SEPTEMBER INFLATION KEY POINTS:

- September U.S. inflation rises 0.4% on a monthly basis, bringing the annual rate to 8.2% from 8.3% in August, topping expectations

- Core CPI climbs 0.6% month-over-month and 6.6% compared to one year ago, exceeding forecasts

- Stubbornly high price pressures in the economy should keep the Fed on hawkish path, supporting the U.S. dollar while creating a challenging environment for stocks

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Most Read: What is Earnings Season & What to Look for in Earnings Reports?

Updated at 9:15 am ET

MARKET REACTION

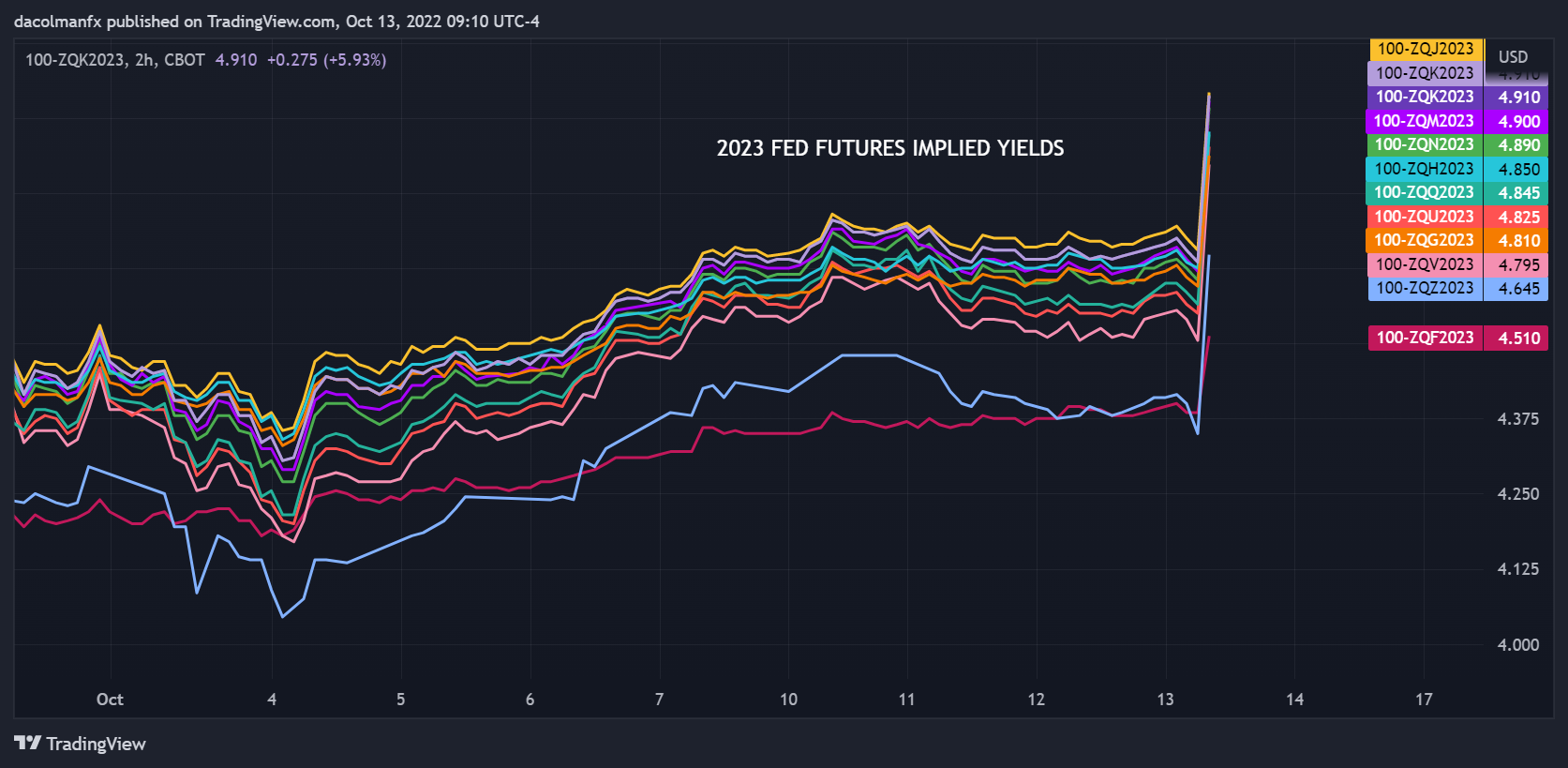

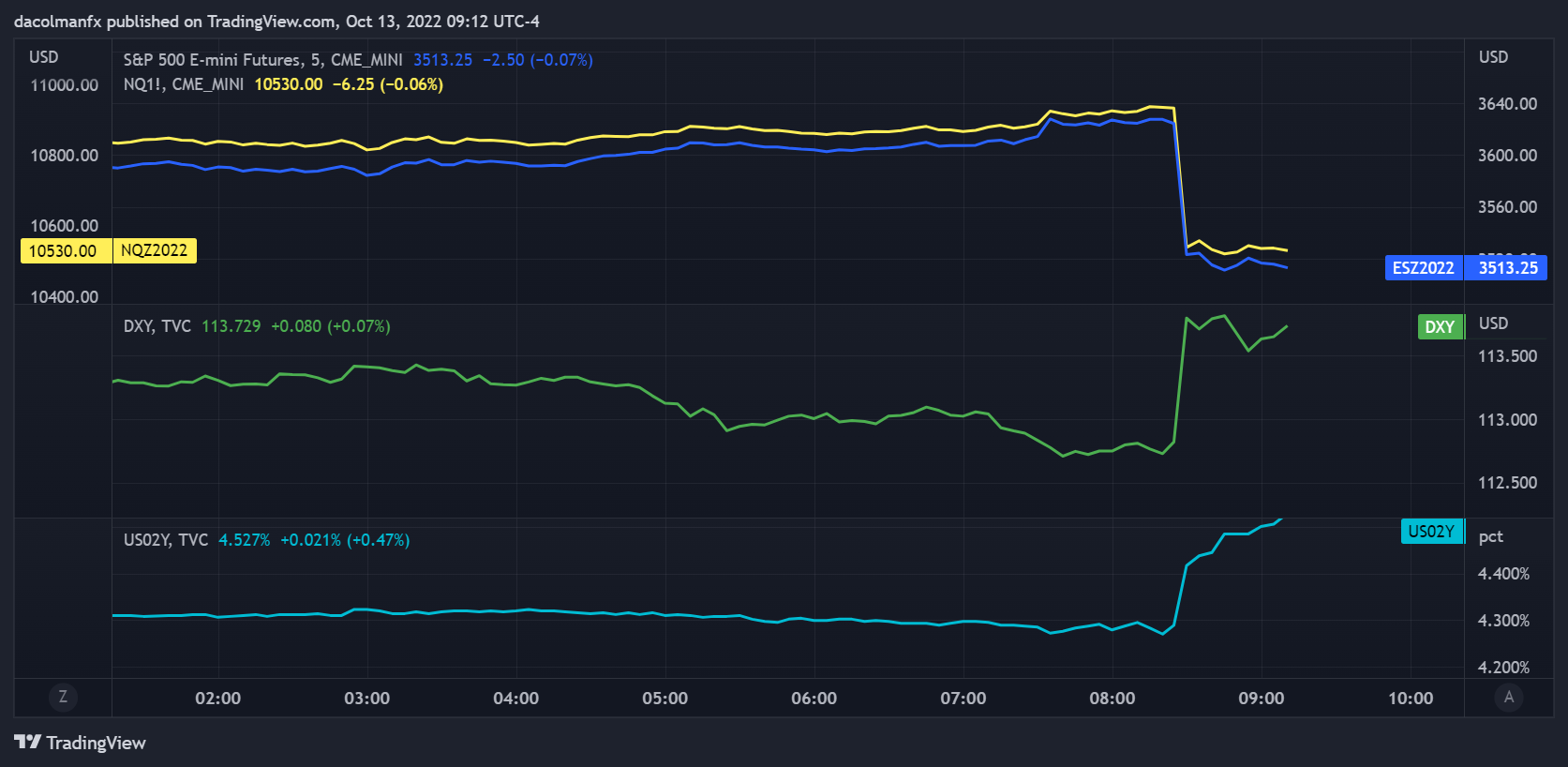

Immediately following the release of the CPI report, U.S. Treasury yields shot higher as traders began to discount a more forceful hiking cycle by the Federal Reserve, as seen in the Fed futures chart below (2023 contracts). The move in rates sparked a solid rally in the U.S. dollar, but weighed on stocks, sending the S&P 500 down nearly 2% at the time of this writing. Looking ahead, the likelihood that the central bank will have to raise borrowing costs more aggressively to curb skyrocketing price pressures should underpin the greenback and reinforce the bearish bias in the stock market.

FED FUTURES CHART (IMPLIED RATES FOR 2023 CONTRACTS)

S&P 500, NASDAQ 100, US DOLLAR (DXY) AND 2-YEAR YIELD CHART

Source: TradingView

Original post at 8:40 am ET

The latest U.S. inflation report, released this morning, brought volatility to markets as the data confirmed that price pressures are not moderating fast enough and at an acceptable pace despite rapidly tightening financial conditions, a sign that the Federal Reserve cannot afford to veer off its hawkish hiking path any time soon.

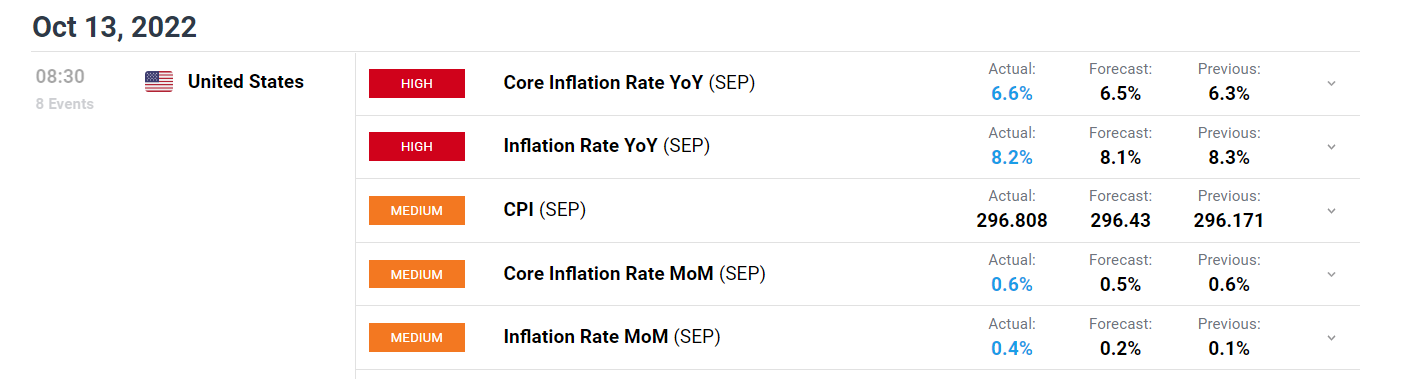

According to the U.S. Bureau of Labor Statistics, the consumer price index inched up 0.4% in September on a seasonally adjusted basis, bringing the 12-month reading to 8.2% from 8.3% in August, a welcome but slow directional improvement that leaves the annual rate still more than four times above the FOMC's 2% long-term target. Consensus expectations called for a 0.2% month-over-month and 8.1% year-over-year increase in the headline indicator.

Excluding food and energy, so called core CPI, which strips out volatile components from the calculation and is thought to reflect longer-term trends in the economy, jumped 0.6% in monthly terms versus 0.4% expected. Compared to one year ago, the index accelerated to 6.6% from 6.3% previously, topping the cycle’s high set in March and reaching the highest reading since 1982.

INFLATION DATA AT A GLANCE

Source: DailyFX Economic Calendar

In terms of the monthly drivers, food and shelter remained on an upward trajectory, climbing 0.4% and 0.7%, respectively, giving little respite to low-income families who spend most of their wages on these two expenditure categories. However, overall price growth was contained by declines in energy, used vehicles, apparel and medical care commodities. These four items declined by 2.1%, 1.1%, 0.3% and 0.1% correspondingly.

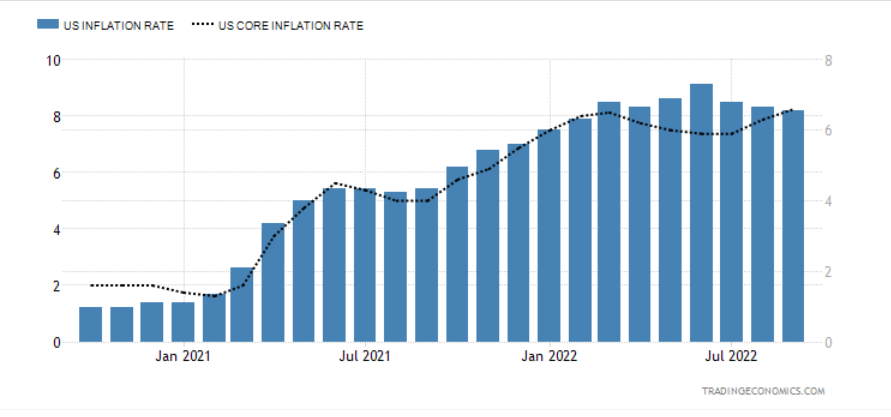

INFLATION CHART

Source: Trading Economics

MONETARY POLICY OUTLOOK

All things considered, there is not much to celebrate in today's CPI report. While the headline index eased at the end of the third quarter in annual terms, the core indicator retained strong momentum, especially the sticky rental component, suggesting that the broader trend remains biased to the upside for now.

In the current environment, the Fed may have no choice but to continue raising rates aggressively to bring monetary policy to a sufficiently restrictive level and keep it there for some time in an effort to curb inflation via demand destruction. This means that a "dovish pivot" is unlikely to materialize in the near term, even if tightening financial conditions lead to a painful recession.

US DOLLAR AND STOCK MARKET IMPACT

Stubbornly high inflation is a recipe for borrowing costs to rise further and for the monetary policy stance to remain restrictive for an extended period of time. Against this backdrop, U.S. Treasury yields should stay supported, especially those in the front end, reinforcing the U.S. dollar's bullish impetus seen in 2022. On the other hand, stocks are likely to continue to suffer in the face of mounting economic and earnings risks, creating a hostile setting for the S&P 500.

EDUCATION TOOLS FOR TRADERS

- Are you just getting started? Download the beginners’ guide for FX traders

- Would you like to know more about your trading personality? Take the DailyFX quiz and find out

- IG's client positioning data provides valuable information on market sentiment. Get your free guide on how to use this powerful trading indicator here.

---Written by Diego Colman, Market Strategist for DailyFX