Highlights:

- Dollar fends off bears after an NFP headline miss, and inline details closing week higher

- Next week contains ECB and BoC, both of which could provide strong FX direction

- Commodity market energy sector remains unclear as Harvey damages still not fully known

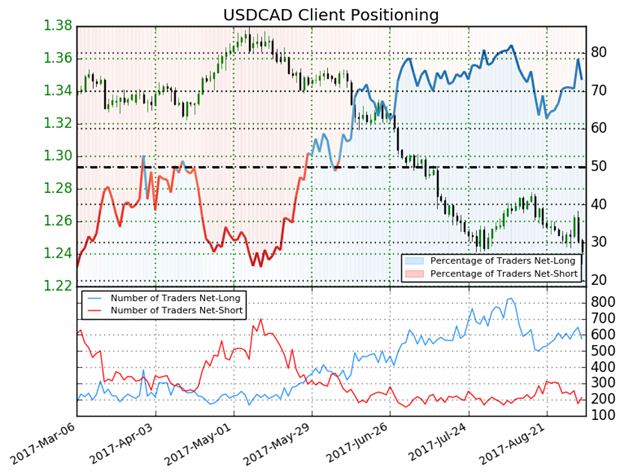

- Sentiment Highlight USD/CAD short positions retreat by 26% WoW, further downside favored

The final four months of the year tend to provide the majority of volatility for trader’s annual calendar. This year could be no different as developing themes both geopolitical and market-based are expected to clarify themselves in the coming weeks and months, which leads to the repricing of previously mispriced assets and brings trading opportunities for those of us that love to pounce on such events.

Friday’s Non-Farm Payroll was seen as a non-event in relative terms as the Fed was not likely to change course (more than they already are perceived to). The headline number had minor misses all around at 156k (vs. 180k) headline as unemployment rose to 4.4%, and Average Hourly Earnings (AHE) missed at 0.1% (vs. 0.2%).A favorable view of the release came from Gary Cohn, a potential replacement for Janet Yellen in 2018 if she is not nominated and Economic advisor to the White House. Cohn said that the numbers were not disappointing and that they were “seeing job creation in the sectors where we want it.”

Be confident with your strategy and your market outlook by consulting our top FREE trading guides.

A bit more significant than Cohn’s words is the push higher in yields of US Treasuries on the front-end. Higher yields align with a lower price that tells investors that the Fed is not seen as being pushed back from tightening monetary policy from today’s news announcement. It is possible the confidence was also borrowed from the US ISM manufacturing has come in stronger than anticipated: 58.8 versus 52.5 expected. There was a sharp move higher in USD/JPY after the news, and EUR/USD pushed toward the daily lows at 1.1860 after the data.

After the US holiday on Monday, the markets will get to work to assess the damage from Hurricane Harvey to see when the largest refiners in the US, which were near the epicenter of the flooding, are expected to be online. We have seen massive calendar spreads between front-month and next month (Sep – Oct) gasoline contracts that show the confusion and shortage at hand. While buying gasoline futures for September on the bet that refineries will not be up and running soon after extensive flooding may feel inhumane, it also helps to get a sense of the stresses upon the infrastructure in coming months.

Keep an eye on our economic calendar for Economic Data Points

The spotlights for central bank action next week will be dispersed around the world. In the US, the focus will be on two Fed speakers, Brainard and Dudley where they will likely be asked to provide a clue toward the kick off the balance sheet reduction plan. Of more interest in North America, especially after a blockbuster GDP is the Bank of Canada on Wednesday. This could have continual ramifications on the USD/CAD downtrend. While favoring a no-hike is still the cautious course of action, the market immediately moved forward the partial pricing of the next tightening from the Bank of Canada from October to September this week.

Not to be outdone, the European Central Bank will also host a rate announcement. The ECB is next week’s main event, but they are not expected to provide new policy signals. Instead, the market is looking to the ECB’s updated economic forecasts and any potential swats at the resurgent EUR. This week, EUR/USD surpassed 1.2000, which could be seen as a liability to the export-heavy economy of Germany, which leads Europe’s current account surplus. Despite what is said, it is difficult to imagine the ECB to completely destabilize the bullish trend seen in EUR/USD, EUR/GBP, and EUR/JPY. The Riksbank (SEK) is also meeting, which could add some volatility to the strong SEK.

Lastly, a central bank with something to cheer about is the RBA. In Australia, the RBA will meet on Tuesday, and they are expected to provide a constructive view on the economic outlook thanks in part to the strong trend in commodities that has continued to defy belief since June. AUD has been favored against weaker currencies like the NZD, GBP, and recently, JPY.

Are you looking for trading ideas? Our Q3 forecasts are fresh and ready to light your path. Click here to access for FREE.

JoinTylerin his Daily Closing Bell webinars at 3 pm ET to discusstradeable market developments.

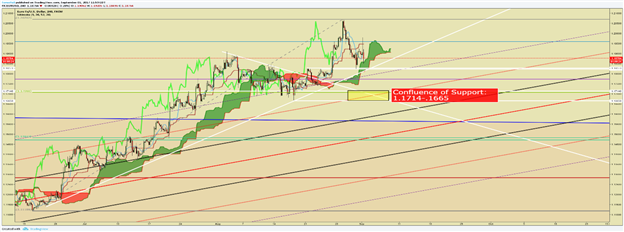

FX Closing Bell Top Chart: EUR/USD tests swing support, breakdown below 1.1830 opens up downside to 1.1665

Chart Created by Tyler Yell, CMT

Next Week's Main Event: EUR European Central Bank Rate Decision (SEP 07)

IG Client Sentiment Highlight: USD/CAD short positions retreat by 26% WoW, further downside favored

The sentiment highlight section is designed to help you see how DailyFX utilizes the insights derived from IG Client Sentiment, and how client positioning can lead to trade ideas. If you have any questions on this indicator, you are welcome to reach out to the author of this article with questions at tyell@dailyfx.com.

USDCAD: Retail trader data shows 72.9% of traders are net-long with the ratio of traders long to short at 2.7 to 1. In fact, traders have remained net-long since Jun 07 when USDCAD traded near 1.34832; the price has moved 7.9% lower since then. The number of traders net-long is 13.0% lower than yesterday and 10.5% lower from last week, while the number of traders net-short is 0.9% higher than yesterday and 26.2% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests USDCAD prices may continue to fall. Positioning is less net-long than yesterday but more net-long from last week. The combination of current sentiment and recent changes gives us a further mixed USDCAD trading bias. (emphasis added).

---

Written by Tyler Yell, CMT, Currency Analyst & Trading Instructor for DailyFX.com

To receive Tyler's analysis directly via email, please SIGN UP HERE

Contact and discuss markets with Tyler on Twitter: @ForexYell