“While QE will push asset prices somewhat higher, investors/savers will still want to save, lenders will still be cautious lenders, and cautious borrowers will remain cautious, so we will still have ‘pushing on a string.'”

- Ray Dalio, Founder & CEO Bridgewater

“If You Want To Make Money, Go To The Scary Places”

James Grant, Grant’s Interest Rate Observer

“The signal is the truth. The noise is what distracts us from the truth.”

― Nate Silver, "The Signal and the Noise: Why So Many Predictions Fail - But Some Don't"

To receive Tyler’s analysis directly via email, please SIGN UP HERE

Where We Stand Today In a Post-Brexit World

Friday was a historic day in the markets as the outcome of Thursday's vote confirmed the United Kingdom voted to leave the European Union. However, traders are always forward-looking, and now it is time to ask important questions that could determine where capital flows and global markets. It appears some trends are turning, and others are accelerating, and knowing which or which will be helpful for those involved in the markets.

Midday Monday, the price of Cable had fallen 12.5% from the pre-election outcome high of 1.5017. Traders now though are asking about the ripple effects of the vote and what the change of capital flows and the discount rate could mean to global risk markets. Unfortunately, markets were already on edge due to uncertain central banks, doubtful strength of the United States and Chinese economy, and uncertainty about the sustainability of equity markets near all-time highs.

Access our Post-Brexit Directory here

Until Article 50 is triggered (the Lisbon Treaty Rules for a Member State Leaving the Eurozone), much of the questions around London and the United Kingdom are more political than market-driven. That means much of the global capital flow is in anticipation of what could lie ahead. While sterling weakness is a worthy headline, it is likely just the first chapter in a long book with an unfinished ending.

Here’s a breakdown of the uncertain environment ahead, the key questions to ask regarding what’s can happen to the leading economies and what trading opportunities may arise.

The Current Market Environment: Choppy Waters Ahead

Before the vote, the SPX 500 was within 10 points of the all-time high summer of 2015. In a significant form of divergence, this attempt was with a weakening economic picture and further uncertainty about the efficacy of central banks and their plans to further stimulate the economy. If we see an environment of decelerating economic growth on the back of the Brexit vote, we could soon see a test and break of the February low and likely because by a stronger dollar, lower commodities, and overall worsening risk sentiment that is seen by deeper negative yields.

Now, in addition to the implications faced with the United Kingdom leaving the largest single market in the European Union, we find ourselves in an environment with lower liquidity and higher volatility. Combinations of low liquidity and high volatility often lead to less risk-taking because price variance is often amplified.

Recommended Reading: Adjusting Your Trading Expectations In Volatile & Possibly Illiquid Markets

On Monday, Standard & Poor’s credit rating agency cut the outlook of the United Kingdom to negative and the credit rating from AAA to AA due to the risks of deterioration and external funding and a new Independence referendum in Scotland and Northern Ireland.

Potential & Feared Brexit Ramifications:

Scottish Independence Referendum 2.0

“I also communicated over the weekend with each EU member state to make clear that Scotland has voted to stay in the EU, and I intend to discussion all options for doing so.”

-Nicola Sturgeon, First Minister of Scotland

The United Kingdom to be on the verge of further constitutional difficulties should Northern Ireland, and Scotland decides to leave the UK in favor of rejoining the European Union. While the Standard & Poor’s credit rating cut was widely expected, there are potential ramifications if the negotiations of the exit do not favor Britain’s diverse economy.

A key risk to keep an eye on would be the removal of the British pound as a reserve currency due to instability in the economy. This is not a base case scenario, but if it developed we would likely see forced selling of the sterling.

An additional ramification which is being an increasingly price then, but the extent is still uncertain is easing measures by the Bank of England. The two main questions center around on whether or not there will be rate cuts from the current level of 50 basis points and possible quantitative easing.

On Friday, Reuters reported that the "Bank of England says it cannot should not, stand in the way of necessary adjustments in financial markets after Brexit." Therefore, it is likely that Mark Carney will have the market do much easing on its behalf before acting.

