Talking Points:

- As we near the end of the year, we’re looking at the top three themes facing markets for 2016.

- Yesterday, we discussed the potential ramifications of a larger-slowdown in Asia.

- Today, we take a look at the commodity spectrum and how this might impact markets next year.

In yesterday’s piece we looked at the top theme for next year being an economic slowdown in Asia, because if this continues to develop there is likely little that can be done to stop it. An already-weakened Europe is too vulnerable to remain unscathed should a larger correction in Asia develop, and this would almost certainly bring on dire consequences for the ‘recovery’ being seen in the United States. But somewhat related is the continued carnage in commodities.

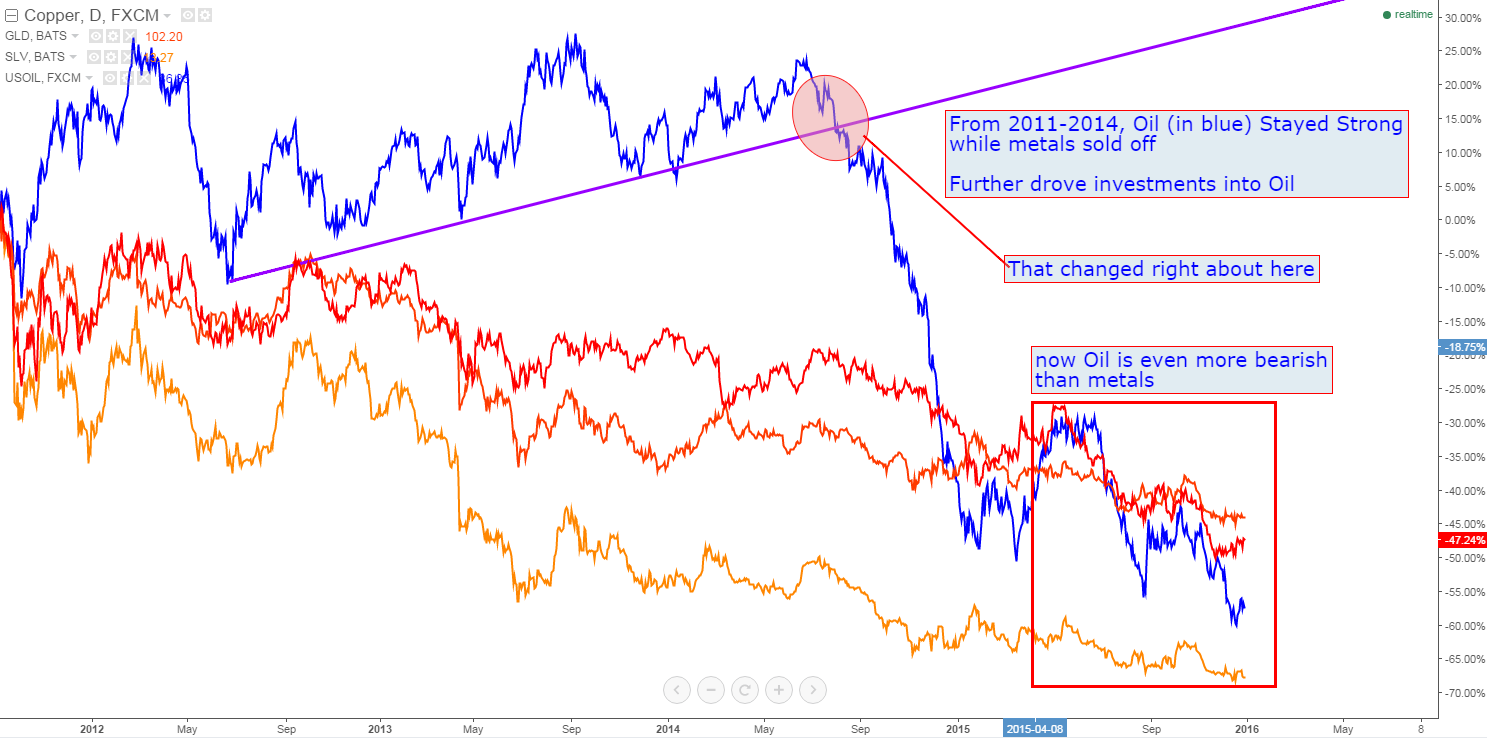

The selling in commodities was initially blamed on the larger slowdown being seen in Asia, positing that lower Chinese demand (and in-turn, lower demand from other Asian trade partners) was precipitating selling in these asset classes; but that would be a fairly disingenuous way of characterizing the move. The major move in Oil really started in June of 2014 after Oil had peaked just above $107.50; and Gold has been in a down-trend since the top was set in Gold prices in 2011, and Copper and Silver are both in similar positions after having been sold considerably since 2011. Chinese stocks were really just getting started on their most recent ramp as Oil prices began to crack. And Chinese stock prices ran up by about 150% as Oil was selling off (along with Gold, Silver, Copper, etc.).

Oil (in blue) compared to Gold (red), Silver (orange), and Copper (Yellow) since 2011

Created with TradingView; prepared by James Stanley

So, there is something larger going on here and the pain in commodities most definitely is not nor has it been 100% attributable to Asia. And that’s what’s worrying. Because one of the consequences of cheap money (low rates, ZIRP) is that investors take on more risk than they normally would. And with Oil prices staying so strong from 2011-2014 while the rest of the commodity world was trending lower, we saw quite a bit of that cheap money get borrowed in order to extract Oil. As long as Oil prices stayed strong, these producers could essentially play a carry trade of Oil/USD, borrowing cheap funds and investing in higher-yielding assets (like Oil). But as Oil prices started to come off in 2014, all of those carry trades began to feel pressure as energy producers felt their margins get squeezed by falling prices.

