What You Need To Understand:

The stakes are high, yet the explicit implications are hazy. The United Kingdom will vote on whether or not to remain a member of the European Union. The outcome will determine not only whether the United Kingdom stays with the EU, but could also affect credit ratings, reserve currency status, and perhaps the economic future the United Kingdom.

Because markets trade on anticipation of future outcomes, the volatility will likely be greater leading up to the event than days after the outcome is known. You should know the potential market ramifications of staying and leaving for the British economy and currency, the Pound. Moreover, it is important to understand how certain outcomes affect the Euro Zone as a whole.

When Is the Vote?

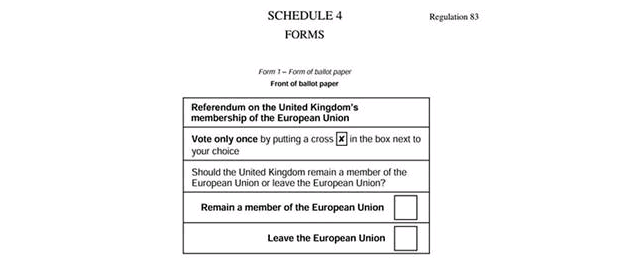

On June 23, the UK electorate will be looking at the following ballot paper in the United Kingdom

Who & What to Watch: Cable, Credit, & Cameron

David Cameron, the Prime Minister of the United Kingdom, is front and center for the ‘Brexit’ vote as well as the negotiations should Britain remain in the EU. The bimodal campaigns of ‘stay’ or ‘leave’ are effectively voting on trade, EU budget, regulation, immigration (which has become a huge sticking point due to the Syrian war displacement), and EU influence over Britain’s economy going forward.

The genesis of the Brexit vote was part of PM David Cameron’s 2015 reelection campaign, where he announced in 2013 as a strategy to strengthen the relationship between Britain and Europe in hopes to make a good relationship better. However, the negotiation might end up being the undoing for now of the conservative party if the rising UK Independence Party (or UKIP) gets their preferred outcome.

David Cameron will look to impress the possible negative economic implications and general shock that could arise from an exit vote. Therefore, as new polling results come in it will be important to watch how Sterling trades, and how credit is priced to reflect the perceived risk of repayment in the market. At the end of February, large banks such as JP Morgan, Goldman Sachs, and HSBC, who have large exposure to credit and ongoing operations in Britain have sided with David Cameron in saying the benefits of staying in the EU outweigh those of the opposite camp.

What is on the Table?

The attention is currently centered on the implications for the United Kingdom. However, you should not dismiss the negative implications to the European Union losing one of its wealthiest members, which could provide a further argument for the exit of other large countries perhaps even core members and/ or Eurozone participants such as Italy.

The United Kingdom’s ability to leave has already stoked a sense of unfairness in the 28 EU nation agreement. French President Francois Hollande & Maltese Prime Minister Joseph Muscat were quick to demand their countries be afforded similar benefits that the United Kingdom seeks to enjoy. The rift is not ill founded. In 2011, an agreement for Britain to take EU initiatives to a referendum passed displaying an unmistakable two-tier system with Britain receiving special considerations that weigh on the fairness of the European Union economic agreement.

Therefore, even if Britain decides to “remain a member” of the EU, the rising threat of another exit will likely have ripple effects for years to come. One thing that Britain will try to avoid should a Brexit be cast is not to disrupt the relationships with the majority of their trading partners still within the EU. Currently, seven of the UK’s nine largest trade partners are EU members, and the risk of damaged trade relationships with even one of those would be great.

What is At Risk?

As Brexit risks increase on the back of polls, investors will likely remain focused on economic implications and credit ratings. Because Britain would be leaving one of the world's strongest trading blocs of its own, there are a few unknowns that will play out. The key focus will understandably be on Britain’s credit rating as it already sports a sizable an account deficit and a Brexit could further stress their economy as noted by the S&P:

”In a worst-case scenario, a Brexit could also harm the sterling’s role as a global reserve currency, removing what has been a significant support for our AAA rating on the UK since the start of the global financial crisis.”

-Standard & Poor’s Statement following the EU deal & Boris Johnson’s Brexit Backing

Should trade relationships that provide an important source of revenue to the United Kingdom deteriorate, attention will turn to the Bank of England. They may be pressured to provide looser monetary policy on a weaker growth outlook that overrides other considerations. Looking at overnight index swaps, investors project a cut by the Bank of England rather than a hike over 2016. In turn, the buoyancy afforded the Pound on an earlier return to normalized rates can further drive the currency down.

