC had initially envisaged in its illustrative scenario. The drop in growth which had been seen at a peak-to-trough of 27% from Q4 2019 to Q2 is now looking more like 20%. In turn, this raises the likelihood that GDP projections in the short term will see an upgrade. Another factor for consideration had been highlighted by BoE Chief Economic Haldane, who stated that fast indicators (high-frequency data) suggest the recovery in both the UK and global economies has come somewhat sooner and has been materially faster than expected. That said, with the path of the recovery largely dependent on the trend of coronavirus, the recent flare-up in COVID cases across the globe and parts of the UK are likely to see a much more gradual recovery than the return to pre-COVID levels by mid-2021 that the MPC had expected. On the inflation dynamic, the BoE’s illustrative scenario sees inflation returning to target by 2022, which much like the growth outlook is contingent on the trend in COVID cases. Alongside this, with expectations for a surge in the unemployment rate, longer-term inflation outlook risks being downgraded.

Bank of England May Economic Scenario

Source: BoE

Surprise Mention on Negative Rates Option Could See GBP Weakness

Negative Rates: Perhaps the most important element to focus on is whether there is a mention over keeping negative interest rates on the table. While the BoE is currently carrying out a strategic review over negative interest rates, which is not expected to be finalised until later in the year (In time for Nov MPR) a surprise explicit mention that negative rates are in the policy toolkit could see GBP under modest pressure with short end rates falling. As it stands, the outlook for the Bank of England is on the dovish side as OIS markets price in negative rates by May 2021 thus negative rate commentary (or lack of commentary) will see a notable reaction in short-end rates. As mentioned above, with a review on monetary policy yet to be completed a more explicit mention of monetary policy would come as to a surprise, in turn, we would expect the BoE to wait for a more opportune time, if needed.

Money Markets Price in Negative Rates by May 2021

Source: Refinitiv

EU-UK trade negotiations remains an interminable process with both parties reaching an impasse. Consequently, this will set up another Q4 political showdown given that the UK did not request an extension to the transition period ending December 31st, 2020. As such, with the clock winding down, political uncertainty will be heightened towards the year-end, potentially requiring further stimulus measures on the back on subdued activity and investment.

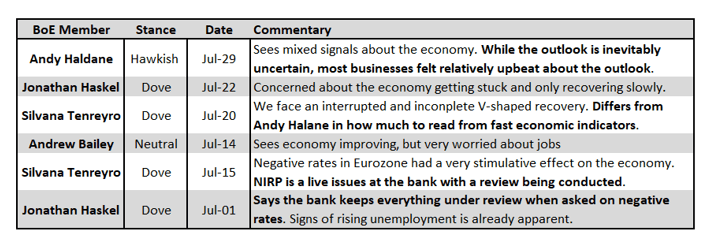

Key MPC Commentary Since June Meeting

External members, Haskel & Tenreyro more cautious than Chief Economist Haldane’s economic outlook.

Source: DailyFX, BoE, Refinitiv

Option Market Reaction

As it stands, GBP/USD ATM overnight implied vols at 14.35 suggests an implied move of 70pips (Vanilla straddle benefits with a move above 70pips in either direction), which covers the BoE meeting as well as the US jobless claims (option expires at 1500BST). As such, in the event of a more upside assessment from the BoE with a lack of mention on negative rates could see GBP/USD attempt a 1.32 test.