A more likely factor for this near-coordinated pain across the commodity spectrum is the low rate environment that has become commonplace over the past six years. Again, when rates are at zero (or close to it) investor behaviors change. And when every large Central Bank in the world is offering ‘extraordinary accommodation,’ this has a tendency to provide investors with a false sense of security. Combine that false sense of security with a dearth of ‘safer’ fixed-income investment options, and investors swallow up risk like it’s a vitamin. And as long as markets are continuing to go up, as long as prices are trudging higher, this is not a bad thing.

The Driver of Commodity Pain

This is what’s changed so drastically this year: The Fed no longer wants to offer ‘extraordinary accommodation’ to markets. Regardless of whether the December hike was a one-and-done or the beginning of a ‘gradual rise,’ the Fed has already shown their hand: They want tighter policy. No more punch bowl. And as rates move up, as opportunity costs in the investment spectrum change to reflect higher rates and tighter monetary conditions, those levered-up bets that investors made during the bullish-run begin to get squeezed massively (this is the painful side of the double-edged sword that is leverage).

And as prices in those levered-up markets begin to move lower, other investors holding long positions in those markets get squeezed and that precipitates even more selling, which can lead to a pain-chain of events that sees prices continue to dwindle lower despite any good news that may be seen as persistent selling pressure envelopes a market.

This tighter monetary environment brought on by the Fed combined with falling prices in many of these commodity makes for an even more daunting investment scenario around-the-world. These are the types of things that can raise red flags and get investors looking at how to position down-the-road. As in, if rates are moving up and expected to continue moving up for the foreseeable future, why take on long-term credit risk? If rates continue to move up, this is a sure-fire, almost locked-in loss for long-dated bonds. Rising rates means your lower-yielding coupons are worth less, so you’ll have to take a discount on that bond simply to close the position in the secondary market. A rising rate environment is a bond investor’s enemy, and with rates super low for so long, we’ve seen debt fuel massive moves in many commodity and equity markets. As rates move up, it’s rational to expect bets in those debt-fueled bull runs to come out of markets.

