Talking Points:

- Today's FOMC meeting is an 'off-cycle' meeting without new economic projections or a Fed Chair Yellen press conference.

- Key aspect in policy statement today for US Dollar will be whether or not FOMC issues concern over inflation; if not, focus should be on timing of balance sheet normalization and next rate hike.

- See our Q3'17 forecasts for the British Pound, Euro, US Dollar, and more.

Upcoming Webinars for Week of July 23 to July 28, 2017

Wednesday at 13:45 EDT/17:45 GMT: Live Data Coverage: FOMC Rate Decision with Chief Strategist John Kicklighter

Thursday at 07:30 EDT/11:30 GMT: Central Bank Weekly

See the full DailyFX Webinar Calendar for other upcoming strategy sessions

The week truly begins for the US Dollar today, which was trading flat on the day at the time this article was written, even though the Federal Reserve is not expected to move on rates. After all, the July FOMC meeting is an ‘off-cycle' meeting, or one that won’t produce a new summary of economic projections (SEPs) and a press conference with Fed Chair Janet Yellen.

Accordingly, the policy statement will garner all of the attention. Given the steadfast support for a majority of Fed policymakers – particularly 2017 voting members – to raise rates again before the end of the year, it is possible that the Fed uses this ‘off-cycle' meeting to further prime the market for the implementation of their balance sheet normalization strategy, which was outlined at the June meeting in the “Policy Normalization Principles and Plans” augmentation.

The Fed intends to wind down its balance sheet with an initial reinvestment cap for US Treasuries at“$6 billion per month initially, and will increase in steps of $6 billion at three-month intervals over 12-months, until it reaches $30 billion per month.For payments of principal that the Federal Reserve receives from its holdings of agency debt and mortgage-backed securities, the Committee anticipates that the cap will be $4 billion per month initially and will increase in steps of $4 billion at three-month intervals over 12 months until it reaches $20 billion per month.”

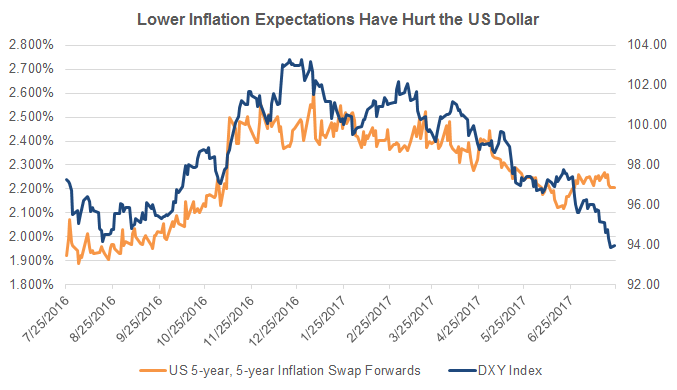

Chart 1: DXY Index versus US 5-year, 5-year Inflation Swap Forwards (July 2016 to July 2017)

The headstrong behavior by the Fed to plow ahead and continue with its desired tightening schedule could reawaken rate timing speculation, which has been decidedly dovish after recent weeks of poor economic data. The US Citi Economic Surprise Index closed last week at -52.6, down from -4.8 three-months prior. During this time, inflation expectations have dropped in parallel, with the 5-year, 5-year inflation swap forwards moving from 2.404% on April 28 to 2.207% on July 21. If the FOMC policy statement turns an eye to recently disappointing inflation readings, it may come across as a dovish blush to market participants.

Amid the lackluster US data performance and slump in medium-term US inflation expectations, the odds of a Fed rate hike by the December 2017 meeting have eroded steadily. At the end of last week on July 21, the implied probability of a 25-bps rate hike was 40.4%; three-months earlier, back on April 28, it was 46.7%. The timing of the next hike, per Fed funds futures contracts, has been pointing to March 2018.

Should the Federal Reserve’s July policy statement reveal the beginning of the normalization process (in say, September) and a reaffirmation of the desire to raise rates by the end of the year (in say, December), perhaps market participants will be forced to confront the divergence between what the Fed is saying it wants to do and the much more dovish interpretation that the market currently holds. If so, the US Dollar may just finally find a reprieve after its latest swing lower.

See the above video for a technical review of the DXY Index, EUR/USD, GBP/USD, USD/JPY, AUD/JPY, CAD/JPY, EUR/JPY, Gold, Crude Oil, and US yields.

Read more: USD Steady Ahead of FOMC Tomorrow; AUD/JPY, CAD/JPY Longs Primed

--- Written by Christopher Vecchio, Senior Currency Strategist

To contact Christopher Vecchio, e-mail cvecchio@dailyfx.com

Follow him on Twitter at @CVecchioFX

To be added to Christopher's e-mail distribution list, please fill out this form