FX Week Ahead Overview:

- The turn into the middle of January brings forth a US-centric docket of economic data and events; all eyes are on the December US inflation report (CPI).

- Chinese inflation data and lending figures for December point to sagging economic momentum in the world’s second largest economy.

- UK GDP may have started to show signs of deceleration in November, ahead of the year-end surge in COVID-19 omicron variant infection rates.

For the full week ahead, please visit the DailyFX Economic Calendar.

01/11 TUESDAY | 12:30 GMT | USD FED CHAIR POWELL NOMINATION HEARING

Fed Chair Jerome Powell will head to Capitol Hill this week for his nomination hearing after US President Joe Biden tapped him for a second term at the end of November. With US inflation rates persisting at their highest levels in nearly 40 years, and the headline US unemployment rate (U3) back below 4%, questions pertaining to the pace of the Fed’s QE taper and eventual rate hikes are likely to be abound – especially in the wake of the December US FOMC minutes that sparked a surge higher in US Treasury yields. While the transcript of his remarks will be released ahead of time, the Q&A portion of Fed Chair Powell’s testimony is likely to generate the most volatility during the nomination hearing.

01/12 WEDNESDAY | 01:30; 08:00 GMT | CNY INFLATION RATE (CPI) (DEC); CNY NEW YUAN LOANS (DEC)

The Chinese economy appears to have slowed down towards the end of 2021, with concerns surrounding the property sector lingering in background. While Chinese company Evergrande may be the posterchild for financial mismanagement, issues are persisting elsewhere. The question for investors remains, “is China heading towards a soft or a hard landing?” The upcoming slate of economic data may not soothe fears, insofar as a further deceleration in Chinese inflation figures and a lack of significant loan origination suggests that the Chinese government is allowing property market sector issues to resolve themselves without heavy handed intervention. Among the major currencies, the Australian and New Zealand Dollars will prove most sensitive to the releases.

01/12 WEDNESDAY | 12:30 GMT | USD INFLATION RATE (CPI) (DEC)

Inflation pressures remain sky-high in the United States, even as Federal Reserve officials have acknowledged that the inflation mandate “has been met” and have guided towards three-plus rate hikes in 2022. With the COVID-19 omicron variant infection rate surging in December and thus far in January, new local lockdowns and restrictions on economic activity may have helped prolonged supply chain issues, which means that headline US inflation rates could still be pitched higher in the near-term.

According to a Bloomberg News survey, the headline December US inflation rate is due in at +0.4% m/m from +0.8% m/m at +7% y/y from +6.8% y/y, with the core inflation rate (ex-energy and food) due in unchanged at +0.5% m/m and at +5.4% y/y from +4.9%. The data will likely help keep US rate expectations firm and US Treasury yields pointed higher, which have been supportive of a stronger US Dollar.

01/14 FRIDAY | 07:00 GMT | GBP GROSS DOMESTIC PRODUCT (NOV)

The UK economy continues to see growth rates trail its G7 counterparts over the past few months, but the upcoming release of the November UK GDP report may prove to be a mixed bag. Consensus forecasts anticipate the 3-month growth rate to fall to +0.8%in the September-November period from +0.9% in the August-October period. This would mark the weakest 3-month period of UK growth since the start of 2021, when the UK was under strict lockdown measures. However, the year-over-year reading is due in at +7.5% from +4.6%, potentially limiting a significant negative reaction by the British Pound.

Nevertheless, with the UK experiencing a sharp rise in COVID-19 omicron variant infections in December and at the start of January, the UK growth data will further stagflation concerns as UK inflation rates continue to press higher.

01/14 FRIDAY | 13:30 GMT | USD RETAIL SALES ADVANCE (DEC)

Consumption is the most important part of the US economy, generating around 70% of the headline GDP figure. The best monthly insight we have into consumption trends in the US might arguably be the Advance Retail Sales report. US economic data around the holidays proved good with the exception of the omicron variant beginning to weigh on momentum, suggesting a sluggish end to the quarter and the year (which otherwise was off to a tremendous start based on data in October and November). According to a Bloomberg News survey, consumption flatlined with the headline Advance Retail Sales due in at 0% from +0.3% (m/m) in November. However, the Retail Sales Control Group, the input used to calculate GDP, is due in at +0.7% m/m from -0.1% m/m.

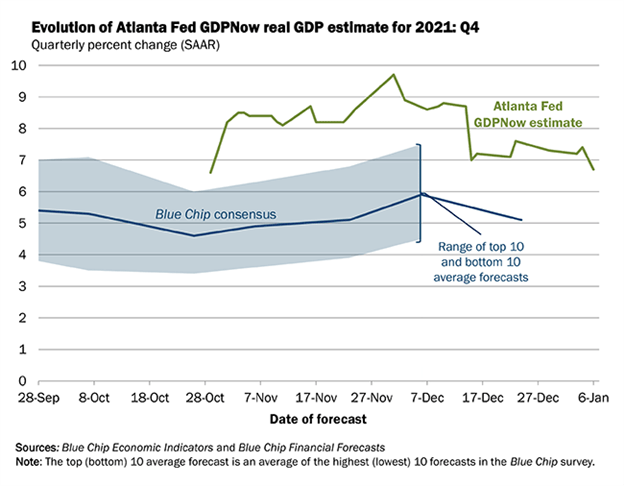

ATLANTA FED GDPNOW: 4Q’21 GROWTH ESTIMATE (JANUARY 6, 2022) (Chart 1)

Based on the data received thus far about 4Q’21, the Atlanta Fed GDPNow growth forecast is now at +6.7% annualized, down from +7.4% on January 4. “Recent releases from the US Bureau of Economic Analysis, the US Census Bureau, and the Institute for Supply Management” have weighed down US growth expectations as the COVID-19 omicron variant infection rate has surged in recent weeks.

--- Written by Christopher Vecchio, CFA, Senior Strategist