Fundamental Forecast for the US Dollar: Neutral

- Fed rate hike odds have pulled back in a fairly meaningful manner, representing a new headwind for which the US Dollar will have to contend.

- Futures market positioning may also prove a headwind for the US Dollar, now its most net-long since March 2017.

- According to the IG Client Sentiment Index, the US Dollar has a mostly mixed bias heading into the last week of June.

US Dollar Week in Review

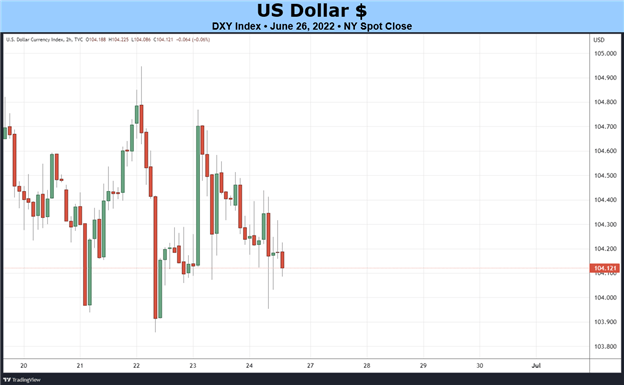

With Fed rate hike odds beginning to retreat, the US Dollar (via the DXY Index) fell for the first time in four weeks, dropping by -0.26%. EUR/USD rates added +0.61% while GBP/USD rates gained +0.44%. The decline in US Treasury yields weighed on USD/JPY rates, which closed higher by +0.23% after being up as much as +1.34% earlier in the week. The biggest movers were USD/CAD and USD/CHF rates, which fell by -1.02% and -1.16%, respectively.

A Full US Economic Calendar

The last few days of June and the start of July will bring about the usual burst of significant data releases over the coming days. In light of receding US growth expectations for 2Q’22, several speeches by Federal Reserve policymakers should also prove persuasive for markets.

- On Monday, June 27, May US durable goods orders are due at 12:30 GMT. May US pending home sales will be released at 14 GMT.

- On Tuesday, June 28, the May US advance goods trade balance will be published at 12:30 GMT. The April US house price index is due at 13 GMT, followed by the June US Conference Board gauge at 14 GMT. San Francisco Fed President Mary Daly will give a speech at 16:30 GMT.

- On Wednesday, June 29, Cleveland Fed President Loretta Mester will give remarks at 10:30 GMT. Weekly US MBA mortgage applications are due at 11 GMT. The final 1Q’22 US GDP report will be released at 12:30 GMT. Fed Chair Jerome Powell is set to talk at 13 GMT.

- On Thursday, June 30, the May US PCE price index will be published at 12:30 GMT, as will weekly US jobless claims figures, May US personal income data, and May US personal spending data.

- On Friday, July 1, the June US ISM manufacturing PMI is due at 14 GMT, as is the May US construction spending report.

Atlanta Fed GDPNow 2Q’22 Growth Estimate (June 16, 2022) (Chart 1)

Based on the data received thus far about 2Q’22, the Atlanta Fed GDPNow growth forecast is now at 0% annualized, holding steady over the prior revision on June 15. The neutral revision was due to “the nowcast of second-quarter real residential investment growth increased from -8.5% to -7.7%.” The next update to the 2Q’22 Atlanta Fed GDPNow growth forecast is due on Monday, June 27.

For full US economic data forecasts, view the DailyFX economic calendar.

