The DAX Index, which tracks the top 30 companies in Germany, is one of the most important and respected indicators of the world’s economic health. DailyFX’s DAX definitive guide is here to help you learn everything there is to know about the history of the DAX 30, as well as where it stands today and where it might be heading in the future.

- How is DAX faring under the unprecedented circumstances surrounding the coronavirus?

- How have cultural and social issues affected the stock of DAX companies over the last 20 years?

- What effect have conglomerates and business acquisitions had on the DAX?

- Which companies could break into and drop out of the DAX over the next decade?

- Which companies have remained on the DAX since its inception – and why?

- Comparing the DAX to international stock indices

- Conclusion

Germany, as the largest economy in Europe and the world’s fourth-largest economy, is a crucial player in the global economic engine. As such, it should come as no surprise that the DAX 30 Index has historically included many of the world’s largest and most well-known companies. Volkswagen, BMW, Siemens, Adidas, and Bayer are just a few of the household names that have made a home for themselves on the German DAX over the decades.

As the DAX is a stock exchange index of top companies that tracks factors such as capital gains and dividends when calculating stock prices, it can give a very clear picture of the health of Germany’s, Europe’s, and the world’s economies. DAX 30 companies typically have a presence in every corner of the globe, employ tens of thousands of people apiece, and are often vital cogs in global trade networks and supply chains.

As such, DAX stock prices and market caps are strongly influenced by global events, as has been seen throughout its 32-year history. Owing to the high levels of liquidity, long trading hours, and tight trading spreads, trading on DAX 30 companies is a popular and widespread activity for individual traders and large firms around the world.

How is DAX faring under the unprecedented circumstances surrounding the coronavirus?

Before we dive into our comprehensive introduction to DAX, it’s important that we address the giant economic elephant in the room: the coronavirus, also known as COVID-19. The DAX has been far from immune to the coronavirus stock market plunge that has wiped trillions of dollars off the market caps of indices and companies in every corner of the globe.

The stock market coronavirus upset has been the result of many factors, including disruption to supply chains, widespread layoffs, mass redundancies, and huge levels of uncertainty. While indices around the globe will likely rally in the near-future, coronavirus has guaranteed that unpredictability is the current order of the day.

In the middle of March 2020, when countries began hiking up their responses to the spread of the virus, the DAX suffered one of the worst trading weeks in its entire history, losing close to 10% of its value in one week and closing at a major recent low of 7990 on 19 March. This represents the quickest and most dramatic drop in the history of the DAX Index.

Of course, not all companies have proven to be equally affected by the coronavirus stocks scare. Some have proven more resilient, largely due to the industry they belong to and how vulnerable that industry is to coronavirus-related disruption. The most obvious casualties were the travel and tourism industries. Lufthansa, Germany’s largest airline and a member of the DAX 30 since its inception, lost 41% of its value in the second half of March 2020, making it by far the most heavily impacted company on the index.

However, other companies, representing very different industries, have also suffered from the coronavirus financial crisis. Deutsche Bank AG, in keeping with other major financial institutions around the world, saw its share price plummet throughout March, reaching an all-time-low of €4.87 per share on March 12. The financial industry has suffered from the chaos for a large number of reasons, with one of the main ones being that investors are pulling out of private banks and fleeing toward safer options such as government-backed treasury bonds.

However, pharmaceutical giants on the DAX 30, such as Bayer and Merck, have been relatively unaffected by the coronavirus crash. Despite some modest declines in the middle of March 2020, both companies quickly rebounded, and look set to ride out the turmoil in good shape. This is, in large part, due to the fact that the vital medical products these companies provide, such as vaccines, antibiotics, antiviral drugs, and biotechnologies, are all massively in demand during a global pandemic of this scale.

As the crisis unfolds, it is possible that certain DAX 30 companies that are better placed to adapt to the new normal will thrive, will others will fall. If we take the global pivot to remote working as just one example, it becomes clear which companies are better placed to weather the storm.

Companies that are heavily focused on the provision of digital services, such as Wirecard, SAP, and Deutsche Telecom, will be able to continue running large parts of their current operations. However, companies that focus heavily on physical manufacturing and exporting, such as BMW, Beiersdorf, and Infineon, will likely suffer as a result of social distancing measures.

Of course, it is impossible to say definitively how the DAX will perform as the crisis unfolds over the coming months. The German government’s aggressive stimulus attempts may lift the index up or compounding crises may drag it down. Only time will tell.

How have cultural and social issues affected the stock of DAX companies over the last 20 years?

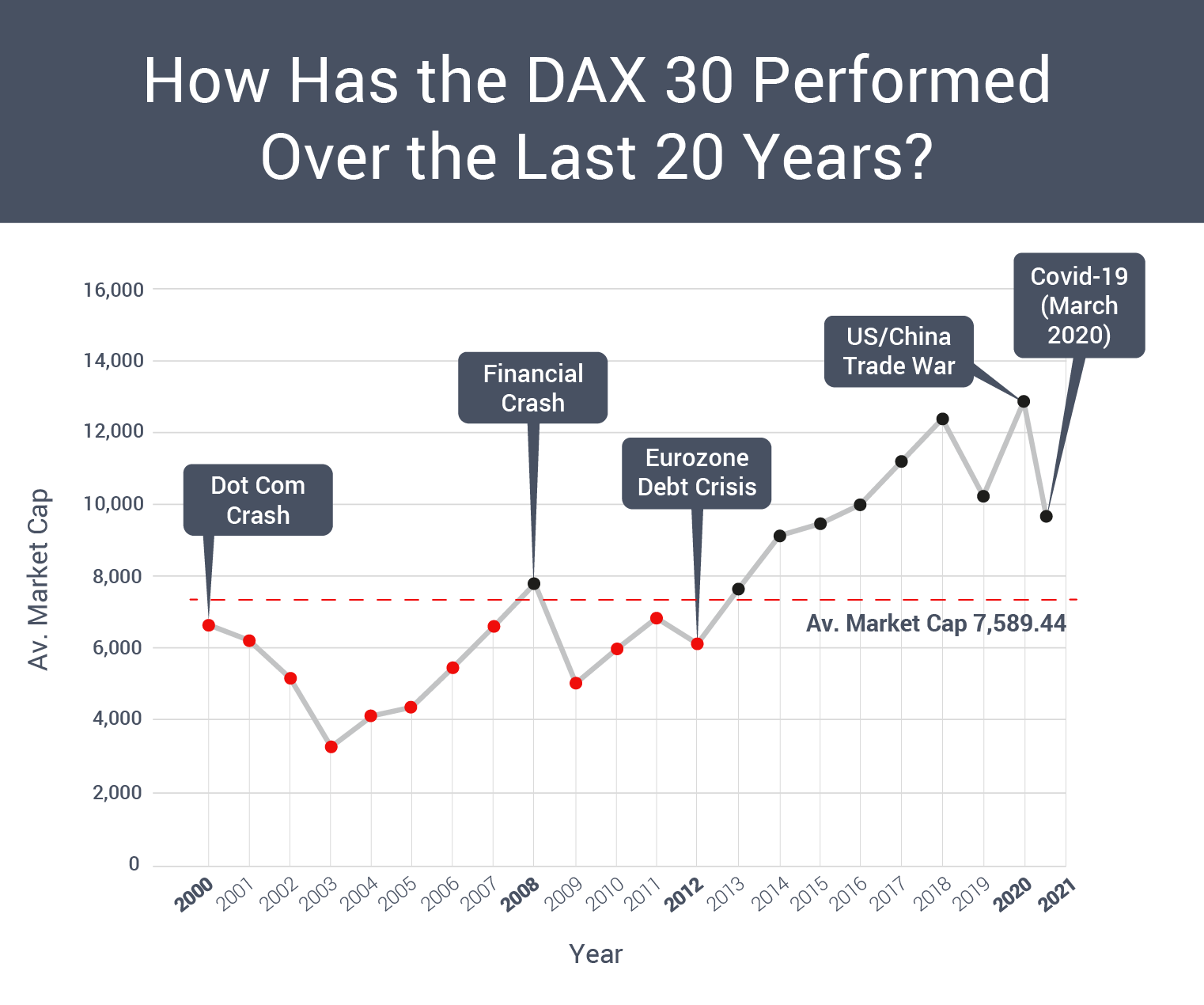

Since the DAX 30 Index was first founded in Frankfurt in July 1988, its performance and progression have seen a lot of ups and downs, in much the same way as similar major indices like the Dow Jones Industrial Average. There have been several peaks and busts in the global economy in the 32 years since the DAX came into existence, including the early 90s recession, the Japanese Asset Price Bubble, Black Wednesday, The Asian Financial Crisis, the Dot Com Bubble, and the crash of 2008. As all of these events are global economic developments, it should come as no surprise that the DAX, which represents the largest companies of one of the world’s most globalized economies, has always been deeply impacted.

