FX Week Ahead Overview:

- Central banks are in focus, with the Reserve Bank of Australia (Tuesday), the Federal Reserve (Wednesday), and the Bank of England (Thursday) on tap in the middle of the week.

- Labor market reports define a busy first week of November, with data due from New Zealand, Canada, and the United States over the coming days.

- On the lower end of the spectrum, global PMI readings – particularly from Asia and Europe – could introduce additional volatility to FX markets.

For the full week ahead, please visit the DailyFX Economic Calendar.

11/02 TUESDAY | 03:30 GMT | AUDReserve Bank of Australia Rate Decision

The Reserve Bank of Australia looks ready to abandon its yield curve control (YCC) policy, having allowed the front-end of the Australian government bond curve to blow out over the past week. The RBA will likely signal that it will end its QE program by mid-1Q'22, and the first rate hike will arrive sometime in mid-2022, putting it well-behind the pace of its RBNZ counterpart (which should hike again this year). Regardless, the Australian Dollar – with a persistent net-short position in the futures market – is well-positioned to continue its rally.

11/03 WEDNESDAY | 18:00 GMT | USD Federal Reserve Rate Decision & Press Conference

The 3Q’21 US GDP report may have proved disappointing in some respects, but not enough to have dissuaded policymakers that it’s now time to taper. Throughout October, several Fed policymakers suggested that they believe “substantial progress” has been achieved, and in context of persistently higher inflation pressures, that tapering should begin as soon as possible.

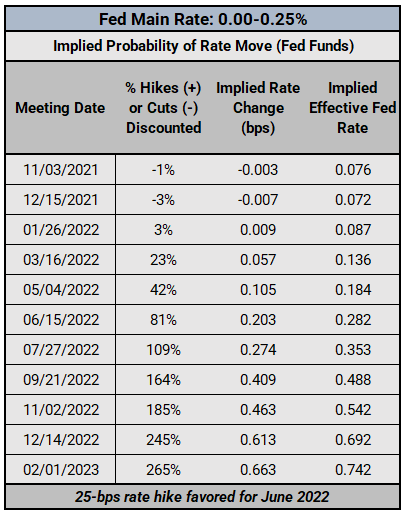

As has been the case for several weeks now, continually elevated Eurodollar spreads alongside action in the US yield are consistent with the 2013/2014 period that suggests a more hawkish Fed is soon to arrive. There are 137.25-bps of rate hikes (that’s five 25-bps rate hikes plus a 49% chance of a sixth hike) discounted through the end of 2023 while the 2s5s10s butterfly recently reached its widest spread since the Fed taper talk began in June (and its widest spread of all of 2021).

FEDERAL RESERVE INTEREST RATE EXPECTATIONS: FED FUNDS FUTURES (NOVEMBER 1, 2021) (TABLE 1)

Now, at the start of November, Fed funds futures are discounting an 81% chance of a 25-bps rate hike in June 2022. This is far and away the most hawkish that rates markets have been since the start of the pandemic.

11/04 THURSDAY | 12:00 GMT | GBP Bank of England Rate Decision

The Bank of England has a tall task to meet this week considering how aggressive rates markets have evolved in October. With rate hike expectations having priced in nearly four hikes through the end of 2022, it's likely that the British Pound walks away disappointed this Thursday; the hawkish case is priced to perfection.

11/05 FRIDAY | 12:30 GMT | CAD Employment Change & Unemployment Rate (OCT)

The Bank of Canada surprised markets last week by cutting its QE program entirely and suggesting that rate hikes could be coming soon. As such, there is a reasonable basis of expectation that they believe the Canadian economy is performing well, building on the robust September jobs report with another strong labor market performance in October (thanks in part to the strong energy picture). The consensus forecast points to the Canadian economy having added another +50K jobs last month, dropping the unemployment rate to 6.8% - which would be the lowest level since the pandemic started.

11/05 FRIDAY | 12:30 GMT | USD Nonfarm Payrolls & Unemployment Rate (OCT)

The primary consideration for the US Dollar when it comes to the October US nonfarm payrolls report is whether or not the US labor market regained its momentum after weaker reports in August and September. The August print came at +235K while the September reading registered +194K. According to a Bloomberg News survey, forecasters are looking for jobs growth of +450K, while the unemployment rate (U3) is anticipated to drop from 4.8% to 4.7%.

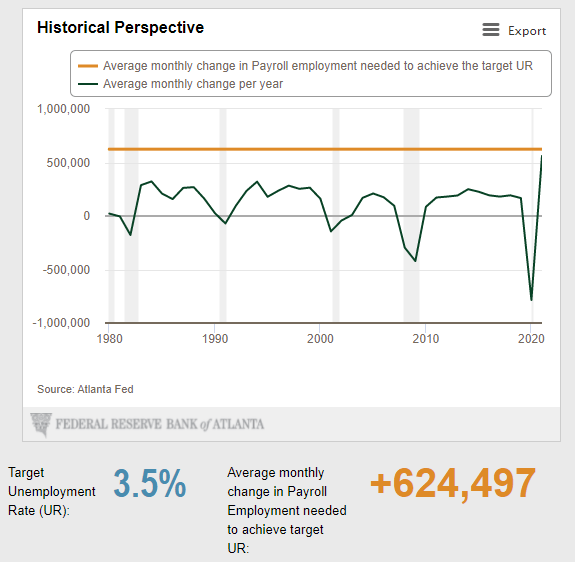

Atlanta Fed Jobs Calculator (November 1, 2021) (Chart 1)

Even if there are good US jobs data, there is still a long ways to go before the US reaches ‘full employment’ as experienced pre-pandemic. According to the Atlanta Fed Jobs Growth Calculator, the US economy needs +625K jobs growth per month over the next 12-months in order to return to the pre-pandemic US labor market of a 3.5% unemployment rate (U3) with a 63.4% labor force participation rate.

--- Written by Christopher Vecchio, CFA, Senior Strategist