More Rate Hikes Discounted, However…

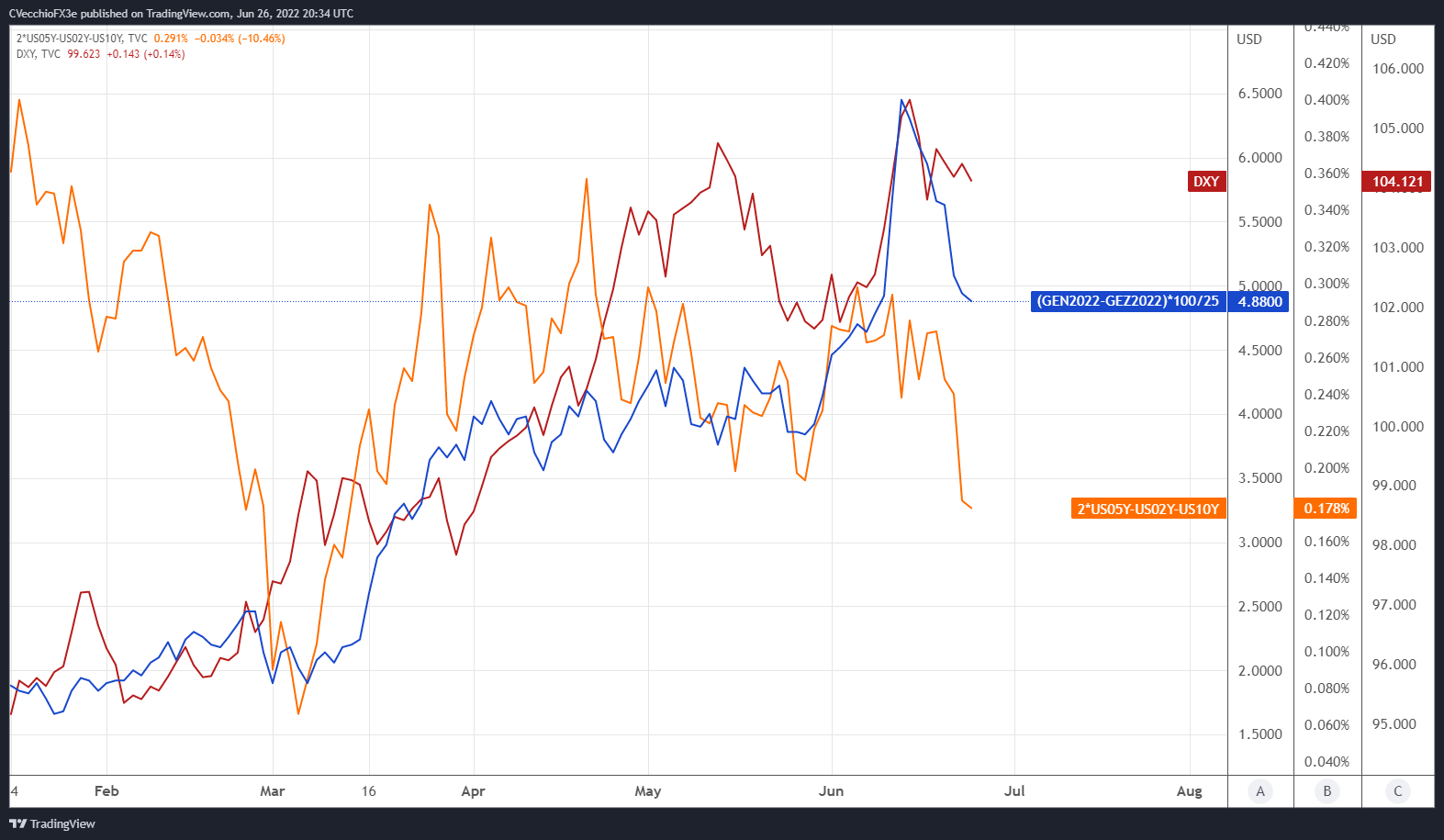

We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below showcases the difference in borrowing costs – the spread – for the July 2022 and December 2022 contracts, in order to gauge where interest rates are headed by the end of this year.

Eurodollar Futures Contract Spread (July 2022-December 2022) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: Daily Timeframe (January 2022 to June 2022) (Chart 2)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred from December 2015 to December 2018 when the Fed was in the midst of its last rate hike cycle. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates; the 2s5s10s butterfly should remain in positive territory.

After a 75-bps rate hike at the July Fed rate decision, there are currently four 25-bps rate hikes fully discounted through the end of 2022, plus an 88% chance of a fifth 25-bps rate hike. The 2s5s10s butterfly has narrowed in recent weeks, suggesting that the market interpretation of the near-term path of Fed rate hikes has become less hawkish.