On Friday, February 26, 2016, an ominous warning came from Markus Kerber, director general of the Federation of German Industries, who noted that a Brexit would mean a needed revision to thousands of investment contracts involving U.K. and German companies. In not wanting to mince words, Kerber said, a Brexit, “wouldn’t be an amicable divorce…I think the damage for both sides in a Brexit would be very big, but bigger for the U.K. as 50 percent of its trade is with the EU.”

Further, as with past financial crises, the risk tends to begin and end with credit. Aside from Standard & Poor’s statement above, there is appropriate fear that creditors in the United Kingdom and those with balance sheet exposure to British borrowers could share in the risk in the event of a Brexit. While confidence and credit ratings go hand-in-hand, markets tend to overreact in the short-term and watching credit default swaps, a financial market insurance product to hedge against a sovereign or corporate default, should be watched to see if confidence in credit fears are rising along with the price of swap insurance.

Previous Votes that Have Driven the Pound

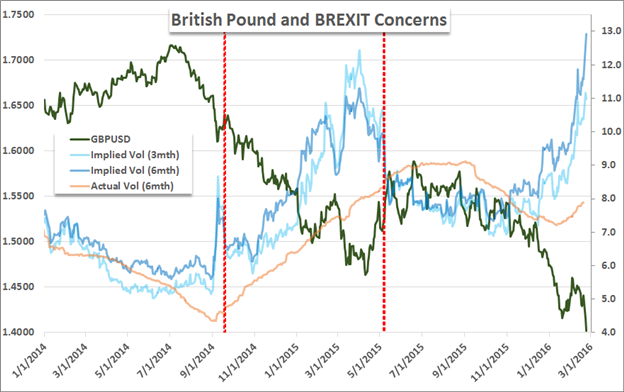

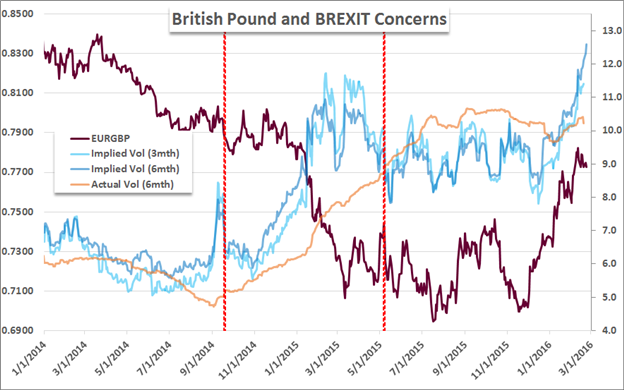

While the UK’s EU referendum is a new risk to face voters, officials, and market participants, it does not come without its precedents. Two previous events that posed apolitically oriented risk that significantly influenced both the Pound and local markets and can be used to extrapolate conditions moving forward are the Scottish Referendum held back on September 18, 2014, and the General UK election held May 5, 2015. Both carried the potential for unnerving outcomes, and the markets exhibited considerable volatility in the lead up to both events.

Below are two graphs that show price action of key Sterling pairs GBPUSD and EURGBP overlaid with the market’s volatility. The red, dashed lines denote the Scottish and General votes. The blue lines reflect expected volatility (also called ‘implied’ and derived from options) for a period three and six months forward. Both events warranted a significant climb in anxiety. With that reference, we can see that the lead into the EU Referendum carries even greater uncertainty for market activity.

Charts above prepared by John Kicklighter, Chief Currency Strategist

Equity Effects: The FTSE 100 & GER 30

As a services-based economy similar to the United States, many of the financial service firms would be the most distressed by a Brexit. In the last week of February, banks began sounding the alarm, suggesting a need for restructuring out of the United Kingdom’s financial district should the exit take place.

JPMorgan CEO Jamie Dimon noted on February 23 that a ‘Brexit’ would bring “massive dislocation,” to London’s financial hub. In Mid-February, Mr. Dimon also noted, “Britain’s been a great home for financial companies and [EU membership] has benefited London quite a bit. We’d like to stay there, but if we cannot, we cannot.” In other words, you can likely expect voters employed by the financial services companies to prefer staying.

