Japanese Yen, Collateralized Loan Obligations, CLOs, Leveraged Loans, Coronavirus – TALKING POINTS

- Japanese Yen may rise as CLO market faces tidal wave of credit downgrades

- Coronavirus pandemic threatening to destabilize shaky corporate debt sector

- Market for so-called ‘leveraged loans’ are particularly at risk amid pandemic

Japanese Yen May Rise on Credit Downgrades Risks

The Japanese Yen may extend its gains versus its peers if stress in the market for collateralized loan obligations (CLOs) is amplified in the current environment. The almost $700 billion market is the biggest part of the broader $1.2 trillion market for so-called ‘leveraged loans’. These are debt obligations typically belonging to borrowers on the lower end of credit ratings but whose higher level of risk offers comparatively more generous returns.

The appeal of leveraged loans and the lower tranches of CLOs is the double digit returns they offer, which has been particularly magnified in an environment of falling interest rates. The negative-yielding bond market almost topped $17 trillion in 2019. At the end of that same year, 51 percent of all new investment grade bonds were rated BBB. Put another way, a majority of comparatively safer debt issues wereright on the cusp of being designated “noninvestment grade” or “junk”.

See my breakdown of the leveraged loan market here

The precarious nature of this debt is now being tested by the coronavirus outbreak that is threatening to plunge the world economy and financial markets into the worst turmoil since the Great Depression. “The Great Lockdown” – to quote IMF Chief Economist Gita Gopinath – has put a myriad of businesses at risk of closing their doors, and imperiled firms – particularly non-financial corporations – with high borrowing costs.

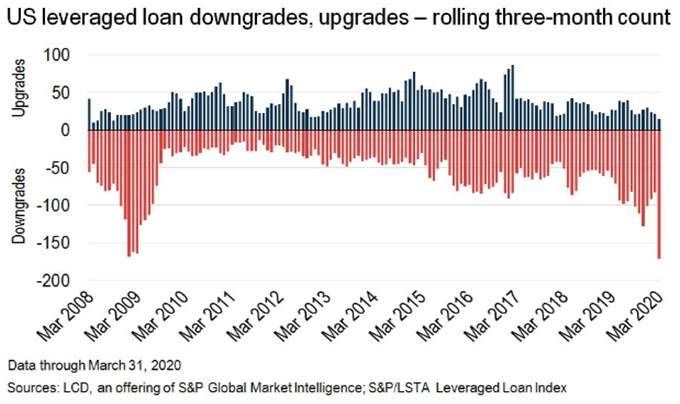

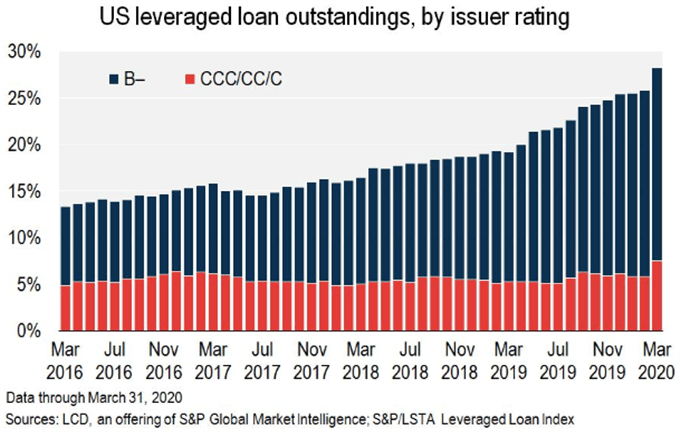

The new economic circumstances have consequently brought forth the much-feared prospect of a wave of credit downgrades, specifically in the corporate debt sector and CLOs into which these obligations have been securitized. The total share of B- rated loans in the leveraged loan market is at a record high following 114 downgrades by S&P Global Ratings in March alone.

Naturally, most of the downgrades were at the tail-end of the credit ratings spectrum. This is because debt issued at those higher-yielding tiers is a reflection of a higher probability of default in the case of a downturn – such as the one we are seeing now. S&P Global Research wrote:

“The share of issuers the S&P/LSTA Index rated B– or lower rose to 28.2% in March, the highest ever, and a 2.4% jump from February. That is the largest monthly increase since November 2008, when this metric jumped 3.5%, to 24%” – S&P Global Research.

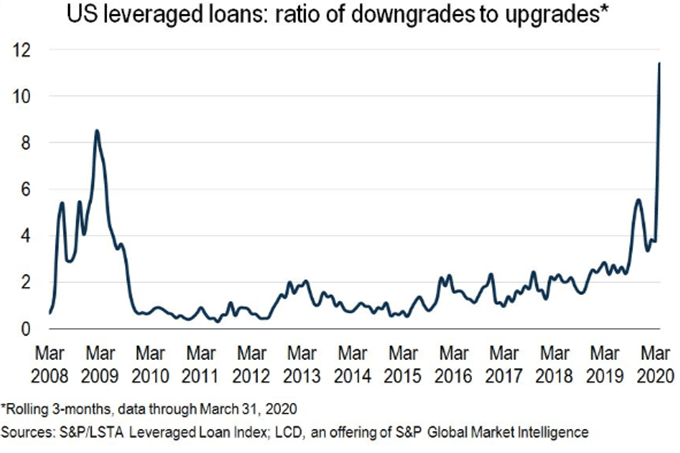

Furthermore, the ratio of credit downgrades to upgrades surged in March to 11.48:1, surpassing the 2009 Great Recession highs of a little over 8:1. However, the key takeaway and major point of concern among investors is the rising share of CCC-rated loans (or lower) underlying CLOs. In the benchmark S&P/LSTA Index, this share rose to 7.48 percent in March – right below the critical 7.50 percent figure.

When the share of CCC-rated debt in a CLO exceeds the 7.5 percent threshold, the manager of the securitized vehicle has to make a choice between two possible ways forward, both of which could rattle markets. He/she might dump lower-rated loans at fire-sale prices or suspend interest payments to investors with exposure to the bonds in the instrument’s lower-level tranches. According to Bank of America, 30 percent of CLOs may already be exceeding that capacity.

The Financial Times wrote that ratings agencies have put more than 1,000 “slices” of debt in CLOs on review, with expectations that the result will lead to a tidal wave of downgrades. The coronavirus pandemic and subsequent shelter-in-place orders that came from governments wanting to contain it, have led regulators to re-evaluate the economic landscape and adjust the ratings of what is now riskier debt accordingly.

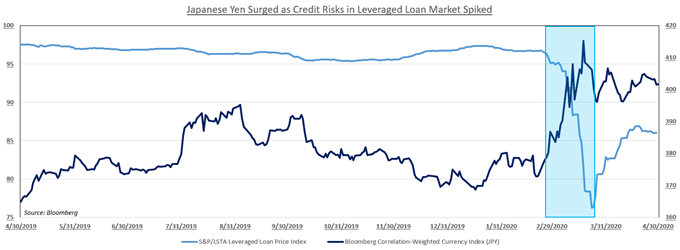

This change in what are already fragile credit markets could spur demand for anti-risk assets like the Japanese Yen. Less than a month ago amid the selloff in global equity markets, JPY surged while the spread on credit default swaps (CDSs) for ensuring sub-investment grade corporate debt skyrocketed. It is not outlandish to suggest this dynamic may yet re-emerge with greater veracity than before as the reality of a deep, global recession is priced into asset prices.

--- Written by Dimitri Zabelin, Currency Analyst for DailyFX.com

To contact Dimitri, use the comments section below or @ZabelinDimitri on Twitter