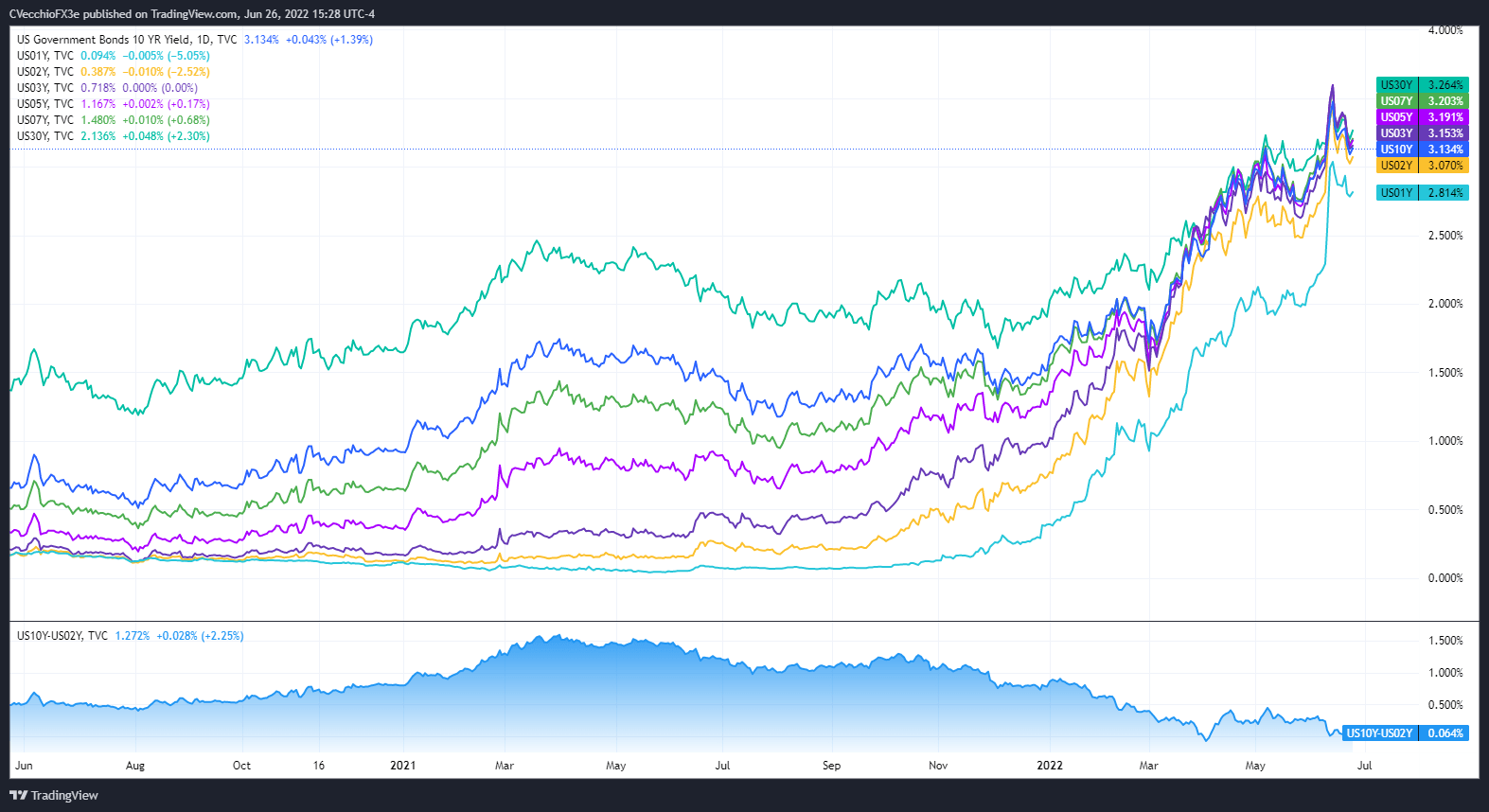

US Treasury Yield Curve (1-year to 30-years) (June 2020 to June 2022) (Chart 3)

The shape of the US Treasury yield curve coupled with declining Fed rate hike odds is acting as a headwind for the US Dollar. Even though US real rates (nominal less inflation expectations) remain in positive territory, other major currencies are seeing their own real rates rise, in part eliminated the gap that the US Dollar built up over the past few months; US Dollar’s relative advantage has been eroded.

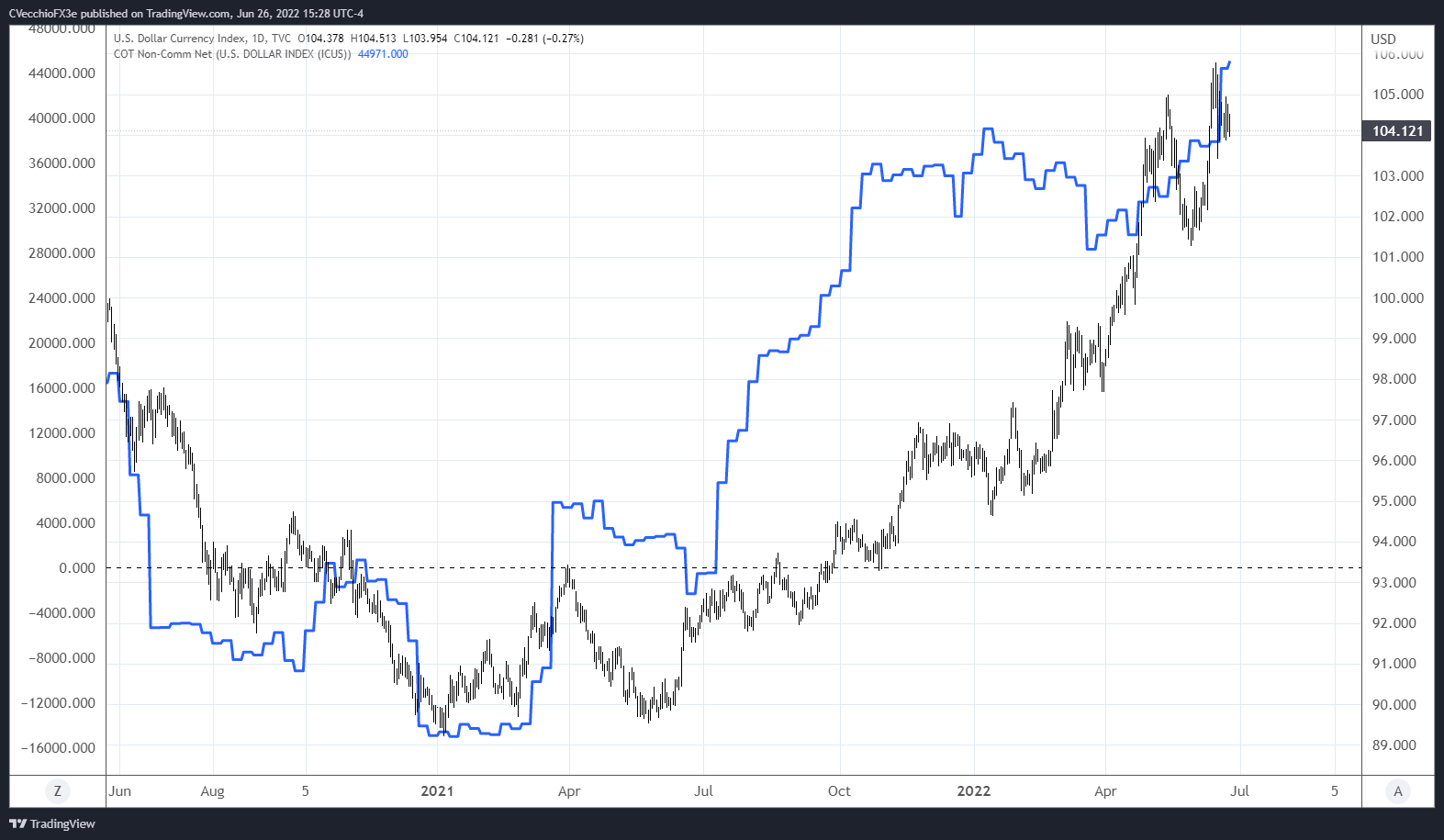

CFTC COT US Dollar Futures Positioning (June 2020 to June 2022) (Chart 4)

Finally, looking at positioning, according to the CFTC’s COT for the week ended June 21, speculators increased their net-long US Dollar positions to 44,971 contracts from 44,435 contracts. US Dollar positioning is now the most net-long since March 2017. Futures market positioning is increasingly becoming a headwind for further US Dollar gains.

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

--- Written by Christopher Vecchio, CFA, Senior Strategist