Let’s take a closer look at the ups and downs of the DAX exchange throughout its history.

1982-1990: Tumultuous Beginnings

The DAX index was first launched on 1 July 1988 in Frankfurt, the economic and financial epicenter of Germany. The goal was to provide a representative snapshot of the German economy that the whole world could rely on (although many people did and still do believe that the top 30 German companies do not in themselves represent the health of the broader economy).

However, not all of Germany was included in this measure. Owing to the existence of the Iron Curtain, Germany was divided into two countries, the Federal Republic of Germany and the Soviet-controlled German Democratic Republic, with the DAX representing the former. For the first few years of its existence, the West Germany DAX grew steadily, rising in market cap by 60% by 1988.

However, the following year was to cause the first major upset for the index. With the fall of the Berlin Wall and subsequent collapse of communism in November 1989, the process of merging the poorer East German states with the wealthier West German states had commenced.

The process caused considerable economic and political turmoil with the newly reunified Germany. This was reflected in the DAX, which saw its value decline by 16% in the first seven weeks of 1990. However, once the dust had settled, the recovery was fairly swift.

2000: Dot Com Bubble

20 years after the fact, the Dot Com Bubble still looms large in the minds of analysts as an example of the dangers of hype when it comes to trading. The late 1990s saw an explosion in the use of the internet in households around the world and the birth of Silicon Valley as the center of the global tech and knowledge economy.

Internet companies founded during this period were carried high by a wave of euphoria over what people thought the internet would bring, with some companies seeing their shares double in value in a single day, despite no news being announced about the company whatsoever. While much of the dot com bubble was centered on Silicon Valley, the DAX was by no means immune.

The jaw-dropping bull market convinced millions of Germans to invest in the DAX in the belief that the party would never end. At the height of the bubble in 2000, 12 million Germans owned DAX-listed stocks, an all-time-high that has never been seen since. Deutsche Telecom, one of the largest companies on the DAX, was forced to raffle off shares throughout 2000 because demand was so high.

Tech companies on Germany’s dedicated tech stock index, the TecDax, saw similar valuation rises to those being observed in Silicon Valley at the time. For many, it seemed like the bubble would keep on growing.

2003: Dot Com Bust

Of course, such a meteoric rise was never going to be sustainable for long. With investors around the world waking up to the fact that many of the internet companies that had been given 10- or 11-figure valuations weren’t actually creating any wealth or value at all, a plummet crept up slowly before crashing down. Investors began moving huge amounts of liquid capital out of high-performing tech stocks and into low performing traditional stocks at the end of the year 2000.

This exodus was compounded by a number of events, including the Enron scandal, the WorldCom Scandal, and the September 11 Attacks. By the end of 2002, global tech stocks from the Dot Com Bubble had lost $5 trillion in market capitalization, leaving a trail of bankruptcies in their wake.

DAX historical data shows that the Dot Com Bubble burst hit it especially hard. After reaching its then-highest level ever of 8,136.16, it closed at a low of 2,202.96 points on 12 March 2003, when the worst after-effects of the bubble were being felt. Stocks on Neuer Market, then Germany’s leading tech stock exchange, lost 98% of their value between 2000-2003, while former DAX companies such as Epcos and MLP were de-listed due to their market cap falling to new lows.

2003-2008: Recovery and Boom

The years following the collapse of the Dot Com Bubble were largely a period of uninterrupted success for the DAX. Driven largely by a global market rally that saw demand for high-quality German exports, particularly those produced by top DAX companies such as Volkswagen and Siemens, soar to previously unseen heights.

By July 2007, the DAX had climbed to a new all-time peak of 8,151.57 points and continued to rise. Shortly after the DAX celebrated its 20th birthday on the Frankfurt Stock Exchange in July 2008, the index recorded its highest ever daily gain, growing by an astonishing 11.4% in just a few hours.

The height and hubris of the pre-recession boom are perhaps best epitomized by Volkswagen, which for a brief time became the world’s most valuable company in 2008 when stock prices rose to more than €1000 ($1078) per share.

Some of the best-placed companies during the boom were financial industry giants such as Deutsche Bank and Allianz, which saw their caps skyrocket in the same way that US giants such as Lehman Brothers did.

2008: Recession and Bust

As we all know, the height of the boom was a short-lived one indeed. Sparked by the subprime mortgage crisis in the US, the Great Recession of 2008 was, by most measures, the most severe economic downturn since the Great Depression in the 1930s. Some of the biggest names in banking went under, and millions of people lost jobs and life savings.

Germany, despite extensive government bailouts to save the biggest German banks, which were estimated to have cost around €500 billion, was particularly hard hit. Between 2007 and 2008, the DAX lost more than half of its value, plummeting 55.9% and bottoming out at 3,585.1 points.

Several companies that once occupied prominent positions on the DAX either exited the index for good or went bust as a result of the crisis. Hypo Real Estate, Deutsche Postbank, and TUI all bowed out after suffering crushing declines in stock prices, largely due to their respective industries – mortgages, banking, and travel – all being decimated by the recession.

2011: Black Monday

While some countries saw their stock markets bounce back dramatically once the worst of the crisis had passed, the case was not quite the same for Germany and the DAX. Recovery was one of the most sluggish in the Eurozone, although admittedly nowhere near as bad as the recoveries seen in Italy or Spain. However, slowly but surely the DAX began to rise again, hitting 7372.24 points in June 2011.

However, the DAX was in for another brutal fall in the August of that year, when fears over a poor post-recession recovery began to bite. By July 2011, the DAX began shedding points as investor concerns started to rise amid the mounting Eurozone Debt Crisis, with many fearing that the astonishing levels of toxic debt accrued by banks in Italy and France would bring down the Eurozone altogether.

However, the catalyst for what followed came from across the Atlantic Ocean. On 6 August 2011, the global credit rating agency Standard and Poor’s downgraded the United States’ credit rating from AAA to AA+, warning that a poor post-2008 recovery had threatened confidence that the world’s largest economy could pay its debts.

This rating downgrade turned out to be the trigger for a massive selloff as investors began to fear another global recession. The following Monday, known as ‘Black Monday’, stocks around the world began to nosedive. The DAX lost 5.8% in a single day and continued to decline until 5 September 2011, when it closed at a low of 5246.20 points.

2013-2018: (Almost) Uninterrupted Growth and a Record Bull Market

Black Monday never did trigger the global recession that investors feared, and things began to return to growth not long after. While growth across the Eurozone continued to be shaky, Germany spent much of the following six years leading the pack, with the DAX going from 5246.20 points in 2011 to a then-record high of 13,559.60 on January 23, 2018.

Thanks to a booming German economy and the ability of once-troubled DAX companies like Volkswagen and Deutsche Bank to regain their reputations as some of the most trusted and quality brands in the world, the DAX saw some of the most sustained bull markets in its entire history.

While the record growth recorded in this period is in keeping with what we have seen in other markets, with the FTSE 250 and S&P 500 both seeing record bull runs and reaching new heights in terms of market capitalization, the DAX did suffer from a few small hiccups during this time.

This first of these was in early 2013, when interest rate cuts from the ECB to an all-time-low of 0.25%, prompted by sluggish Eurozone growth, prompted investors to flee the DAX. However, this was short-lived, and the ECB rose rates again in May that year, prompting a rise that remained virtually uninterrupted until June 2015.

It was during this time that the Greek Debt Crisis, during which Germany held the largest amount of Greek debt, prompted a mass sell-off when fears arose over Germany’s ability to recover its losses. However, Germany was able to lead the European Commission to strike a repayment deal with Greece, and fears quickly subsided, allowing the DAX to continue to once again discover record heights.

2018: Trade Wars and Uncertainty Bite

Despite heading into 2018 looking stronger than ever, underlying problems were mounting. While the Eurozone had seen some of its strongest growth of the decade during the first few months of 2018, things began to take a turn for the worst in the middle of the year. Rising debts, fears of an Italian banking crisis, traumatic restructuring plans for German financial giants such as Deutsche Bank and Commerzbank, and mounting uncertainty over Brexit negotiations all began to take a toll on the DAX companies.

