Australian Dollar Outlook: Domestic Factors Sidelined as the Fed Talks Up Rates

AUTRALIAN DOLLAR FORECAST: NEUTRAL

- The Australian Dollar has been boosted and dropped by central banks

- The Fed is on the rate hike march and the RBA is eyeing lift-off

- Swaying risk sentiment is gripping the globe, will AUD/USD hold on?

The Australian Dollar made a 10-month high at 0.7661 earlier in the week before weakening going into the weekend as global factors override the domestic picture.

The Aussie was boosted after the RBA monetary policy meeting on Tuesday. They left rates unchanged at 0.10%, but it was the hawkish tone in the proceeding statement that lifted the currency. In particular, the reference to being “patient” regarding tightening was dropped.

Trade data disappointed on Thursday, coming in at AUD 7.46 billion for the month of February, instead of AUD 11.65 billion anticipated. The miss in estimates was due to a 12% surge in imports, while exports were at the same level as January. The export side of the ledger hit forecasts, but imports were expected to rise by only 2%.

Ironically, the miss in the trade data is symptom of a red-hot Australian economy.

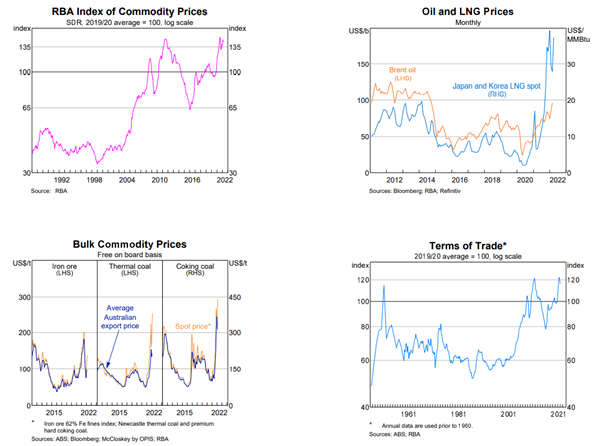

It should be noted that the impact of higher commodity prices is yet to be felt. The bulk of Australian exports are in long term contracts that roll over periodically and some already have, but those payments are still months away from hitting the ledger.

The charts below from the RBA highlight differences between the spot (current) price of bulk commodities against the prices received by exporters.

The terms of trade are at multi-generational highs, and this is further fuelling domestic growth. The war in Ukraine continues to see an increase in demand for many Australian exports to replace the Russian supply.

Various speakers from the US Federal Reserve hit the talk show circuit this week, seemingly spruiking their new-found love for all things hawkish. The term “transitory” is but a distant memory.

The impact is that yields are favouring the US Dollar, and this has undermined AUD. The 10-year government bond spread has narrowed toward 30 basis points (bp) from a recent peak of 47 bp.

China is also experiencing a rise in Covid-19 cases and as they pursue a zero-case policy, the financial hub of Shanghai is going into full lockdown. The iron ore spot price has eased as a result.

Looking ahead, jobs data will be released on Thursday, but it seems like it will need to be a large miss to have an impact on the currency. While the Australian economy is as healthy as it has ever been, the currency is at the whim of global markets and consequent sways in sentiment.

--- Written by Daniel McCarthy, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @DanMcCathyFX on Twitter