S&P 500 – Talking Points

- S&P 500 sinks by 1% as traders brace for CPI on Thursday

- Fedspeak remains hawkish as FOMC looks to talk down market

- Bank earnings to set the tone for Q3 earnings season

Stocks are sliding to start the week as traders remain on edge ahead of Thursday’s US CPI print. Risk assets have struggled lately as markets once again are forced to digest the prospect that a Fed pivot is not imminent. With Fed Chair Jerome Powell not changing his tune from Jackson Hole, subsequent Fedspeak has reiterated the hawkish intent of the FOMC. Equities still continue to tread water as rates and FX markets continue to flash warning signs.

This week sees a significant amount of event risk, as traders will look to navigate Thursday’s US CPI print and the first wave of corporate earnings. While the market will likely be volatile into and after CPI, the market is effectively priced for 75 basis points in November, and the bar remains extremely high for this to change. Friday sees Citi, JP Morgan, Wells Fargo, and Morgan Stanley all report earnings. Bank CEO commentary will be key, as they will likely give key guidance on the state of the economy and the US consumer. While trading revenues may be elevated due to volatility, earnings may be dampened by loan loss provisions and slowing M&A activity.

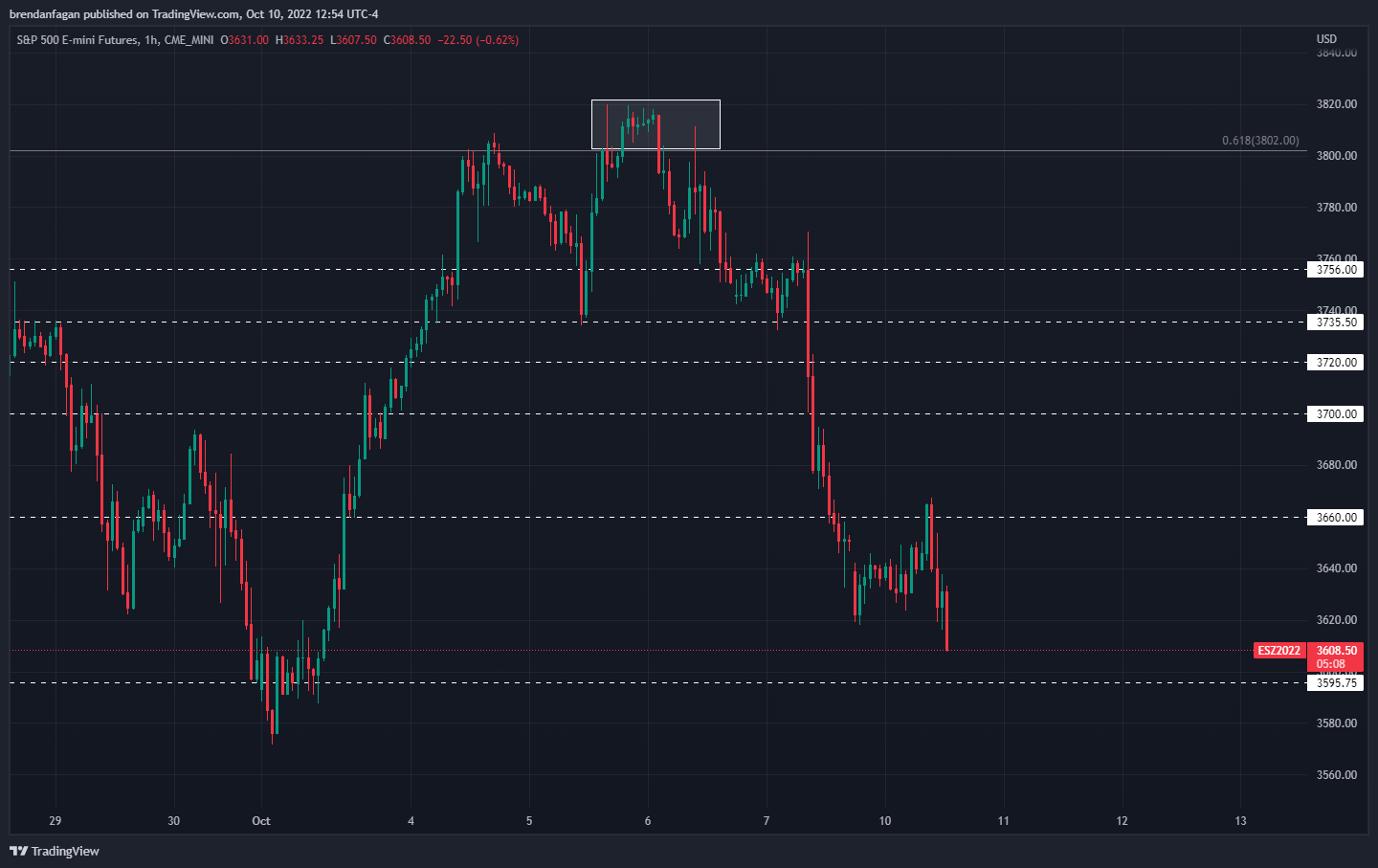

S&P 500 Futures 1 Hour Chart

Chart created with TradingView

After a stunning decline in Friday’s session following the nonfarm payrolls print, S&P 500 futures (ES) picked up on the Sunday open right where they left off on Friday. An initial gap lower was filled during the APAC session, but the brief rally into the 3660 area was promptly rejected following the opening bell in New York. As gravity continues to act on equity markets, slowly pulling the various benchmarks back to pre-pandemic levels, the path of least resistance continues to point lower.

With YTD lows for ES firmly in sight, poor sentiment and continued expectations of a hawkish Fed may see ES trade down to major Fib support around 3500. As interest rate volatility remains elevated, it remains difficult to see a period in which equities can mount a sustained rally. When your rallies are caused by short covering, it is safe to say your markets are under serious pressure. I continue to support the notion of selling into strength in this market, as equities continue to make a series of lower highs and lower lows on a longer timeframe.

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

RESOURCES FOR FOREX TRADERS

Whether you are a new or experienced trader, we have several resources available to help you; indicator for tracking trader sentiment, quarterly trading forecasts, analytical and educational webinars held daily, trading guides to help you improve trading performance, and one specifically for those who are new to forex.

--- Written by Brendan Fagan

To contact Brendan, use the comments section below or @BrendanFaganFX on Twitter