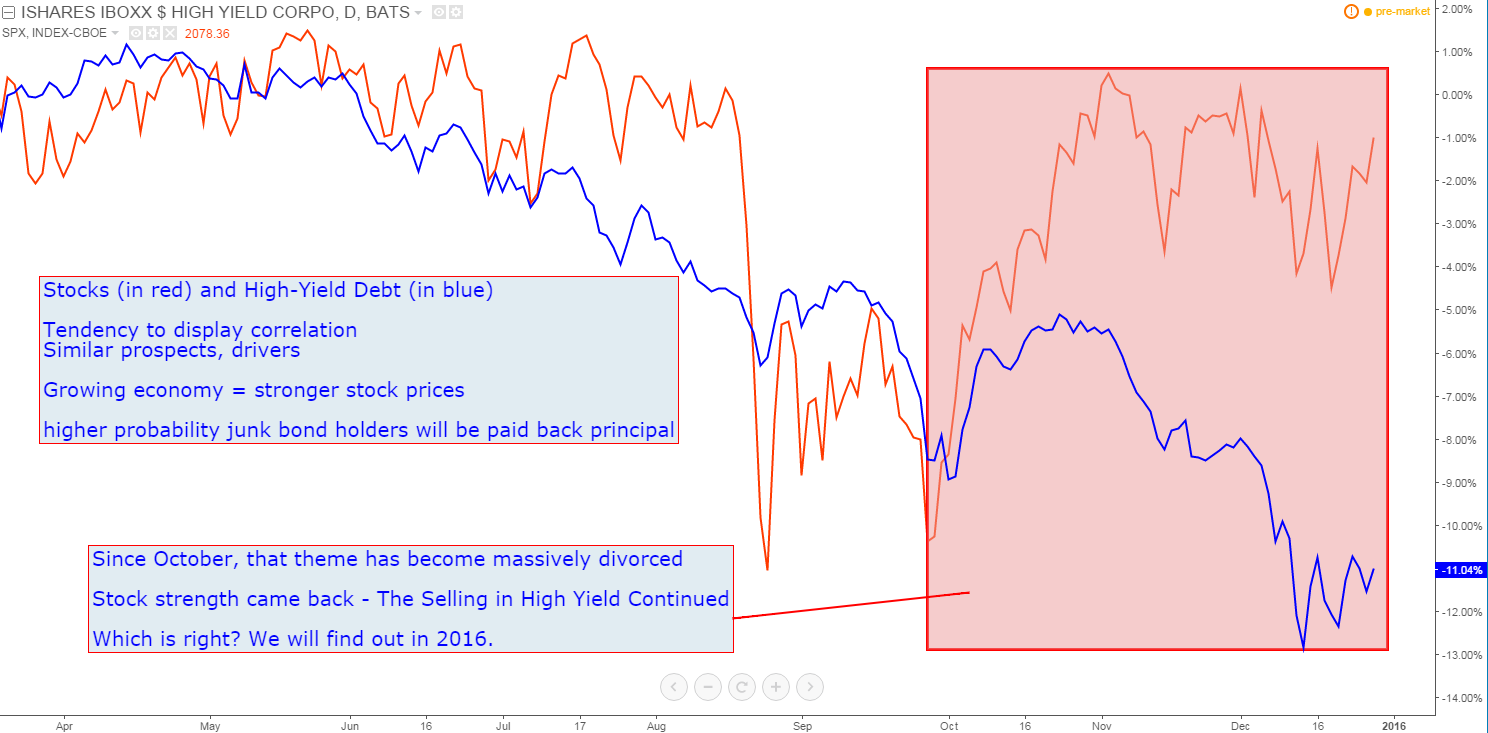

This is what we’ve been seeing in High Yield Debt over the past three months. Logically, high-yield debt and stock prices should display some degree of correlation; they have very similar drivers. If an economy is growing and everything is great, there is a higher chance that holders of junk bonds will be paid back their principal and, hence, rewarded for taking on the credit risk of a lower-credit quality issue. This type of environment is generally conducive for stocks too. But of recent, we’ve seen that correlation become massively divorced. When China’s Black Monday was hitting global markets on August 24th, we saw both markets sold massively as worries of a correction became prominent. But an entourage of Central Bankers talking up ‘looser for longer,’ was enough to bring equity markets back to life in the four months since. The problem is that high-yield debt markets have not followed, and this is what indicates that all is ‘not right’ we may be in for a tumultuous 2016. One of these themes is going to correct; the big question is which one:

High Yield Debt (in blue) v/s SPX (in red) Divergence Since October

Created with TradingView; prepared by James Stanley

The Consequences of a Continued Collapse in Commodity Prices

It’s not good. For a long time analysts expected strength in the American economy with lower oil prices. Lower oil/gas prices simply meant that there were a few more dollars in American’s pockets, and this meant that it would likely get spent on consumer goods considering the extremely low marginal propensity to save seen by American consumers. But a lot can change in 10 years, and the United States becoming a net producer of Oil could certainly have been that driving factor behind the change.