Questions To Guide Us Forward:

Market outcomes often revolve around probabilities and catalysts. Therefore, in addition to numbers, scenarios and questions are often a great tool when faced with uncertainty. The benefit of multiple questions being asked in volatile environments with uncertain outcomes is that you are less likely to be shocked by a specific outcome and often able to act quickly and trade to your benefit as long as risk is managed.

Therefore, here are three key questions as well as three sub- questions worth asking that could provide insight and clarity for trading through the second half of 2016.

Question #1: How Effectively Central Banks Act?

One could easily make the argument that if central-bank policies had been as effective as they were intended, the EU referendum would likely a favored a ‘Remain’ vote. Of course, this is speculation, but it is worth noting that many people were unhappy with the status of the economy as a whole and felt that the benefits of quantitative easing had been heavily tilted towards those who held paper assets, and less towards the working class.

Fortunately, for central banks, if this is an accurate diagnosis of their effectiveness than it is coming at a time when there is little gas in the tank for further accommodation. Therefore, with diminishing belief in the efficacy of extreme and unconventional monetary policies like Zero or Negative Interest Rate Policies & Quantitative Easing, what can banks do now that they have not already done to stem the tide of risk-off that they’ve effectively done at least in terms of most equity markets.

Over the weekend, there were rumors of a new 10 trillion JPY stimulus to be proposed by the Bank of Japan this fall. Additionally, we’ve seen the markets effectively price out any rate hikes from the Federal Reserve as the probability of a February 2017 rate hike has dropped from 48.5% last week down to less than 8% after the Brexit.

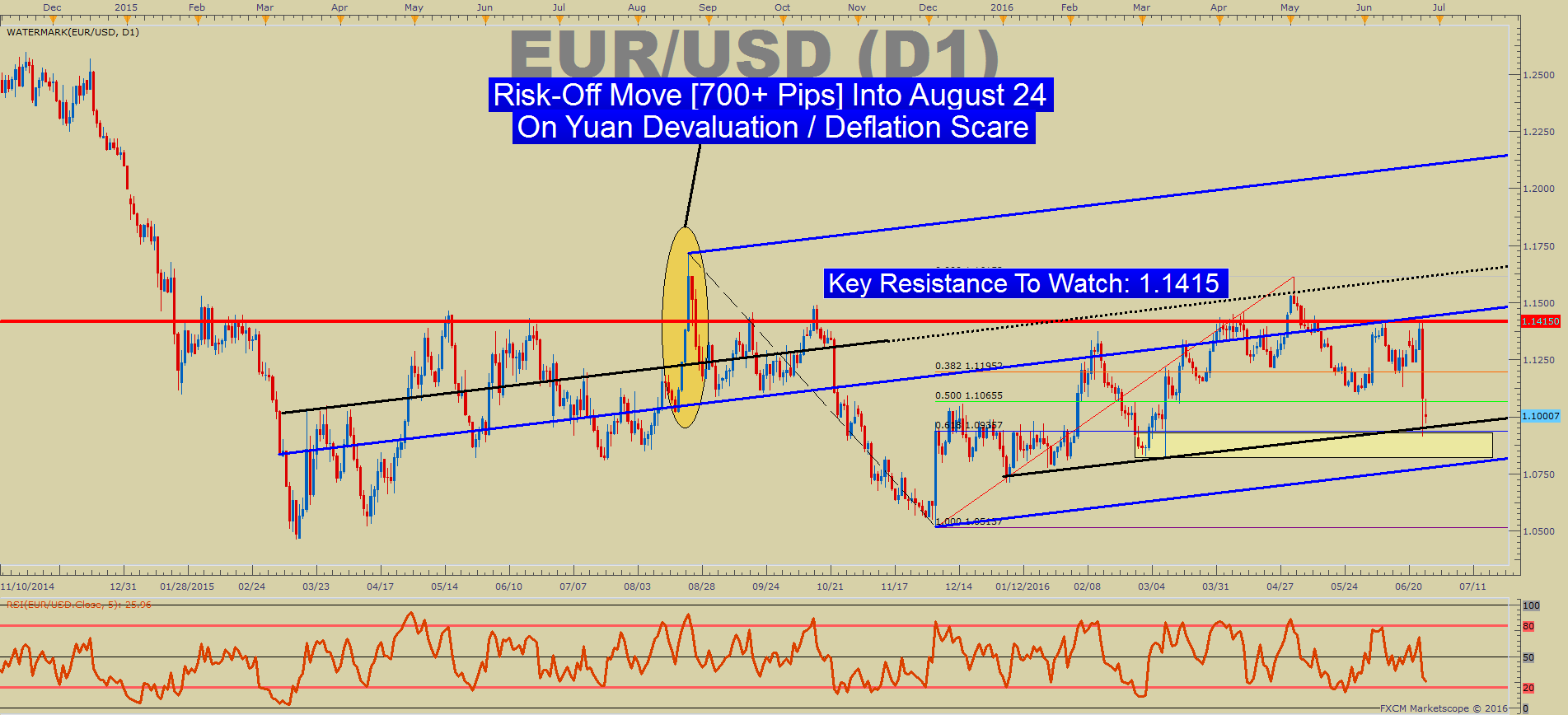

Additionally, we saw on the markets opening that the People’s Bank of China Daily Yuan fixing dropped the most against the US dollar since August and reaction to the Brexit. This was not a risk positive event as will be indicated on the EUR/USD chart below.

In summary, the market is adjusting and anticipating what the next move will be by the central banks. The important answer to the question is if the market cares? If they do not care or find the central banks actions able to stem the risk off tide, how aggressively can market selloff?

Sub-Question #1: Is The Fed’s Game changing?

Many traders have had their head spinning on the back-and-forth preference of the Federal Reserve. They seemingly flip from Dove (favoring an easing of monetary policy relative to market expectations) to Hawk (favoring tightening of monetary policy compared to market expectations) within a few month’s time. To my knowledge, this attempt of guidance has never been so fluid and recent market history.

To back this up, we’ve recently heard from the Federal Reserve Bank of St. Louis President James Bullard that the Fed may be changing the playbook. The quote below is long but worth a read

“The Federal Reserve Bank of St. Louis is changing its characterization of the U.S. macroeconomic and monetary policy outlook. An older narrative that the Bank has been using since the financial crisis ended has now likely outlived its usefulness, and so it is being replaced by a new narrative. The hallmark of the new narrative is to think of medium- and longer-term macroeconomic outcomes in terms of regimes. The concept of a single, long-run steady state to which the economy is converging is abandoned, and is replaced by a set of possible regimes that the economy may visit. Regimes are generally viewed as persistent, and optimal monetary policy is viewed as regime dependent. Switches between regimes are viewed as not forecastable.” [Emphasis Mine]

If what Mr. Bullard said holds, the new question traders will ask is what regime is the Fed recognizing and how is that affecting monetary policy? This would likely have a long-lasting impact on markets.

Given the Federal Reserve’s goals of higher inflation, this regime change would appear to mirror a potential coordinated dollar weakening to hit Fed targets and restore market credibility.

The natural and inevitable question is what happens the market becomes less interested in the Fed’s objectives? Again, the question becomes whether or not the ‘Brexit’ is a catalyst to this new regime coming to the forefront.

Question # 2: What Ripple Effects To Watch?

After the Brexit, the most tangible move in markets outside of Sterling was that of weakness in the European banking sector. This appears to show stress in already weak sectors of the global economy like banking. Italian banks were down 20% on Friday alone.

Other bank indices were also in pain, but the question becomes are the ripple effects of the vote hitting some the most fragile markets before the vote. The answer appears to be, ‘Yes.’

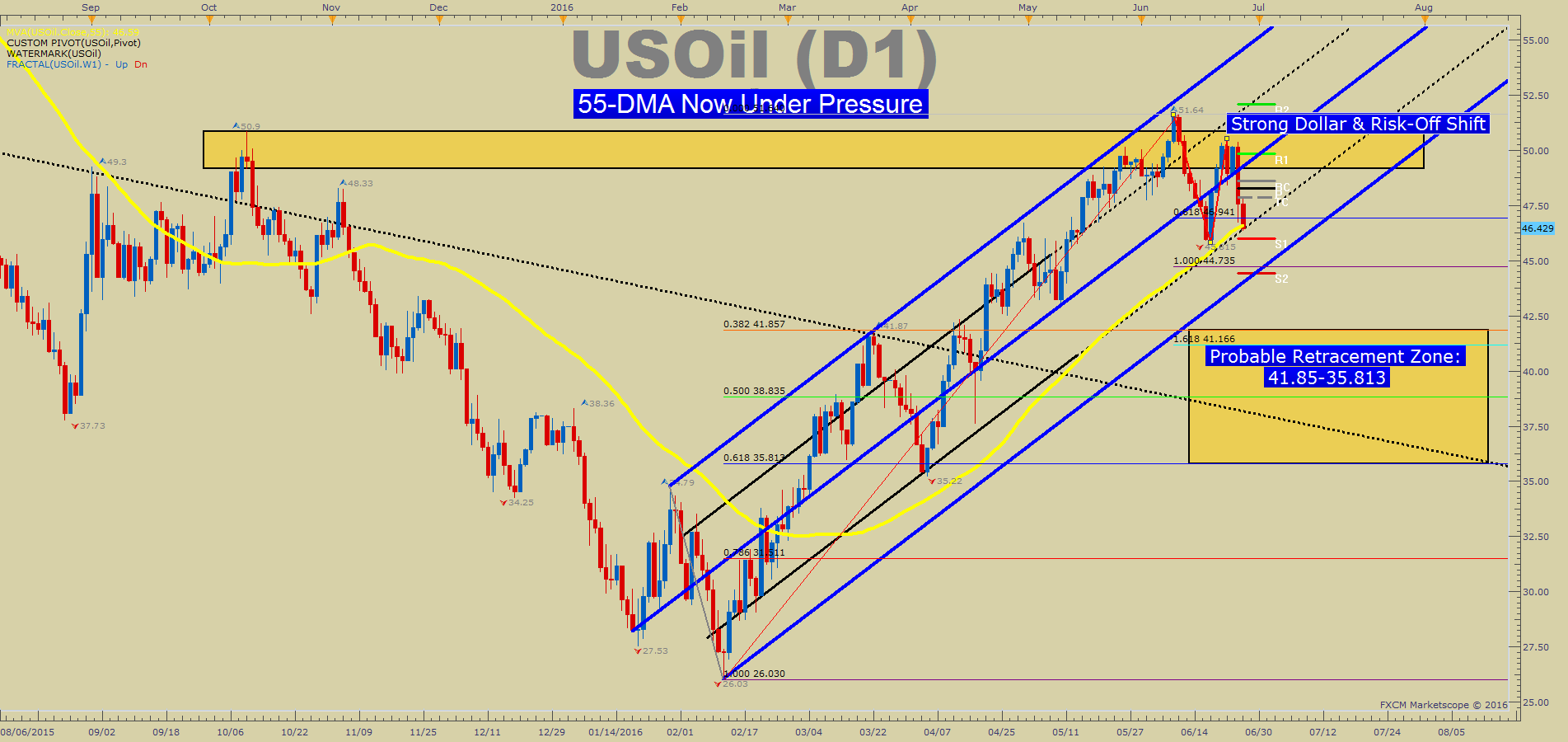

The other market to look for his industrial commodities such as WTI crude oil. WTI Crude Oil has been on an incredible run for most of 2016, but that may soon come to an end if dollar strength begins to take hold. The energy sector was fragile much like the banking sector, and a further weakening here will likely strain many companies to the point where a bailout is needed.

If industrial commodities weaken, it is equally worthwhile to keep an eye on precious commodities like gold to strengthen. Strengthen precious metals alongside weakness and industrial commodities could be complemented by further dollar strength.

From a technical level in crude oil, the easy levels to watch of the 55-Day moving average (currently at $46.59 per barrel) and the May low of $43.00. A break below these two support zones would be indicative of a fragile recovery running at a gas.

Question #3: Is The US Dollar Resuming The Pain Trade?

If the dollar is entering into a new phase of strength, we could be resuming the pain trade. The pain trade is a term coined for dollar strength because a stronger dollar is negative for industrial commodities (not necessarily precious metals like XAU/USD) and therefore has a deflationary effect that is counter to the goals of many central banks (see point number one).

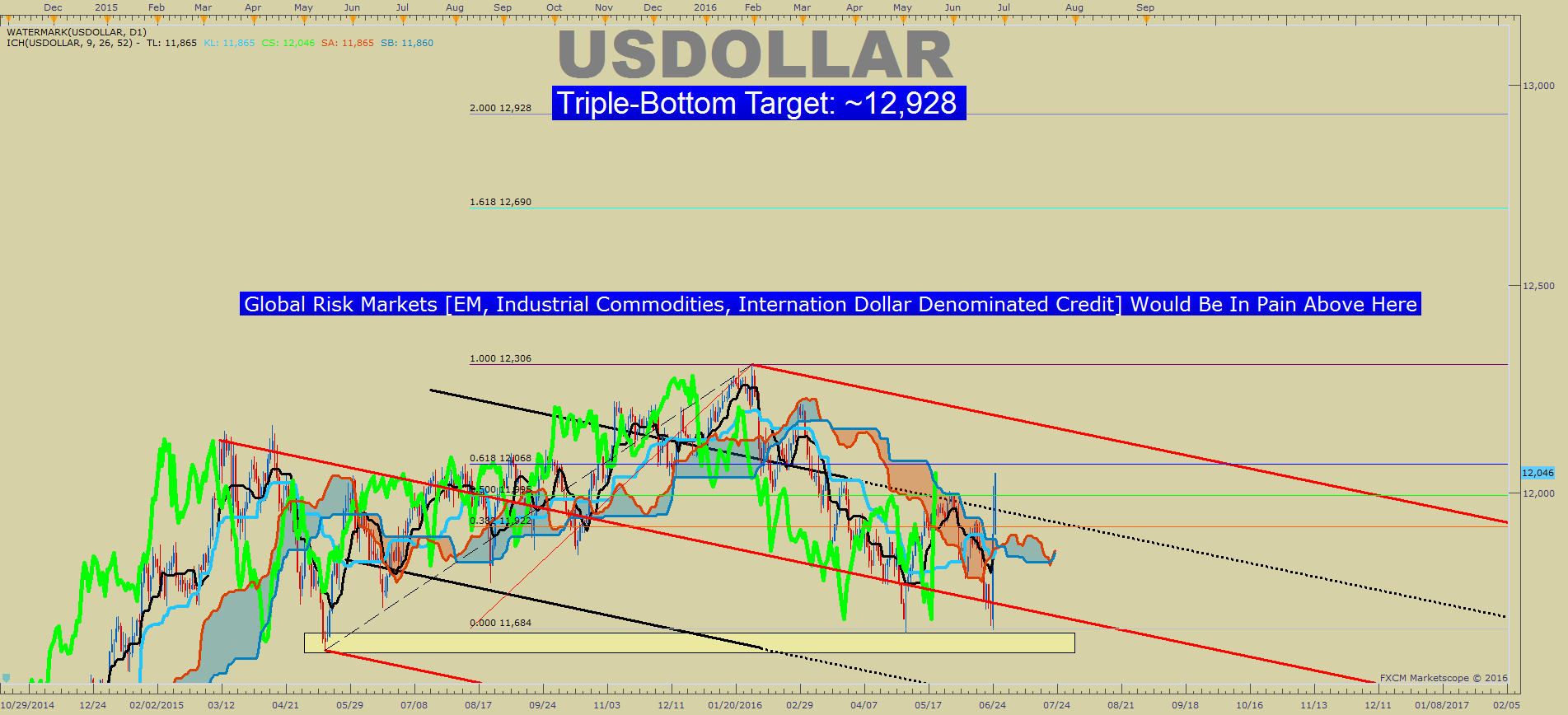

Looking at the chart below, it is possible that we have seen a triple bottom in the US dollar index. From a technical analysis point of view, a triple bottom happens when three attempts of a weakening currency fail at common support and then the market suddenly and aggressively shifts higher to break the range high.

If a triple bottom is in the works, there are a few other trades that work other than those that benefit from a strong US dollar. As noted earlier, the question on many people’s minds (which is likely been conditioned) is what will the central bankers do to limit the dollar strength? However, outside of the fourth installment of quantitative easing, which hasn’t been considered openly yet or a rate cut back to zero (also not openly considered), it is unsure what the Fed could do to limit the pain trade. Investors would assume, though, that they would try.

The chart above shows a zone of support that could be the springboard for A triple bottom. The highlighted zone is the price range of the May 14 extreme day with a low of 11,634. Given the breaks it, and the risk of flow into the US dollar, attention will now be paid on resistance to see if it can hold. The first key resistance was the 12,000 level, which broke aggressively on Monday.

Now, the resistance in focus is the 61.8% retracement of the 2016 range at 12,063 and the top parallel line of the channel that comes in ~12,200. A break above these levels would leave little doubt that the pain trade is among us. The entertainment (as painful as it may be to watch) is to see what’s up the central banker sleeve to prevent such aggressive strength in the US dollar.

The chart above shows targets on a potential triple bottom in the US dollar index. A 61.8% Extension above the 2015-2016 range would take us to ~12,700. A complete triple-bottom move toward the 100% extension would take us toward ~12,930. Once again, the pain of this trade could be similar to the pain in 2008/early 2009 for those who were short US Dollar then.

Fault lines were already being seen in the banking sector stock indices around the world, and a stronger dollar could further stress these banks. Another industry to keep an eye on is energy, which was beginning to gather footing on the 95% plus a rise in WTI Crude Oil from the February low. A return close to the February low would put significant strain on companies with little reserves left recently started to increase production.

Sub-Question #3: If The Dollar does not Strengthen, For What Should We Be Watch?

There are no certainties in markets and often-prided market views come before the falls. Therefore when one side of the trade looks obvious (such as dollar strength), it is worthwhile to see other scenarios that could develop. One such scenario could be current-account positive currency strength such as those from Japan, Europe, Sweden, and Switzerland.

While this is not a default view, it is worth noting that in August when equity markets crashed, and equity futures went limit down (like they did Friday morning after the Brexit outcome was announced), the EUR strengthened aggressively.

Many are expecting EUR/USD to revisit 1.0500 or lower due to the scenario painted above of significant US dollar strength. However, if a risk of scenario does grow in the US dollar does not strengthen, EUR/USD upside is worth watching. Such a development would likely be aligned with a breakthrough the proposed triple bottom support in the US dollar index any further push higher in EUR/GBP toward 1.0000.

Tyler’s Takeaways:

Summer is traditionally a rough time to have a risk-off event like the Brexit due to lower liquidity that leads to higher volatility. Combine that environment with a potential catalyst that the Brexit may bring to resume the pain trade of a stronger US Dollar, and we are likely to have a volatility H2 2016. Such volatility could come despite the Federal Reserve’s intentions to calm markets with their new regime. Additionally, we could see a weakening of fragile markets like the banking sector in Europe, global energy companies, and the value of the Chinese Yuan resurrect deflationary worries. Lastly, we need to keep an eye on a potential Tinderbox for credit, commodities, and central bank credibility that could usher in a strong USD in 2016.