Chart Prepared by Tyler Yell, CMT

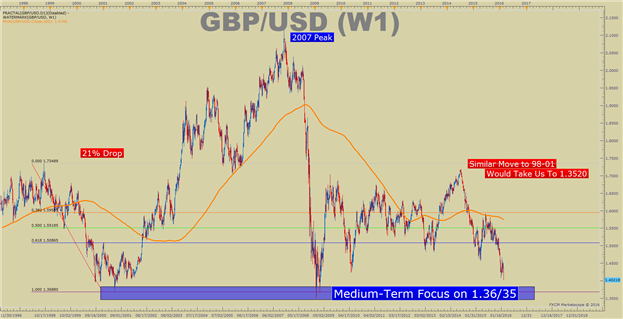

The Key Charts:

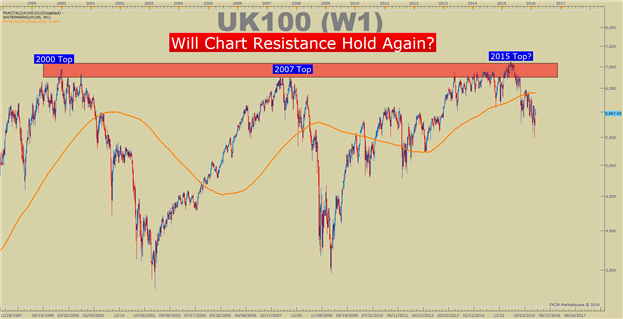

The problem with buying low and selling high is the emotional battle within. At high prices, everything is rosy, and the investor’s mind often tells them to buy more. At low prices, when everything is in dire straits, which was a predecessor to low prices investors often want to sell more. On a simple chart going back to the late 90s, you can see we are pushing off a high price from a move that was initially established in the wake of the 1992 crisis when London left the ERM. While simplistic, this chart may show that optimism to the upside has run its course, and the reason to sell has been switched out from internet boom-bust to housing crisis, to potential Brexit.

However, if the Brexit becomes the economic equivalent of clumsily pulling a rug from under a tier of champagne glasses, we will likely see selling pressure elsewhere. Given the distinct ramifications in the EU, the focus should equally be on the German DAX 30. The long-term weekly chart of the DAX shows late February price putting pressure on the 200-week moving average, which is also shown on the FTSE 100 chart above. A sustained break below that level near 9,150 would likely cause pressure to mount up in regional equity indices. The assumption would be for further selling and lower prices in both the GER 30 & FTSE 100.

Chart Prepared by Tyler Yell, CMT

Political Heavy Weights Are Picking Sides

One of the critical developments that came out over the weekend of February 21 was that Boris Johnson, the popular mayor of London had decided to back the Brexit view - although he did say it was an “agonizingly difficult” decision. Because the polls are nearly evenly split with roughly 45% preferring to stay to the 40% preferring to leave according to one, the effectiveness and momentum of Boris Johnson’s decision could see further important voices shift the standings for the polls. An Ipsos Mori poll showed that almost 1/3 of the electorate that responded noted Johnson’s opinion would be an important factor in their voting decision.

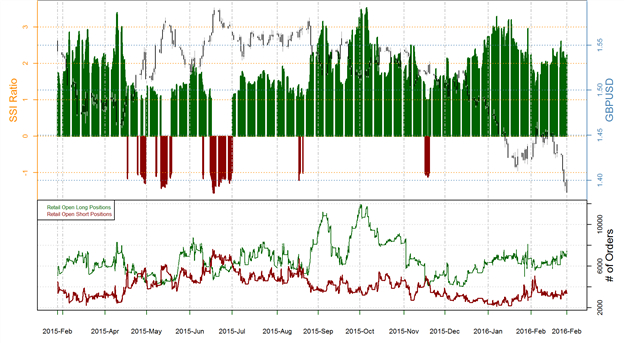

Track Trader Sentiment In Real-time with DailyFX Speculative Sentiment Index

Data source: Speculative Sentiment Index, Chart source: R. Prepared by DailyFX Team

It will be helpful to keep an eye on trader sentiment for GBP/USD as anticipation builds for the Brexit vote. Currently, retail traders as shown by DailyFX Speculative Sentiment Index above have been fighting the GBP sell-off while IMM futures positioning data shows investors continue to build a net short position. However, there is still historical room for further bearish pressure. This positioning data means there is still money on the sidelines that could push this market lower even against the retail positioning who often tries to “buy low” in strong downtrends. Currently, IMM positioning has dropped to levels that were last seen around the SNB-shock of January 2015. A reloading of short Sterling trades could see a retest of the 2001-2009 low of 1.35/36.