This is what makes commodities so incredibly bearish for next year, at least the early part, as there doesn’t appear to be a direct supply-demand transmission here. With the United States becoming a net producer of Oil and with OPEC sticking to their brisk production metrics; combined with many emerging markets feeling their own squeeze and reacting by drilling more and more oil out of the ground; supplies have not yet come down. And perhaps more to the point, this newly-built industry in the United States based around Oil exploration and Fracking are facing significant headwinds that’s leading to fewer jobs, less competition for what jobs are available (leading to slower wage growth – the Fed’s favored precursor to inflation), and slower overall economic growth.

This, of course, leads to lower stock prices if a Central Bank isn’t providing the burst of wind to the sails of the market. Which is what we have going into 2016 from the United States.

But lower stock prices aren’t the big worry here, as that’s more related to the contagion-effect that lower Oil/commodity prices may have. As in, many of those investors that took on debt to finance Oil exploration are likely having a difficult time paying it back. Many of those loans were issued when Oil was well supported above $75/barrel, and most of these investors expected prices to stay strong for a long time. But as prices have come down (and stayed there), servicing this debt has become monstrously difficult.

If we see more and more producers defaulting on that debt, it likely won’t stoke much risk-taking behavior from the banks and hedge funds that are taking those losses; and that’s where this theme can spill out from High-Yield to hit other debt markets, particularly United States Municipal Bonds which are looking extremely vulnerable to a continued rising rate environment. If we see pain in High-Yield move to pain in Muni’s, quite a few more people will become impacted, and this is what can lead to a loss of confidence in markets, and that’s a key ingredient to any major sell-off that the world has seen over the last 100 years. Markets are built on confidence, and as that confidence erodes, investors sell without regard to the loss that they might take; and this is why it only takes a few days/weeks/months to wipe away gains that took years and years to build.

Fear and Greed compel most human behavioral patterns, and when fear spreads throughout a market – look out.

You can see this expectation across the DailyFX desk going into 2016. We just published our Top Trade Ideas for next year, and you’ll probably notice that we’re looking at similar themes here. We don’t groupthink this stuff, we all write it individually and then find out what the others have written after the fact; so I was very surprised to see this correlation of themes across so many different styles of trading.

Yen strength is a very opportunistic way to play a larger risk-aversion theme and we discussed that in yesterday’s piece. John Kicklighter, David Rodriguez, Christopher Vecchio and Michael Boutros (as well as myself) are all looking to Yen strength next year as the Bank of Japan has been wedged between a rock and a hard place. Should risk aversion continue to develop around-the-world, we’ll likely see considerable Yen-weakness bets come out of the market as the Bank of Japan finds it increasingly difficult to continue extending and increasing QE when it’s showing few signs of working (and the economy is still close to deflation).

My top idea going into next year, and related to the expectation for a continued sell-off in Commodities, is for a correction in stock prices, and you're welcome to read about it in thie article, This may be the year that stock prices finally tumble. The S&P has basically put in a Doji formation this year as we’re ending the year fairly close to where we started. But we’ve seen rampant volatility throughout the year, so this isn’t ‘just’ a Doji, but a long-legged Doji, and that’s a prime candlestick setup for a ‘topping’ type of move. There have been seven instances of the S&P moving by less than 6% in a year since 1980; and the average move in the year after has been 24.63%. This makes logical sense, and it’s sensible to expect something similar going into next year, in one direction or the other.

But this isn’t the only indication of potential topping in the S&P. The level at 2,138 is extremely interesting as this is the 61.8% extension of the Financial Collapse, and not coincidentally, is but 1.4 handles away from the top set earlier in the year. Since that 2,137.1 top was set, the S&P has made continually lower-highs, which is yet another sign often indicative of topping.

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX