USD, JPY, Euro Talking Points:

- This article takes a step back to look at three top FX themes for 2023.

- Does the Fed pivot and what might that pivot look like? The bigger change may be at the BoJ but focus will remain on the ECB and BoE as each struggles with +10% inflation.

- The analysis contained in article relies on price action and chart formations. To learn more about price action or chart patterns, check out our DailyFX Education section.

It’s been a big year for FX markets. The US Dollar came into the year with a full head of steam and in February, a major event triggered a historic run in the Greenback that lasted all the way into September. Along the way, the British Pound went into collapse after the unveil of a peculiar budget, which marked one of the shortest leadership ventures atop British politics as Liz Truss’s tenure could not outlive a head of lettuce. In Europe, the Euro put in a threatening fall below the parity level as worries built over a storm on the horizon. Inflation remains aggressively-high in the Euro bloc but the ECB has recently started hiking rates in effort of stemming that inflation. In turn, that’s helped EUR/USD to recover a bit but going into 2023 that remains a very unsettled theme.

Below, I look at three of the Top Themes for the FX market in 2023.

The Fed Pivot

Interestingly this has been a notable theme pretty much since the Fed started to hike. The Fed hiked rates for the first time in this cycle in March and by June, there was already building hope that inflation had topped and the Fed could begin to ease up on their rate hike plans.

That didn’t pan out over the summer as inflation continued to run-higher. And the Fed never really calmed, as they started to hike by 75 bps at the June rate decision and continued to do so at each meeting until December, when they backed down to a 50 bp hike. To some, this signaled a pivot already, in that the Fed only hiked by 50 v/s 75, but that ignores history as 75 bp hikes have historically been an outlier move reserved for extreme circumstances, such as we’ve seen since all of the Covid stimulus came online.

The unassailable fact remains that inflation is too high. And if the US economy does go into a recession with CPI over 5%, the Fed is in a difficult spot as they have little latitude in stimulating the economy. This would be the scenario that the Federal Reserve would look to avoid at all costs which also helps to explain why they’ve been hiking so aggressively even with warning signs showing in housing.

So, we should probably define what constitutes a ‘pivot’ in this case since the Fed is still in an extremely-hawkish place. Getting less hawkish seems likely because well, we’ve already seen the start of that with a move down to a 50 bp cut from the prior 75. And taking that a step further, we’ll probably see the Fed shift down again at some point in the next couple of rate decisions to 25 bp hikes

If inflation makes a convincing turn lower, there could be motive for the Fed to pause rate hikes and this would be another form of a pivot. As a matter of fact, this might be the most likely too considering that we’ve heard multiple Fed members state that they wanted to hike rates to a restrictive level and then pause.

But – what about a full-fledged pivot into rate cuts? There was some bubbling anticipation of possible rate cuts for 2023 during 2022 but, given where inflation remains that seems a more distant prospect. It seems for the Fed to begin cutting rates by the end of next year, inflation would need to fall in historic fashion and if inflation was back-below the 2% target, the Fed could investigate policy loosening. But for that to happen, it would seem that we would need to see some pretty major developments elsewhere. If there’s a housing collapse or some other black swan-like event, the dominos could fall such that the door could re-open for the Fed to start cutting rates but it would seem that some pretty significant destruction would need to take place first to allow for that scenario.

But, it’s important to note that these matters can shift quickly. Coming into 2022 the Fed had forecasted a mere 2-3 rate hikes which is pretty far from what ended up happening.

US Dollar Monthly Price Chart

Chart prepared by James Stanley; USD, DXY on Tradingview

The Bank of Japan

The year of 2022 was marked by most developed Central Banks moving into some form of policy tightening in effort of stemming inflation. Hearing the ECB, BoE and Federal Reserve embarking on 50 bp rate hikes just a year ago would seem unthinkable. There is one notable exception, however, as the Bank of Japan remains as loose and passive as they were throughout the backdrop of the pandemic.

Initially in 2022, this led to a massive run of Yen-weakness as the currency was favored for carry trades, and as rates in the US, Europe or the UK were lifting, that low-yielding Yen made for an ideal backdrop for carry.

But towards the end of 2022, something started to shift in Japan, and inflation started to run-higher. Granted, this is far delayed from the inflation spikes elsewhere, but with inflation at 40-year highs and the Bank of Japan still such an outlier in the global rates picture, the question remains for how much longer can they maintain policy?