Chart Prepared by Tyler Yell, CMT

Probabilistic Outcomes in FX:

The first place to start on a Brexit outcome is the GBP negative view. A Brexit may force Mark Carney and the Bank of England to hold off raising rates even longer. Currently, futures markets are pricing in rate cuts over the next 12 months, which contributed to the two-year gilt yield moving below the current Bank of England reference rate of 50 basis points at nearly 35 basis points.

However, the better opportunities and trades could come from incomplete information on the secondary ripple effects of a Brexit. As noted above, Britain leaving the European Union will turn the doubt towards the existence and sufficiency of the union itself, which German Finance ministers have also been discussing with a plan to impose “haircuts” on holders of Eurozone sovereign debt before further bailouts are issued. Therefore, the subsequent crisis of confidence in the Eurozone kicked off by a Brexit carried by the German Council of Economic Advisers to appropriately price sovereign risk within the Eurozone and force bondholder losses before a bailout could translate into trouble for the Euro.

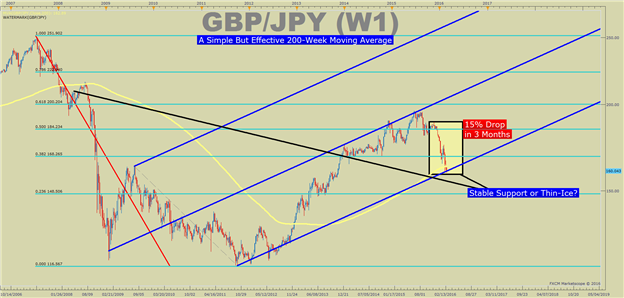

As for currencies that could strengthen, a Brexit could add to a laundry list of global macroeconomic worries that would likely further propel the JPY and CHF higher along with gold. JPY and Gold in 2016 have thus far been the top performing markets. With Euro Zone stability potentially adding to global uncertainties, we could see further leverage for GBP/JPY to break below the 200-week moving average similar to 2008.

Chart Prepared by Tyler Yell, CMT

Another currency that could come out shining from a Brexit would be the US dollar. If the Standard & Poor’s threat of a credit rating cut would, in turn, bolster its reserve currency peers, it could even endanger its long-term reserve status, creating far-reaching troubles.

In contrast, a vote to stay in the European Union will carry far less uncertainty about the future. The existential relief may help to buoy the British Pound, but there will be other concerns to once again evaluate (BoE timing, risk trends, etc.). However, given the Sterling’s significant tumble these past weeks and months versus key counterparts, there may very well be discounts that will be reversed.

The Brexit Takeaway

High conviction bets are scarce now. As we saw during the Scottish independence referendum vote, markets will likely swing violently on new poll outcomes and more intensely when the view shifts to the leave vote. The Sterling rout on February 22 was the most volatility the pound had seen versus the USD since 2011, a slide that took the pair to 2009 levels. However, we could surpass those lows and see the Cable pressure 2008’s generational low – while pressuring its other crosses at the same time.

Understanding what is going on and what is at stake is very important heading into June 23 vote. While much attention will be paid to outright volatility, do not forget how efficient markets are at pricing news as it is released while also remaining remarkably inefficient in its interpretation of the main story. Below, you will find a table of geopolitical events that have caused volatility in the FX market. While these events are not the norm, it is wise to be prepared as event-risk becomes more common in 2016 than in years past.

Trading around highly volatile geopolitical events is in our opinion, not an appropriate time to test the limits of leverage afforded to FX traders. If you look at our Traits of Successful Traders 2.0 Report, you’ll notice that our longest-lasting clients were well-funded and utilized just enough leverage to get more out of their trading ideas, but never too much leverage. When uncertainty is high, as is expected from events such as the British Referendum, liquidity providers understandably shy away from providing deep pricing normally found in markets. Such an environment has led to opening gaps or fast moves that traders with underfunded accounts or overleveraged trades found frustrating. The frustration comes from gaps that can happen on the week's opening bid based on developments over the weekend, when the market is closed for trading. When weekend event risk is prevalent, traders are wise to consider reducing exposure before market close on Friday due to price risk uncertainty.

See How FXCM's Most Successful Traders Handle The Volatility Well in Forex

-Tyler L. Yell, CMT