However, the major blow again came from outside of Europe. The Trump Administration’s mounting trade war with China came to a head in the summer of 2018, when both countries placed successive tariffs on each other’s exports in June, July, August, and September. By the end of September, both countries had placed hundreds of billions of dollars worth of tariffs on each other’s exports, with rates on some goods reaching 25%.

During the same time, the US had also threatened to slap tariffs on German automobiles and car parts, in a direct threat to some of the biggest names on the DAX like Volkswagen and Daimler, the company behind Mercedes.

While those specific threats did not materialize in 2018, the conflict between the US and China was enough to ensure that 2018 became the worst year for the DAX since the Great Recession. Between January and December of 2018, the DAX lost 18% of its value, representing around $300 billion. The worst performers were Deutsche Bank, which lost 56% of its market capitalization, Covestro, which lost 49.8%, Continental, which also lost 49.8%, Bayer (-40.9%), Deutsche Post (-39.8%), Daimler (35.2%), and Volkswagen (16.5%).

While the poor performance of Deutsche Bank was set in motion before the trade war reached its peak, the other casualties are a direct result of it. Carmakers such as Daimler and Volkswagen relied heavily on exports to China and the United States, and the weak demand for imports triggered by the trade war meant that they were the first to suffer. Meanwhile, pharma giants like Bayer and Merck saw their supply chains in China majorly disrupted by the turmoil, which further contributed to their devaluations.

Most significantly, the turmoil of 2018 fired a warning shot to the global economy, reminding investors and traders just how closely interconnected the world really is.

2020: COVID Chaos

Just a couple of weeks before the COVID-19 virus caused mass selloffs in stock markets across the world, things had literally never looked better for the DAX. Despite generally weakening economic data coming out of the country, the DAX hit a high of 13,795.24 points on February 17, 2020, back when there was a general consensus that the coronavirus was an isolated, easily contained phenomenon.

However, as we have seen, such attitudes did not last long. As Europe became one of the regions hardest hit by the virus and began implementing sweeping lockdowns and workplace closures, the DAX went into freefall and lost an unprecedented 6000 points in the space of just four weeks, while major players on the DAX such as BMW and Lufthansa have responded to the crisis with heavy layoffs.

Since a low point in late March, the DAX chart has rebounded a little. However, it is clear that the turmoil caused by the virus is a long way from over, making it impossible to say how the index will perform in the coming months. One thing is certain is that now is a very interesting time to be following DAX 30 realtime data.

What effect have conglomerates and business acquisitions had on the DAX?

Source 1: Macrotrends

Source 2: Bloomberg

Over the course of its existence, the DAX historical data has proven itself to be mercurial, with its size, industry composition, and membership changing frequently. Many companies have dropped out of the DAX after decades of membership, often because their market capitalization has fallen to a point where they were no longer ranked among the top 30 German companies. Some companies have dropped out of the DAX because they were in deep financial trouble.

Many longtime DAX 30 members left the index because they merged with or were acquired by a rival company. Understanding the processes and forces that shape the DAX index today is vital for any would-be DAX trader. With that in mind, let’s take a closer look at the long and sometimes complicated history of DAX mergers, acquisitions, takeovers, and dropouts.

Biggest DAX Mergers & Takeovers

When it comes to companies that are at the vertex of one of the most valuable stock indices in the world, sometimes the only way to continue growing is to merge with similarly sized competitors or to allow themselves to be swallowed up entirely. The German DAX index has a long and storied history of mergers and takeovers that have seen some of the biggest companies on the index pool together to become truly global giants.

As mergers and takeovers become an increasingly common feature of the business landscape across the globe, an understanding of the processes and considerations that have fueled the biggest DAX mergers and takeovers in history is vital for anyone looking to become a DAX trader, or indeed anyone already operating in that market index. Without further ado, here is a list of the most significant mergers and takeovers to have ever taken place on the DAX 30 Index.

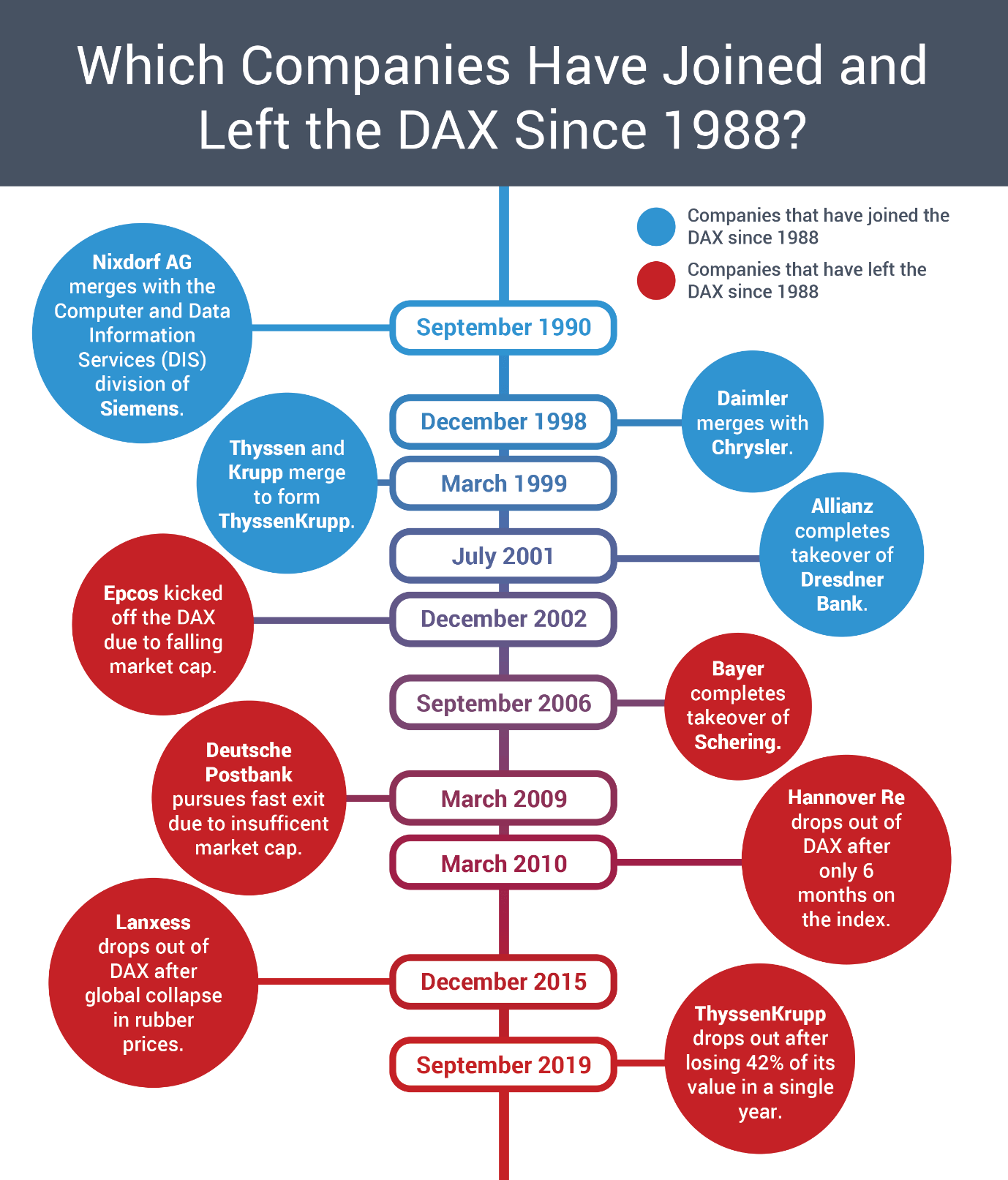

- September 1990: Nixdorf AG merges with the Computer and Data Information Services (DIS) division of Siemens. Just as Siemens was beginning to ramp up its IT capabilities, they made a splash in financial headlines around the world by acquiring Nixdorf, then Europe’s largest IT company and itself a prominent DAX index member. Siemens merged Nixdorf with the DIS department of its own company, retaining most of the resources and staff.

- December 1998: Daimler merges with Chrysler. Daimler’s merger with US auto icon Chrysler was, at $35 billion, the largest industrial merger in history at the time. Touted as a ‘marriage of equals’ at the time, the merger was designed to help Daimler corner the US market whilst offering both companies protection from Japanese competitors. However, DaimlerChrysler was not a match made in heaven, and the Chrysler division was sold off to the private equity group Cerberus nine years later for just $7.4 billion.

