Talking Points:

- This week has seen an uptick in volatility in the U.S. Dollar, driven by Fed Chair Janet Yellen’s two-day Humphrey-Hawkins testimony in front of Congress.

- The Dollar’s near-historic second half of Q4 saw an aggressive retracement in January. The first half of February appeared as though that strength may be on the way back; but an aggressive reversal since yesterday morning raises fresh questions about USD-strength sustainability.

- If you’re looking for trading ideas, check out our Trading Guides. And if you’re looking for ideas that are more short-term in nature, please check out our Speculative Sentiment Index (SSI) Indicator.

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

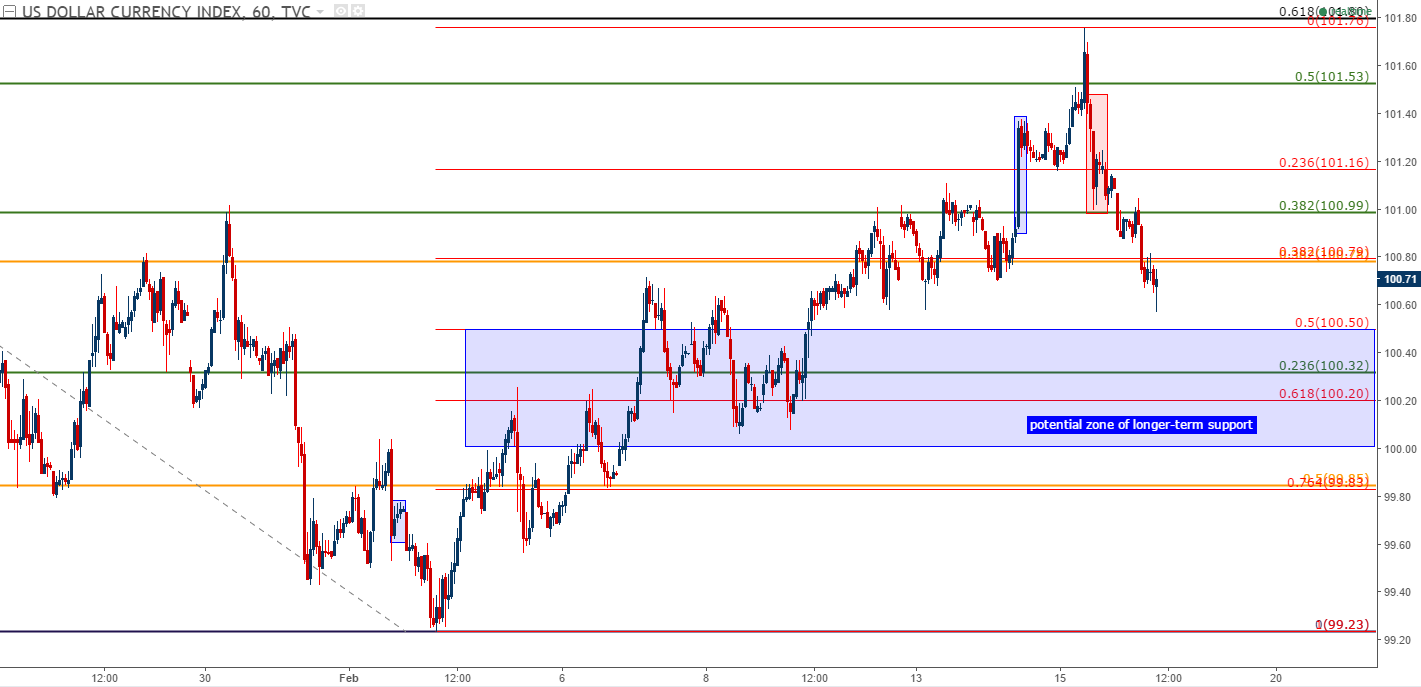

USD Shake and Bake: The past two days have seen some interesting U.S. drivers come into the fold; the highlight being Fed Chair Janet Yellen’s two-day Humphrey-Hawkins testimony in front of Congress on Tuesday and Wednesday of this week. Perhaps a bit obscured by the second day of that testimony was the U.S. CPI print for January that came out at .6% versus the expectation of .3%; a healthy beat that could bring that next rate hike from the Federal Reserve ‘sooner rather than later.’

But by looking at the Greenback’s price action yesterday, it might be difficult to decipher any additional bullishness, as prices have been running lower since the hour before Chair Yellen’s testimony began. As that CPI number printed at 8:30 yesterday, the U.S. Dollar posed a quick run above a key resistance level at 101.53. This is the 50% retracement of the January retracement in the Dollar and, with price action posing a sustained break above this level, the prospect of bullish continuation could look considerably more likely. But that move was short-lived as sellers came-in just ahead of Janet Yellen’s prepared remarks, and have been in control ever since.

Chart prepared by James Stanley

By taking a step back and looking at the U.S. Dollar’s weekly chart, the general level of strength is still quite visible, as even the recent uptick in bearishness has seen price action mostly residing above the prior zone of resistance on the Greenback. So, while the shorter-term charts are indicating the possibility of continued retracement-lower, the longer-term chart is still very much bullish:

Chart prepared by James Stanley

Timing a Return of Bullish Price Action in the Dollar:

The net takeaway from the past two days of Chair Yellen’s testimony has been a weaker Dollar (we’re currently under the level USD was at before day one of that testimony began), so patience should be in order if looking for that theme of short-term weakness to reverse into the larger theme of ‘big picture’ strength. But Chair Yellen had indicated on the first day of that testimony that rate hikes may be coming sooner rather than later, with the market’s focus near-immediately moving to the bank’s next meeting in March. The potential for continued Dollar strength certainly exists on a fundamental basis; and to better help in timing such a theme, traders can watch the chart to wait for bullishness to begin to show (again); first by buyers coming-in at support, followed by near-term higher-highs to indicate that bulls are able to re-take control.

Chart prepared by James Stanley

For those looking at options for taking on long-U.S. Dollar exposure, the Japanese Yen is likely an attractive counterpart, much as we saw in the midst of the Dollar’s bullish run in the second half of Q4. But last night we heard some rather unexpected comments from BoJ Governor Haruhiko Kuroda when he said that he thought that low rates could be sowing the seeds of the next financial crisis. This is pretty ironic given the Bank of Japan’s stance on monetary policy; but perhaps more disconcerting to traders, it may signal an increasing amount of hawkishness at the Bank of Japan. We discussed this theme ahead of the most recent BoJ meeting in the article, ‘How Much Confidence Does the BoJ Have in the Trump Trade?’

So, while last night’s comments from Mr. Kuroda may be innocuous on their face, this does speak to a theme that markets have been concerned about; positing that this recent bout of new-found strength on the back of the ‘Trump Trade’ may get the Bank of Japan to move away from their uber-dovish policy outlay, even with the potential for, maybe, possibly a rate hike later in the year (a distant prospect).

For traders looking at continuation prospects on the pair, or for those considering mannerisms of adding USD exposure, the long-term zone of support in USD/JPY ranging from 111.61-112.40 could be very interesting for such a theme. In between those two levels we have the 38.2% retracement of the ‘Trump Trade’ at 11.96, and this zone helped to set support last week.

Chart prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX