TALKING POINTS – CLO, FINANCIAL RISK, GLOBAL GROWTH

- What are collateralized loan obligations (CLOs)?

- Do they pose a risk to the global financial system?

- How would FX markets react to CLO meltdown?

See our free guide to learn how to use economic news in your trading strategy !

The IMF, central banks and politicians have warned about the proliferation of collateralized loan obligations (CLOs) and the threat they pose to the global financial system. Currency markets may be battered by breakneck volatility if a slowdown in global economic growth triggers a collapse in this fragile market.

WHAT ARE COLLATERALIZED LOAN OBLIGATIONS (CLOs)?

Collateralized loan obligations (CLOs) are a structured credit instrument, similar to a collateralized debt obligation (CDO), the infamous financial instrument at the center of the Great Recession in 2008. Similar to CDOs, it involves the process of securitizing various debt obligations and then redistributing the cash flows to all participants who bought into the security.

However, CLOs don’t deal with mortgage loans but are rather composed of bundled corporate debt. Within the security are various levels or “tranches” that investors can buy into that cater to the risk appetite each market participant is willing to tolerate. While the top tranches – which generally have higher ratings (e.g. AAA) – get paid out first, the reward is smaller because the level of risk is comparatively lower.

The lower-level tranches get paid out last and generally have lower ratings – e.g. BB – but the payout is higher. A premium offered to investors who are willing to take on additional risk. Some of the more financially-precarious levels offer returns as high as 20 percent, but the associated risk is proportionately higher.

Unlike fixed-income securities, CLOs are packaged with floating-rates yields. Meaning, if prevailing interest rates rise, the yield on the underlying assets will advance accordingly. In this regard, investors have found CLOs to be a great hedge against rising interest rates, a feature not offered in traditional fixed income securities. This might partially explain why popularity in CLOs has grown as global credit conditions tighten.

However, given the recent global slowdown caused by a slower rate of expansion in China, greater political and economic uncertainty in Europe and the pain caused by trade wars, it is possible central banks may pivot toward adopting a more accommodative monetary policy.

WHAT RISKS DO CLOs POSE TO THE FINANCIAL SYSTEM?

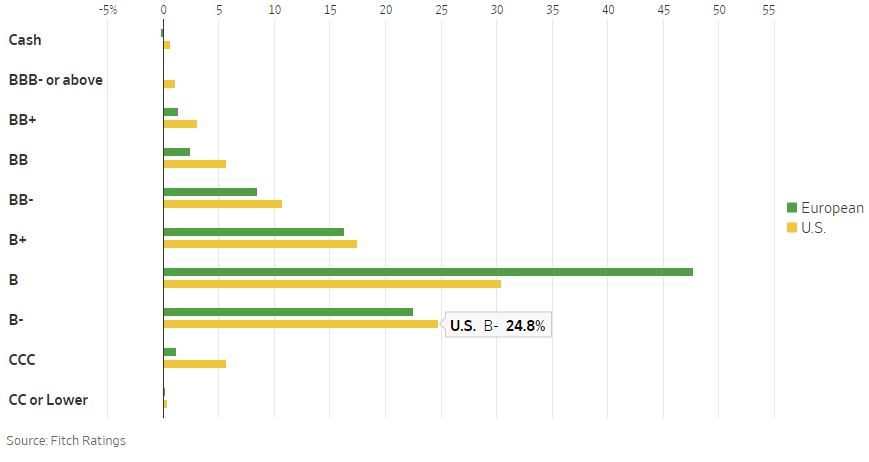

While defaults on CLOs have been relatively low, the growing demand for this instrument has caused a deterioration in underwriting standards. This has led to an increased issuance of what are called “leveraged loans” – high-risk debt obligations. These are often made to firms that have an unfavorable debt-to-assets ratio that puts the lender at a greater risk of suffering a default and reporting a loss on their balance sheet.

These are now being repackaged into CLOs, raising the overall level of risk inherent in owning the security:

Average Distribution of Ratings on CLOs

Source: Wall Street Journal, Fitch Ratings

Central bank officials, politicians and major international institutions are all keeping a close eye on the growing threat that CLOs could pose to the global financial system. As outlined in the IMF’s bi-annual Global Financial Stability Report, the market for leveraged loans currently stands at $1.4 trillion, with global annual issuance reaching a record in 2017 at $788 billion, and “surpassing the pre-crisis high of $762 billion in 2007”.

Coinciding with this has been the rise of so-called “covenant lite” loans, which place fewer restrictions on the borrower while simultaneously offering less protection for the lender. The appeal of CLOs to borrowers is that they are able to obtain a more generous level of financing than normal lending practices would dictate. The appeal to the lender is the prospect of obtaining considerably higher returns to compensate for the risk.

WHAT ARE COVENANTS?

Covenants are in essence contracts that outline specific conditions that the borrower has to fulfill in order to obtain the loan. They are broken down into two categories: “positive” and “negative” covenants. The former is a legal stipulation that requires the borrower to perform certain actions. This can include keeping sufficient levels of insurance and maintaining an adequate credit score.

This could also include keeping certain levels of working capital and retaining essential employees at the business. If the borrower violates any of the outlined conditions, the lender reserves the right to declare a default and require the debtor to repay the principal and interest immediately. Some contracts can contain clauses that allow the borrower to rectify their violation within a given period of time and avoid this outcome.

Negative covenants are implemented as a way to prevent borrowers from actions that could undermine their credit-worthiness and ability to service their debt. Some of these conditions include maintaining balanced business and financial ratios in order to curb the risk of insolvency on the part of the borrower.

This could mean keeping the debt-to-asset ratio under control in order to prevent the borrower from incurring so much debt that it could inhibit their ability to pay the interest and principle Another example is requiring the borrower to keep a specified interest coverage ratio which stipulates that earnings prior to taxes and interest have to be greater by a certain number of times as a way to assure financial health and stability.

Softer covenants also reportedly allow borrowers to magnify their projected future earnings. This could lead to a distortion in the ratings which reflect the level of risk attached to each of the underlying loans within the security. In other words, an investor could be holding a CLO that is actually filled almost – if not entirely – with below-investment grade loans that are more financially precarious than advertised. Sound familiar yet?

HOW CAN A GLOBAL SLOWDOWN TRIGGER A CLO COLLAPSE?

As global demand wanes, consumers begin to spend less, business revenue streams dry up and investors pivot away from chasing yields and more toward preserving capital. Corporations that took out these covenant-lite loans – that were then securitized into a CLO – then face mounting pressure as their ability to service their debt is compromised. The probability of an onslaught of defaults then becomes considerably higher.

Furthermore, companies that are on the hook for these loans may attempt to cut corners or lay off employees as a way to trim losses and stave off insolvency. However, in the process, they may end up breaching their covenant(s), consequently giving the lender the right to declare a default on the loan. This in turn could make many of the income-generating tranches in the CLO worthless and bring down the overall value of the security

The CLOs would then shift their position on the balance sheet from assets to liabilities, potentially putting financial institutions outside the regulatory parameters of capital requirements. This may then force them to start selling other assets to compensate for the losses they incurred on the CLOs. Consequently, a selloff iterated across multiple institutions could trigger broad-based panic and hurried liquidation across global financial markets.

HOW WOULD FX MARKETS RESPOND TO A CLO UNRAVELING?

In the event of a downturn, which is further exacerbated by a CLO collapse, anti-risk assets like the US Dollar, Japanese Yen and US Treasuries would likely gain at the expense of cycle-sensitive currencies like the Australian and New Zealand Dollars. Cycle-sensitive commodities like oil – and currencies that frequently track its movement like the Canadian Dollar, Russian Ruble and Norwegian Krone – may also suffer.

While many central banks could lower rates to combat the downturn, the exact simulative effect of further cuts may not be sufficiently conducive in restoring liquidity and confidence. Other central banks with rates at or below zero like the ECB and Riksbank may have to resort to unconventional monetary measures, though even those are sometimes not effective enough to raise inflation and stave off a slowdown.

CLOs may not be the next trigger for a recession, but they could exacerbate an economic downturn. Furthermore, the average recovery rates for defaulted loans have fallen to 69 percent from the pre-crisis levels of 82 percent. Indirectly-connected players like banks that lend to firms that are holding these instruments or have exposure to them could be at risk.

The exact extent of the CLO web remains unknown. However, what the 2008 financial crisis taught the world is that highly integrated markets are efficient but also incredibly vulnerable. This then risks an element of contagion whereby a system-wide disruption could occur. A web of interconnectedness is often welcome by all – that is, until along comes a spider.

FX TRADING RESOURCES

- Join a free Q&A webinar and have your trading questions answered

- Just getting started? See our beginners’ guide for FX traders

- Having trouble with your strategy? Here’s the #1 mistake that traders make

--- Written by Dimitri Zabelin, Jr Currency Analyst for DailyFX.com

To contact Dimitri, use the comments section below or @ZabelinDimitri on Twitter