- March 1999: Thyssen and Krupp merge to form ThyssenKrupp. Both Thyssen and Krupp were titans of the steel industry, with roots in Germany stretching back centuries. Despite this, both were struggling to fend off competition from US and Asian producers, leading to their multi-billion-dollar merger in 1999, after more than a decade of negotiations.

- July 2001: Allianz completes takeover of Dresdner Bank. DAX lifer Allianz announced its $20 billion takeover of Dresdner Bank in 2001 as one of the most important deals of the decade. Allianz had hoped that merging with a veteran of the German banking industry would allow it to branch out into banking. However, this was another short-lived dream, with Allianz selling Dresdner Bank to Commerzbank for $14 billion in 2008, after announcing it would be returning to its ‘core’ business of insurance.

- September 2006: Bayer completes takeover of Schering. Bayer’s takeover of the Berlin-based pharma company best known for inventing aspirin, Schering, was the result of bitter wrangling with its fellow DAX-listed competitor Merck. Both companies were engaged in an aggressive and lengthy competitive bidding process to secure the merger with Schering, with Merck eventually acquiescing after Bayer offered to buy Merck’s shares at a greatly inflated price. All told, the takeover is estimated to have cost Bayer around $20 billion.

DAX Dropouts

The DAX 30 is undeniably an exclusive club, one that only the largest, richest, and most dynamic German companies are able to join. Due to the very high standards for membership, it is unsurprising that there are plenty of companies that have fallen out of the DAX over the decades. The most common reason that DAX listed companies leave the index is that their market capitalization falls to a point where they can no longer be considered one of the top 30 most valuable companies in Germany. Sometimes their market cap does not fall at all, but they are instead overtaken by another, faster-growing company. With that in mind, here are some of the biggest DAX dropouts from the past couple of decades.

- Epcos: The German electronics manufacturer Epcos enjoyed a fleeting moment on the DAX index, entering it for the first time in February 2000, before being kicked off again in December 2002 due to investor jitters sending its market cap down several percentage points.

- Deutsche Postbank: Not long after being sold to Deutsche Bank, Deutsche Postbank was forced to pursue a fast exit from the DAX in March 2009 due to its inadequate levels of market capitalization. Postbank’s market cap didn’t actually fall in this case, but changes to DAX rules pertaining to how market cap is calculated meant that Postbank no longer met the requirements.

- Hannover Re: Hannover Re, one of the largest reinsurance groups on the planet, had one of the shortest stints on the DAX in its history. After replacing Deutsche Postbank in March 2009 and entering the DAX for the first time, it found itself out in the cold again six months later, to be replaced by Infineon Technologies.

- Salzgitter: One of Europe’s largest steel producers, Salzgitter entered the DAX for the first time in 2008, only to find itself out of the DAX in June 2010 and replaced by a prominent competitor, HeidelbergCement.

- Lanxess: The world’s largest producer of synthetic rubber, Lanxess found itself barreling out of the DAX in September 2015, after building overcapacity in the rubber market saw consumer demand for its products nosedive. The company now sits on the M-DAX index of medium-sized companies.

- K+S: After becoming the first commodity stock on the DAX 30 in history in 2008, falling market capitalization resulted in this 121-year old fertilizer company making an exit in September 2015.

- Commerzbank: As Germany’s second-largest lender, pundits expressed surprise when Commerzbank was booted out of the DAX in September 2018, following a chaotic restructuring process and an aborted attempt at a merger with Deutsche Bank.

- ThyssenKrupp: After a dramatic drop in share prices of 42% in a single year, struggling industrial conglomerate ThyssenKrupp bowed out of the DAX for the first time in its history in September 2019, marking one of the most significant DAX changes in history.

DAX Shopaholics

Many of the largest acquisitions in the history of the DAX are the work of just a handful of companies. While acquisitions, in which a typically larger company takes majority ownership of a smaller one and adds it to its portfolio, have been a common feature of the business landscape for decades.

Source 1: Crunchbase Source 2: Crunchbase

Source 3: Crunchbase

While evidence suggests that the rate of acquisitions has increased dramatically in the decade following the 2008 crash, some of the DAX’s largest and most longstanding companies have been pulling off multi-billion-dollar acquisitions since long before then. Here are the biggest shopaholics on the DAX today.

Siemens: Electronics and telecommunications giant Siemens leads the pack by a considerable stretch, with a total of 65 acquisitions under its belt. Although it has since divested itself of 21 major assets, Siemens remains the biggest shopaholic on the DAX 30 Index, and one of the most popular options for people trading DAX 30 index shares. As a global engineering and electronic conglomerate, Siemens serves a huge variety of customers, which helps to explain the considerable diversity of its investment portfolio spanning numerous industries. While Siemens's acquisitions are too lengthy to list here, we’ve provided a roundup of the biggest ones in the company’s 173-year history.

- 1991: Nixdorf Computer AG. Prior to the acquisition, the computer manufacturer was the largest IT company in Europe. Once Siemens acquired it in a hostile takeover for an undisclosed sum, it became Europe’s largest computer company.

- 1998: Westinghouse Power Generation. The US energy company Westinghouse was acquired by Siemens for $1.5 billion, significantly boosting its presence in the realm of energy technology.

- 2007: Dade Behring. This American clinical diagnostics company was snapped up by Siemens for a cool $7 billion in 2007, marking Siemens's biggest step yet into the world of medical technology.

- 2007: UGS Corp. Citing a need to beef up its industrial software portfolio, Siemens shelled out $3.5 billion to buy this Texas-based developer of manufacturing simulation technologies.

- 2012: Invensys Rail. The rail division of Invensys, a British engineering conglomerate, was purchased by Siemens for £1.7 billion in 2012 as part of a wider shift towards strengthening its core business activities, namely the development of infrastructure technologies.

- 2015: Dresser-Rand Group. The heavily indebted energy firm Dresser-Rand was bought by Siemens for $7.6 billion in cash in 2015, resulting in Siemens announcing that it would make Houston, where Dresser-Rand is based, the center of their oil and gas operations.

- 2016: Mentor Graphics. Siemens continued to bolster its industrial software portfolio by snapping up Mentor Graphics for $4.5 billion in 2016.

Volkswagen Group: While automobile conglomerate Volkswagen has a more modest number of acquisitions, the companies it has absorbed are some of the most prestigious and well-known brands in Europe. What is notable about Volkswagen’s acquisition strategy is just how focused it is. All of the company’s acquisitions consist of commercially successful, well-known European car brands with a strong reputation. In the early years of acquisitions, Volkswagen focused on affordable family car brands.

However, at the turn of the 21st Century, they changed tack and focused on aggressive buyouts of prestige luxury auto manufacturers. Here is Volkswagen Group’s acquisition history, in a nutshell.

- 1965: Auto Union. Before Audi was Audi, it was Auto Union, East Germany’s largest car manufacturer. Volkswagen, a West German company, began acquiring the assets of Auto Union in the early 1960s, gaining majority control in 1965.

- 1986: SEAT. The popular Spanish auto manufacturer was acquired by Volkswagen when the group obtained a 51% ownership stake in 1986. By 1990, Volkswagen acquired 99.99% ownership, making SEAT the first non-German company to become a wholly-owned subsidiary of Volkswagen.

- 1994: Skoda. Czech auto manufacturer Skoda was first partially bought up by Volkswagen in 1991, when the Czech government allowed them to buy a 30.1% share. While this original purchase was designed to ease Skoda’s troubles following the collapse of communism and state-backed support, Volkswagen continued to show a strong interest in Skoda, acquiring majority ownership in 1994.

- 1998: Bentley, Lamborghini, and Bugatti. As part of a concerted push to capture the luxury market, Volkswagen went all out in 1998, spending billions of dollars to acquire Bentley, Lamborghini, and Bugatti, some of the most prestigious automobile brands in the world.

- 2008: Scania. In a move that was unexpected by many financial analysts and pundits, Volkswagen moved rapidly to acquire a 36.4% share of the Swedish truck manufacturer Scania in 2007, before upping their share to 70.94% the following year. The acquisition marked Volkswagen’s first foray into the industrial vehicle sector.

- 2012: Ducati and Porsche. Porsche and Volkswagen have been tight-knit for over a century, but it wasn’t until 2012 that Volkswagen finally achieved its dream of acquiring majority ownership. That same year, they also acquired outright ownership of the Italian high-end motorcycle manufacturer Ducati.