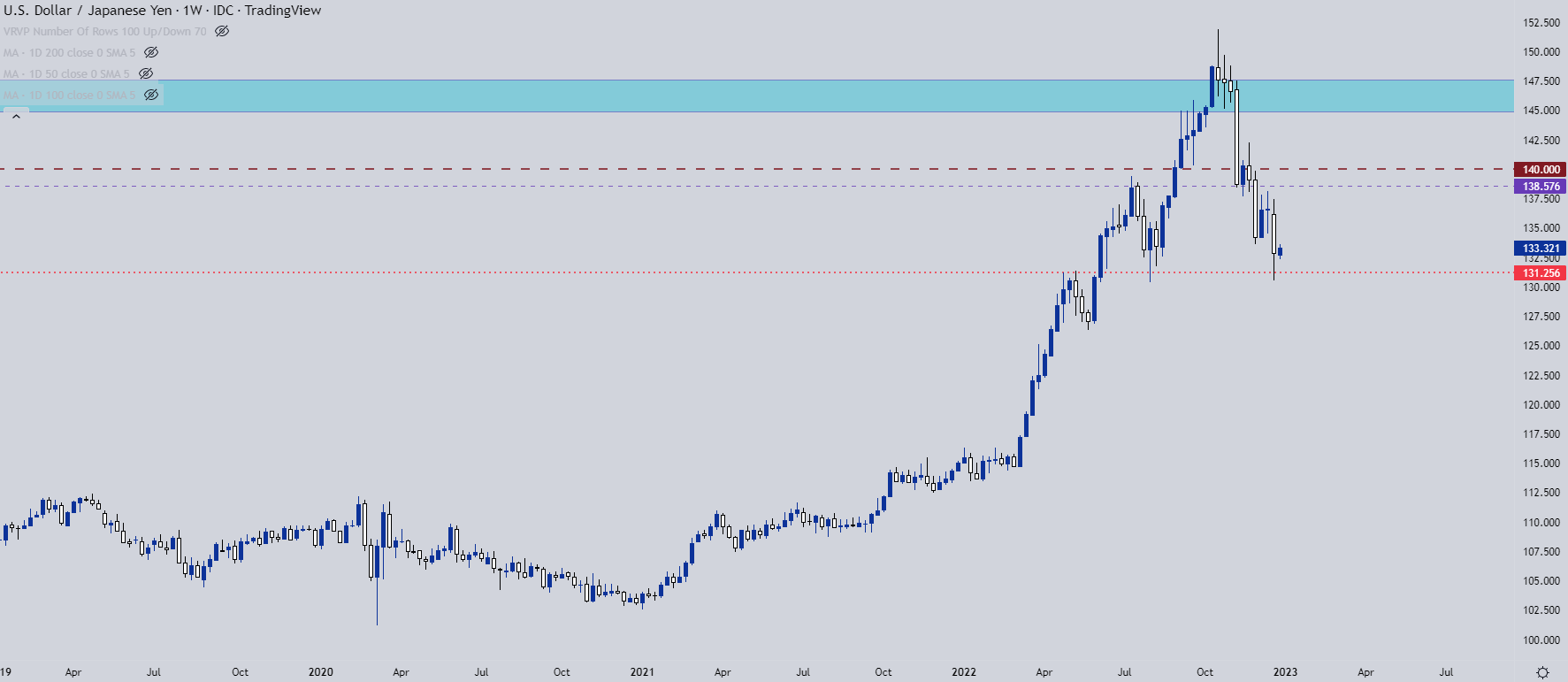

And perhaps more to the point, there’s an expected leadership change at the helm of the BoJ set to take place in the first-half of this year. As Kuroda steps down, might there be change on the horizon for the Bank of Japan? It seems unlikely that by the end of 2023 we have the same policy at the BoJ and it doesn’t seem as though they can go any looser than they’ve been. In USD/JPY, we can already see some of this anticipation priced-in, with price settling at support at a key price point from 2022 trade at 131.25.

More pressing, however, is how EUR/JPY or GBP/JPY might react, the latter of which I set up as a Top Trade for 2023.

USD/JPY Weekly Price Chart

Chart prepared by James Stanley; USDJPY on Tradingview

The Euro: Can the ECB Tame Inflation?

The Euro was on a threatening track through the first nine months of 2022 trade. Perhaps more to the point, from February into September, there was legitimate fear. After Russia invaded Ukraine, a number of possible risk factors flared. Inflation was already high in Europe but now there was the prospect of disruptions to food and energy supplies. European growth was weak, the ECB was afraid of choking off whatever growth was there by hiking rates to address inflation.

The ECB eventually came to the table with rate hikes in July and then started with heavier hikes in September. This started to bring some life back to the single currency and as we walk into the end of the year, the Euro has walked back from the proverbial ledge.

But this bounce is still very young and, frankly, we’re in the early stages of ECB rate hikes. Inflation remains brisk and European growth remains low, so the ECB is already nearing the difficult spot of having to hike rates in a recessionary backdrop, which is what’s taking place in the UK currently. The Bank of England has said that the economy is in recession, but with inflation remaining above 10%, the BoE has little choice but to continue to hike rates. The ECB is facing inflation over 10%, as well, putting a fragile economy in an even more difficult spot as Central Bank support becomes a more distant prospect.

Perhaps the bigger question for 2023 trade isn’t the Fed pivot – but the ECB pivot. Will the ECB be able to remain on a hawkish path, even as inflation holds above 10% without causing too much pain in the European economy? And the same can be said for the BoE, really, and this makes the prospect of Euro and GBP weakness as an attractive scenario for next year. And if meshed up with a strong JPY on the back of some form of change at the BoJ, there could be an amenable backdrop for bearish scenarios in EUR/JPY and GBP/JPY.

EUR/JPY Weekly Chart

Chart prepared by James Stanley; EURJPY on Tradingview

--- Written by James Stanley

Contact and follow James on Twitter: @JStanleyFX