Deutsche Post: Until just a couple of decades ago, Deutsche Post, which operates under the trade name Deutsche Post DHL Group, was a strictly domestic operator. With its origins as the state-backed postal service Deutsche Bundespost, founded in 1947, the company had a minimal presence outside of Germany until it embarked upon its first wave of global acquisitions at the turn of the 21st Century. Here is the full list of Deutsche Post’s acquisitions to date:

- 1999: Van Gend & Loos. Deutsche Post kicked off its international push with the acquisition of Van Gend & Loos, the oldest and largest distribution company in The Netherlands, in 1999.

- 2000: Danzas. Hot on the heels of their Dutch acquisition, Deutsche Post moved quickly to snap up the Swiss-based global distribution company Danzas in 2000. The company has since been transformed into the DHL Global Forwarding Division.

- 2002: DHL International and Airborne Express. Deutsche Post cemented its position as a global courier and delivery service by acquiring majority ownership of Seattle-based Airborne Express. The company then promptly merged Airborne, Danzas, and Van Gend & Loos into DHL International.

- 2005: Exel. In 2005 Deutsche Post beefed up its logistics capability by acquiring the UK corporate logistics giant Exel for $6.73 billion.

- 2010: Nugg.ad. In a move intended to bolster Deutsche Post’s move into the e-commerce market, they acquired the digital ad targeting platform Nugg.ad for an undisclosed sum in 2010.

- 2011: AdCloud. In a similar vein the online search engine ad agency AdCloud was acquired the following year.

- 2012: All You Need GmbH. For an undisclosed sum, Deutsche Post snapped up the Berlin-based grocery delivery platform All You Need. However, the acquisition was short-lived, with DP selling it on a few years later.

- 2014: StreetScooter GmbH. In a somewhat unorthodox move, Deutsche Post acquired majority ownership of the electric scooter company StreetScooter, as part of a move to reduce their carbon footprint.

- 2016: UK Mail. Deutsche Post cemented its grip on Europe’s largest e-commerce market, the UK, in 2016 when it acquired the independent postal giant UK Mail for $315.5 million.

Which companies could break into and drop out of the DAX over the next decade?

As we have seen, membership of the DAX is by no means a lifetime guarantee. Keeping a foothold in the prestigious index requires an ability to constantly fend off the competition and stay at the top of your game. Many of the companies that have found themselves booted off the DAX were not necessarily performing poorly. Rather, the competition proved itself to be more dynamic.

Predictions on who will leave and who will enter the DAX in the future can be tricky, given that many of the past exits and entrances have come as a surprise to even the most seasoned financial pundits. However, if one pays attention to the market forces that are currently reshaping the German economy, it becomes possible to identify certain clues and trends that may tell us more.

Source 1: Bloomberg

Source 2: Delivery Hero

Source 3: Scout24

Source 4: Statista

Source 5: Lufthansa Group

Source 6: BWM Group

Source 7: Infineon

With this in mind, we examine some of the common predictions for which companies are most likely to leave the DAX over the next decade, versus those that are most likely to enter the DAX within the next ten years.

Who Will Leave the DAX?

Deutsche Lufthansa AG

Long before the COVID-19 drama wiped out the bookings and profits of airlines around the globe, Germany’s flag carrier Lufthansa was facing existential troubles. The company has posted a number of profit warnings over the past few years, with one of its worst coming in Q1/2019 when the airline suffered a record quarterly loss of €336 million ($380 million) due to an ongoing wrangling with German tax authorities and biting competition from low-cost airlines.

Throughout the full year of 2019, Lufthansa was the single worst performer on the DAX Stock Exchange, with share prices falling by a total of 44.42% between January and December. All of this does not bode well for the future of Germany’s flagship airline, which has already gone through a traumatic decade of restructuring, layoffs, and losses. While the mere fact that Lufthansa is still on the DAX 30, as of this writing, is a testament to its resilience, the recent disruption to the airline industry caused by the coronavirus may well prove to be the final nail in the coffin for this once-dynamic company.

BMW AG

There are few market hawks out there who would deny the notion that now is not a good time to be a German auto manufacturer. Owing to a number of factors, demand for high-end German auto exports has plummeted in the past couple of years, whilst threats such as the coronavirus and Brexit are placing a serious squeeze on the complex supply chains of these massive companies. While some, such as Volkswagen, clearly have a diversified enough portfolio to weather such storms, BMW AG has not.

The company’s DAX stock price lost a total of 27.79% of its value in 2019 after numerous profit warnings sent investors heading to the doors. The company started off last year by issuing a severe profit warning and announcing that it would be seeking to make more than $13 billion in cuts, with personnel, operations, and assets all being affected. The company’s relatively narrow portfolio, which focuses overwhelmingly on top-tier luxury cars, has proven intensely vulnerable to market uncertainty. It is for these reasons that BMW’s chances of remaining on the DAX for another decade do not look great.

Infineon Technologies AG

The semiconductor manufacturer Infineon should, on the surface of things, be in a good position to spend the 2020s living it up on the DAX. There is virtually zero chance of the global demand for semiconductors, which are vital for the production of microchips, waning anytime soon. However, Infineon has had a bad couple of years, and is now in a situation where its continued membership of the DAX stock index is looking increasingly untenable.

The company saw 29.92% of its share value wiped out in 2019, following a chaotic first quarter in which revenues dropped by close to 20%, which Infineon attributed to plunging demand for semiconductors from its biggest consumer market, China, which has ramped up production domestically rather than relying on imports.

This, coupled with scandals such as the ROCA incident of 2018 which saw security flaws in Infineon products leading to the personal data of hundreds of thousands of people being exposed, does not bode well for the future. Unless Infineon can fend off foreign competition and get its act together, it may struggle to hold onto its position on the DAX for much longer.

Who Will Join the DAX?

Delivery Hero SE

Founded in 2011, the multinational online food delivery platform Delivery Hero is one of the most promising potential future entrants onto the DAX 30. Between 2018 and 2019, the company, which has a presence in more than 40 countries and is partnered with over 250,000 restaurants, saw its revenues growing 119%, to an all-time-high of €1.46 billion ($1.58 billion). Over the past five years, revenues and orders have grown exponentially, fueled in part by a series of lucrative acquisitions that have helped Delivery Hero capture a significant share of the European food delivery market.

Between 2011 and 2019, the Berlin-based company acquired Hungryhouse (UK), Lieferheld (Germany), OnlinePizza (Sweden), Baedaltong (South Korea), and Zomato (India), to name just a few. These acquisitions have added billions of dollars to Delivery Hero’s market cap, putting it on a solid path towards the DAX. Given the triple-digit growth of the food delivery market as a result of the coronavirus outbreak, Delivery Hero could enter the DAX sooner than anyone had previously anticipated.

Scout24 AG

Scout24 AG may not be nearing DAX levels of market cap just yet, sitting firmly on the lower end of the M-DAX, but it certainly has the potential to be a fast riser in the years ahead. The tech company operates a large number of online marketplaces in several industries, with a presence in 18 countries and rising. Although it was founded back in 1998, it is only in the past five or so years that Scout24 has aggressively been expanding its offerings, acquiring numerous large companies along the way.

Scout24’s websites now offer real estate, rentals, cars, insurance, job postings, vacations, and classified ads to tens of millions of users around the world. The company began its acquisition journey with the purchase of the popular daily deal portal Dealstar for an undisclosed sum in 2012. Since then, Scout24 has spent big bucks acquiring the CRM company Flowfact in 2014, before paying over $331 million in cash to acquire Germany’s largest consumer loan marketplace Finanzcheck in 2018. This is clearly a company with big ambitions and a growing share of an increasingly important market.

Carl Zeiss AG

Carl Zeiss AG, which operates under the trade name ZEISS, is one of the world’s largest manufacturers of optoelectronics. With a 174-year history behind it, ZEISS has been making serious steps to expand its global presence and market reach in recent years, to the extent that it could finally break into the DAX in the near future. While the original focus areas of the company on camera lenses, which have seen it manufacturer smartphone lenses for some of the biggest phone manufacturers in the world certainly look promising, its subsidiary Zeiss Meditec AG may hold the key to future DAX membership.

Meditec manufactures, develops, and distributes eye-related medical technology such as medical lasers, surgical microscopes, diagnostic equipment, and visual aids. This is a rapidly growing and lucrative market that ZEISS is clearly trying to capture, recently acquiring industry giants such as the US-based IanTech, whilst winning sweeping FDA approval in 2018 to roll develop and roll out treatment technologies in the United States. This is definitely one company that is worth keeping an eye on in the next few years, particularly if you're looking at investing and trading on DAX 30 index futures.

Which companies have remained on the DAX since its inception – and why?

Source: Bloomberg

While plenty of companies have entered and left the DAX over the years, some have proven themselves to be resilient to the changing market conditions and competition that has dislodged others. A total of 13 companies have been continuously included on the DAX since its launch on 1 July 1988. For various reasons, they have been able to come out on top year after year to retain their position at the peak of the mountain. If you’re wondering how they have managed this, here’s the rundown on the DAX lifers.

Allianz

Industry: Insurance

Year Founded: 1890

Share Price January 3, 2000: 316.50 EUR

Share Price January 3, 2020: 221.50 EUR

Founded in Berlin by Carl von Thieme on 5 February 1890, Allianz was one of the first insurance companies with truly global ambitions. Within just a few years of opening, Allianz had open branch offices in London, Amsterdam, Brussels, Paris, Sweden, and Milan. Today, in terms of revenue, it is the world’s largest insurance company and the largest financial services group. In some years, it has also been the largest financial services company. It provides services in over 70 countries and boasts 147,000 employees, making it one of Germany’s largest employers. Other than its brief and ill-fated foray into the world of banking following its acquisition of Dresdner Bank, Allianz has stuck firmly to its core offerings, having acquired dozens of small and large insurance firms in dozens of countries, before merging them under the Allianz banner. With revenues of over $130 billion in 2019 and more than $1 trillion of assets on its books, Allianz looks set to remain one of Germany’s most important and influential players for the foreseeable future.

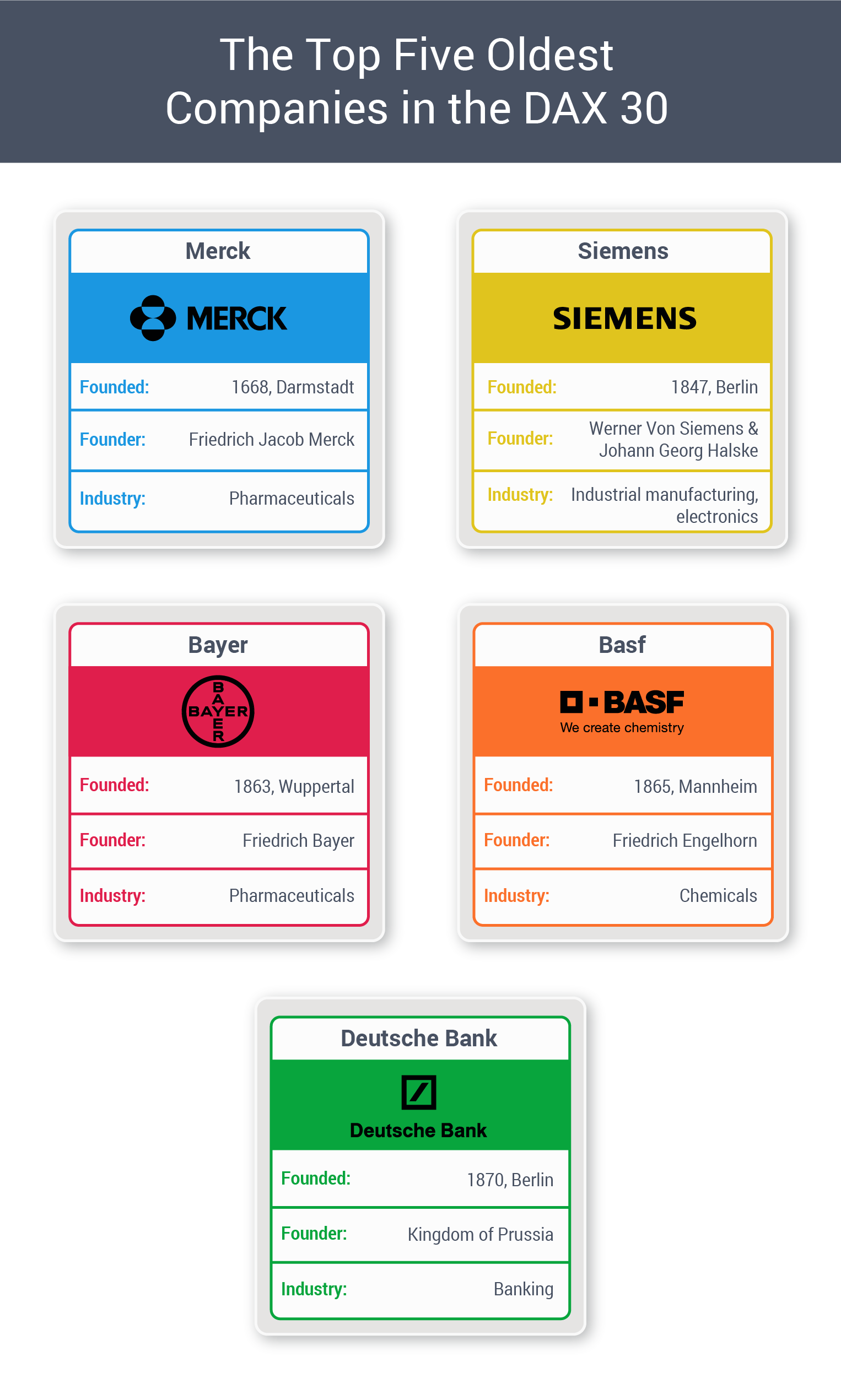

BASF

Industry: Chemicals

Year Founded: 1865

Share Price January 3, 2000: 25.60 EUR

Share Price January 3, 2020: 67.27 EUR

BASF stands for ‘Baden Aniline and Soda Factory and was founded as a gasworks for dye production by Friedrich Engelhorn in Mannheim on 6 April 1865. It is now the second-largest chemical producer on the planet, with operations in more than 80 countries and a global employee roll of more than 117,000 people. The company was one of the first to synthesize vital chemicals like ammonia and sulfuric acid on an industrial scale, and rose to global prominence in the late 20th century by acquiring multi-billion-dollar competitors such as Herbol, Ciba, and Sorex Ltd. The company was briefly one of the world’s most prominent manufacturers of consumer electronics, before abandoning the practice and reverting back to chemicals in the 1990s. BASF boasted revenues of around $65 billion in 2019, with its total assets being valued at around $94 billion.

Bayer

Industry: Pharmaceuticals, Chemicals

Year Founded: 1863

Share Price January 3, 2000: 46.35 EUR

Share Price January 3, 2020: 72.58 EUR

Founded in modern-day Wuppertal by Friedrich Bayer and his partner, Johann Friedrich Weskott in 1863, Bayer was originally focused entirely on the production of commercial dyes. This is a far cry from its current role as one of the largest and most influential pharmaceutical companies on the planet, responsible for a number of world-changing drug inventions. Its first and best-known product was Aspirin, which it still holds a trademark on in over 40 countries, representing billions of dollars in revenue. The company also notoriously trademarked the name ‘heroin’ in 1898, back when it was thought that the deadly drug was an effective cough medicine. Since then, Bayer has ballooned in size, acquiring other major pharmaceutical companies around the world, whilst occasionally tussling with its lifelong competitor, Merck. In recent years, Bayer has notably moved into the high-growth market of genetically modified crops and plant biotechnology, under the banner of its Bayer CropScience Division. Bayer reported revenues of around $47 billion in 2019, with close to $140 billion of assets on its books.

BMW

Industry: Auto Manufacturing

Year Founded: 1916

Share Price January 3, 2000: 29.49 EUR

Share Price January 3, 2020: 73.32 EUR

Bayerische Motoren Werke AG was founded in 1916 via the combination of the business operations of Karl Rapp, Franz Josef Popp, and Camillo Castiglioni. Originally founded as a manufacturer of aircraft engines, BMW switched to producing parts of motorcycle engines, farming equipment, and railway brakes in 1918, before producing its first-ever vehicle, the BMW R 32 motorcycle, in 1923. The company moved into its current niche, luxury automobiles, in the 1950s, but it wasn’t until it began mass-producing more mid-range vehicles in the 1960s that it really took off on a global scale. Other than its acquisition of the Rolls Royce brand in 1998, BMW has largely stayed away from takeovers and acquisitions, instead building its original brand piecemeal throughout the decades. Today, BMW produces millions of vehicles a year, making it one of the largest car manufacturers on the planet. They are one of the most important industry players in the professional motorsport sector, producing cars and parts for Formula 1 and the Isle of Man TT. With revenues of over $113 billion in 2019 and close to $250 billion worth of assets, BMW is the definition of an industry titan.

Daimler

Industry: Auto Manufacturing

Year Founded: 1926

Share Price January 3, 2000: 73.00 EUR

Share Price January 3, 2020: 49.07 EUR

Daimler, more commonly referred to as Mercedes due to its most iconic brand, began its life as Daimler-Benz AG on 28 June 1926, following the merger of Daimler-Motoren-Gesellschaft and Benz & Cie. The company has been producing high-quality, luxury automobiles since then, and is best known for its Mercedes-Benz and Maybach series vehicles. Throughout its history, Daimler has profited immensely from its fiercely-protected reputation as a provider of vehicles of the highest quality, and has generally stayed away from larger takeovers and acquisitions. The stormiest period in its history, however, came from its ill-fated ‘merger of equals’ with the US auto giant Chrysler in 1998, then the largest industrial merger in history, being valued at $38 billion. Daimler sold Chrysler to a private equity firm for a fraction of the price less than a decade later and returned to its primary focus on producing Mercedes vehicles. The company sold 3.3 million vehicles in 2019, making it the thirteenth-largest car manufacturer and the largest truck manufacturer in the world. With 2019 revenues of $188 billion and a total of $333 billion worth of assets, Daimler is in a good position to retain its place at the top for the foreseeable future.

Deutsche Bank

Industry: Banking

Year Founded: 1870

Share Price January 3, 2000: 83.88 EUR

Share Price January 3, 2020: 7.25 EUR

Despite its recent trouble, Deutsche Bank is a giant in the world of finance. Founded on 10 March 1870 in Berlin with the expressed purpose of financing foreign trade and promoting German imports, DB was instrumental in the transformation of Germany into one of the world’s foremost industrial powerhouses. Today it is the largest banking institution in Germany, the 17th largest bank in the world by total assets, and one of the few companies with a joint listing on the Frankfurt Stock Exchange and the New York Stock Exchange. Whilst it has always been an industry leader, Deutsche Bank has struggled with a number of scandals and structural issues over the past few decades, and was especially hard-hit by the 2008 Financial Crash, being forced to pay out billions in fines to financial regulators. Today DB is undergoing a years-long restructuring program to get its finances in better shape, but this doesn’t change the fact that it remains one of the most influential financial institutions on the planet.

E.ON

Industry: Energy

Year Founded: 2000 (Formerly Veba/VIAG)

Share Price January 3, 2000: 14.61 EUR

Share Price January 3, 2020: 9.51 EUR

Originally founded in 2000 as the result of a merger between two German energy institutions, VEBA and VIAG, E.ON is now one of the world’s largest electric utility service providers, providing energy to households and businesses in over 30 countries. While the first couple of years of its existence focused largely on the domestic German market, E.ON began to branch out on the international stage from 2003 onwards, acquiring domestic and foreign energy giants such as Ruhrgas, Sydkraft, OGK-4, and Acciona. It is now one of the leading energy providers in countries such as the UK, Spain, and Sweden, and has transformed its model in recent years by leading the charge towards renewable sources of energy. To this end, E.ON has acquired green energy titans such as Innogy, and built some of the world’s largest wind farms in the UK, US, Poland, and Sweden. With $45 billion of revenue in 2019 and assets totaling around $60 billion, there are few energy companies in the world that can hold a candle to E.ON.

Henkel

Industry: Consumer Goods, Chemicals

Year Founded: 1876

Share Price January 3, 2000: 20.97 EUR

Share Price January 3, 2020: 91.22 EUR

Founded under the name Henkel & Cie in Aachen 144 years ago by Friedrich Karl Henkel, Henkel’s original offering was a best-selling laundry detergent, created thanks to the founder’s penchant for home chemistry. The company spent much of the first 100 years of its existence branching out within the cleaning products market, developing brands such as Persil and Purex which went on to become household names. From the 1970s onwards, Henkel began aggressively expanding into growing industries such as cosmetics and industrial adhesives, going on a shopping spree of acquisitions which included massive companies such as AOK, Advanced Research Laboratories, and Sun Products. While Henkel has not gained the same foothold in the Western market for beauty and home care as its main competitor, Proctor & Gamble, it commands a considerable market share in Asia and the Middle East. Today, more than 80% of Henkel’s 53,700 employees work outside of Germany, with offices and development labs in over a dozen countries. With around $22 billion in revenue in 2018 and more than $30 billion in assets, Henkel has shown the world just how profitable soap and makeup can be.

Linde

Industry: Industrial Gases

Year Founded: 1879

Share Price January 3, 2000: 26.75 USD

Share Price January 3, 2020: 205.36 USD

The Linde Group is the world’s largest industrial gas company, with almost 60,000 employees worldwide and a presence in over 100 countries, thanks to its extensive empire of more than 600 affiliated companies. Linde Group started its life as Linde AG of Germany, founded by Carl von Linde in 1879 with the intention of furthering his development of cooling systems for the brewing and food industries. The company went on to spend much of the next century gobbling up any and all industry players within the industrial gas sector as possible, including AGA AB, Lincare Holdings, and The BOC Group, for which it paid $15.5 billion in cash. Linde AG morphed into the Linde Group when it merged with the US gas company Praxair, cementing its position as the largest industrial gas company in history. Last year the Linde Group brought in $28.2 billion in revenues, whilst also reporting assets worth close to $40 billion.

Lufthansa

Industry: Transport Aviation

Year Founded: 1953

Share Price January 3, 2000: 24.05 EUR

Share Price January 3, 2020: 15.59 EUR

Despite Lufthansa’s recent trials and tribulations, it remains a titan of the airline industry and a strong marker of German national identity. Founded in 1953 as the flag carrier for West Germany, it was originally feared that the company wouldn’t be able to fly any planes, due to the US largely controlling the airspace above the country at the time. However, by the end of the decade, they were running flights across Europe and the Atlantic, whilst subsequent decades involved massive expansions that transformed Lufthansa into one of the largest airlines on the planet. Prior to its current belt-tightening operations that have defined the last decade, Lufthansa acquired a number of well-known major airlines, including Swiss International Airlines (2005), Brussels Airlines (2008), Austrian Airlines (2009), and a large stake in Scandinavian Airlines (2009). Since 2010, Lufthansa has been engaged in major cuts and outsourcing efforts in order to rebalance its finances, but it remains a trusted and high-quality airline, being the first in Europe to receive a Skytrax 5-star certification in 2017. With $40.8 billion in revenues last year and over $48 billion in assets, Lufthansa remains in a better position than most to ride out the current airline industry turmoil.

RWE

Industry: Energy

Year Founded: 1898

Share Price January 3, 2000: 37.49 EUR

Share Price January 3, 2020: 26.84 EUR

Another giant of the global energy industry, RWE provides energy to more than 30 million consumers, mostly in Europe. Founded in Essen in 1898 by a group of industrialists, RWE didn’t get its first power plant up and running until a couple of years later, in 1900. Much of the first 100 years of RWE’s existence saw the company’s operation confined to its corner of Western Germany. However, the company began to develop more global ambitions and expand overseas at the turn of the 21st Century. This process was aided by a number of headline-grabbing acquisitions, including the outright purchases of American Water and Thames Water (both of which it later sold), as well as acquiring energy companies in Poland, Slovenia, the US, and elsewhere in Germany. Much like E.ON, RWE has been making major strides in the renewable energy industry, although its main renewables arm, Innogy, was sold to E.ON in 2018. Today the company employs almost 6,000 people around the globe and pulled in $14.7 billion in gross revenue last year, as well as boosting its total assets to around $93 billion.

Siemens

Industry: Industrial, Electronics

Year Founded: 1847

Share Price January 3, 2000: 90.47 EUR

Share Price January 3, 2020: 116.36 EUR

An icon of the German economy and one of the largest companies on the DAX in terms of market cap, Siemens is the definition of a mammoth conglomerate, with interests in healthcare technology, electronics, power generation, industrial automation, and PLM software, to name just a few. It is the largest industrial manufacturing company in Europe and the 18th largest in the world by total revenue. It is also the oldest company that has been on the DAX since its inception. Founded as Siemens & Halske by Werner von Siemens and Johann Georg Halske in 1847, its first invention was a telegraph device that could spell out messages in letters rather than Morse code, a world-first at the time. Other major original Siemens creations that bolstered its global presence included one of the first hydroelectric power stations, the first loudspeaker device, and the first electric rail. For much of the past century, Siemens has steadily expanded its global operations via the acquisition of industrial titans such as Plessey, Westinghouse Power Generation, Invensys, Dresser-Rand Group, and Brande, spending countless billions in the process. Today Siemens and its many subsidiaries employ around 385,000 people worldwide, making it one of the largest private-sector employers in the world. With revenues last year of $94 billion and assets totaling around $163 billion, Siemens is a hugely influential global player within the world of manufacturing.

Volkswagen

Industry: Auto Manufacturing

Year Founded: 1937

Share Price January 3, 2000: 31.01 EUR

Share Price January 3, 2020: 176.64 EUR

As far as auto companies go, there are very few in the world that can even come close to competing with Volkswagen. Given that the company consistently sells more than 10 million vehicles a year, Volkswagen has held the coveted title of being the world’s largest automaker for several years in a row. It has dominated the market share in Europe for the past twenty years, whilst also holding the title in 2018 of being the world’s largest manufacturing company and the seventh-largest company outright. Founded in 1937 by the ‘Labor Front’ of the Nazi Party to produce a ‘People’s Car’ for the regime, the company’s sole auto offering for the first few decades of its existence was the Type 1, or the Beetle as it is commonly known around the world today. After the war, the company was able to put its dark past behind it, achieving global success due to its ability to mass-produce high-quality, affordable cars for families. A number of its models, such as Golf Mk1, rank among the best-selling cars in history, with tens of millions sold around the world. Volkswagen Group expanded dramatically from the 1990s onwards, acquiring household name auto brands such as SEAT, Audi, Bentley, Lamborghini, Porsche, and Skoda. With revenues of $282.2 billion in 2019 and assets totaling a whopping $530 billion, there are few companies in human history with the financial and industrial clout of Volkswagen.

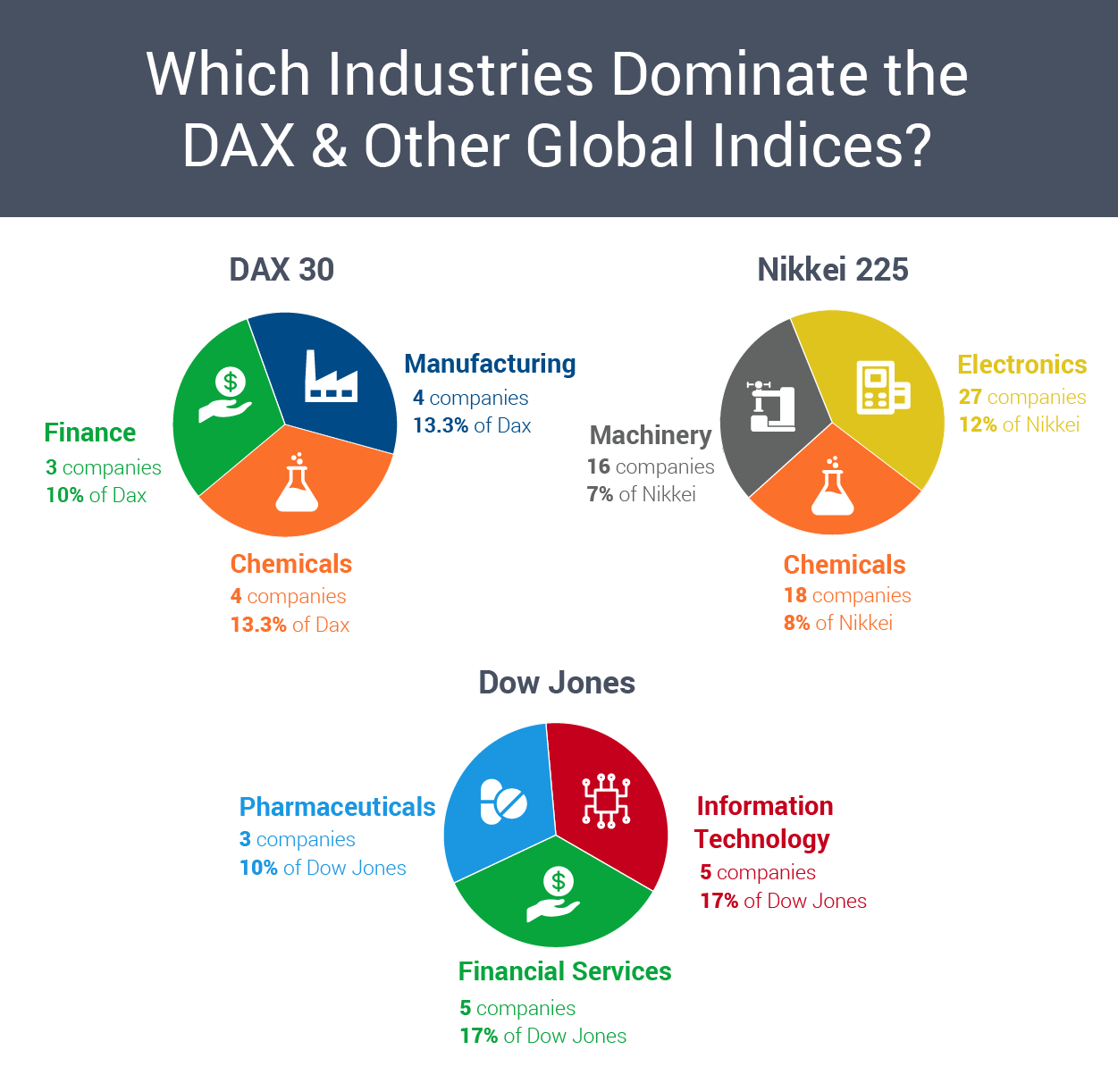

Comparing the DAX to international stock indices

Source: Bloomberg

The DAX may represent the best of the best in the German economy, but how does it stack up against the rest of the world’s major stock indices? Much like the DAX index, other stock indices tend to be dominated by a select few industries. While this is a useful way of getting a picture of a national economy, it’s also worth noting the role that globalization has to play. Across the world, the same few industries, such as oil, energy, auto manufacturing, and banking, tend to dominate.

In the same vein, the biggest companies on the DAX and other indices are never simply domestically focused, but rather are global in their reach. Consider Adidas, for example, which is a hugely significant member of the German DAX that people around the world often mistake to be an American company. That’s not to say that all major stock indices are barely distinguishable, however. All have their own unique features, strengths, and weaknesses, that are vital to understand for anyone looking to trade stocks and shares on the DAX and beyond. Let’s take a closer look at how the DAX shapes up against other major stock indices from around the world.

DAX (Germany)

Market Capitalization (January 2020): $1.36 trillion.

Dominant Industries: Energy, Auto Manufacturing, Chemicals, Finance, Pharmaceuticals

Largest Listed Companies: SAP, Siemens, Bayer, BASF, Allianz

2019 Growth: +25.48%

CAC 40 (France) vs DAX

Market Capitalization: $2.0 trillion

Dominant Industries: Banking, Clothing & Accessories, Aerospace, Auto Manufacturing

Largest Listed Companies: Total S.A., AXA, Carrefour, Credit Agricole, Peugeot

2019 Growth: +26.37%

FTSE 100 (UK) vs DAX

Market Capitalization: $2.55 trillion

Dominant Industries: Banking, Aerospace, Food & Drug Retailers, Insurance, Media

Largest Listed Companies: BP, HSBC, Tesco, Vodafone, GlaxoSmithKline

2019 Growth: +12.10%

Dow Jones Industrial Average (USA) vs DAX

Market Capitalization: $8.33 trillion.

Dominant Industries: Financial Services, Information Technology, Pharmaceuticals, Retail, Defense

Largest Listed Companies: Apple Inc., UnitedHealth Group, The Home Depot, McDonald’s, Visa Inc.

2019 Growth: +22.34%

Nikkei 225 (Japan) vs DAX

Market Capitalization: $4.49 trillion.

Dominant Industries: Machinery, Electronics, Auto Manufacturing, Construction, Chemicals

Largest Listed Companies: Chugai Pharmaceutical, Daiichi Sankyo, Fast Retailing, Daikin Industries, Central Japan Railway

2019 Growth: +18.20%

SSE 50 (China) vs DAX

Market Capitalization: $2.14 trillion

Dominant Industries: Banking, Construction, Real Estate, Insurance, Energy

Largest Listed Companies: Sinopec Group, China State Construction Engineering, Industrial and Commercial Bank of China, Ping An Insurance

2019 Growth: +15.16%

Conclusion

The companies that represent the DAX also represent, in many ways, the parts of the German economy that are most celebrated. Resilience, innovation, flexibility, and quality are all reflected in the household names that make up the DAX 30 Index. Although some members have been at the top of the list since the DAX’s foundation, others are young newcomers that are representing the ripples and disruptions currently underway in German industry. Watch this space to see how DAX develops in 2020 and the years ahead.