FTSE, DAX News and Analysis

- FTSE continues sharp sell-off, lead by Standard Charted and Barclays among others

- DAX suffers largest single day drop since December

- The analysis in this article makes use of chart patterns and key support and resistance levels. For more information visit our comprehensive education library

FTSE 100 Continues Sharp Sell-off, Led by Banks

Very few equity benchmarks have been able to withstand the contagion, which started in the banking sector and appears to have evolved into a broader ‘risk off’ move. Standard Chartered and Barclays suffered 6.6% and 5.67% declines at the time of writing. The FTSE index has substantial weighting in financial stocks (around 17%) meaning the index’s robustness from 2022 may come under pressure if the contagion isn’t contained.

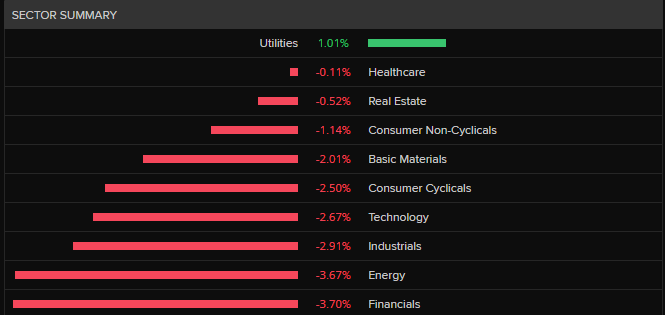

FTSE Sector Performance 13 March 2022

Source: Refinitiv, prepared by Richard Snow

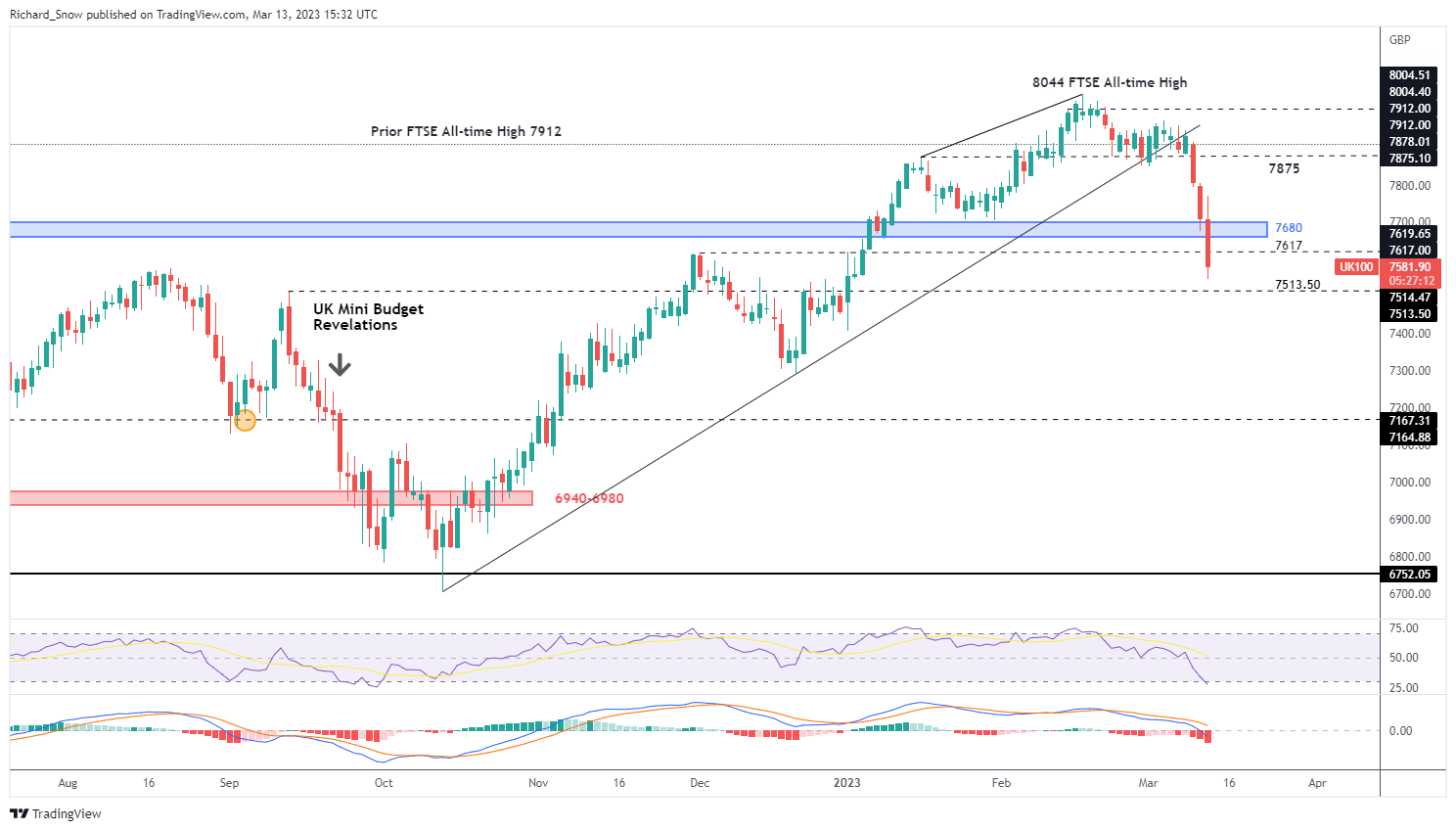

The FTSE chart reveals a continuation of the sizeable 4.2% sell-off that began on Thursday, breaking through levels of support with ease. The next level to note is the 7513.50 level which marks the September 2022 high. From there the December low of 7294 comes back into focus before 7167. The ‘oversold’ condition identified by the RSI does little to inspire confidence if we are in the early stages of a broader crisis. Resistance appears at prior support, 7617 and 7680.

FTSE 100 Daily Chart

Source: TradingView, prepared by Richard Snow

DAX Suffers Largest Single Day Drop Since December

The DAX was unable to hold off the risk off sentiment throughout global equity markets, sending the index considerably lower. Later this week the European Central Bank is due to announce an expected rate hike, 25 or 50 basis points. In the wake of the Silicon Valley Bank (SVB) and Signature Bank failures, the hawkish ECB will be forced to assess the impact of the larger 50 bps hike at a time of nervousness for global and European banks.

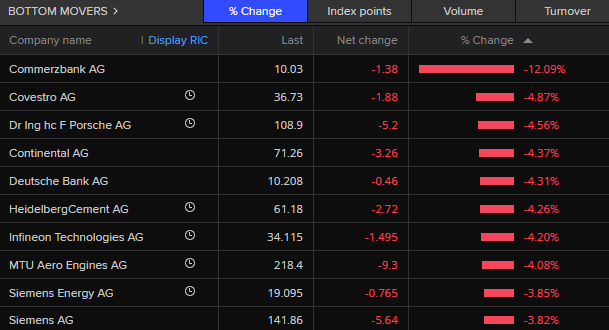

Biggest losers on the DAX include Commerzbank and Deutsche Bank, declining 12.09% and 4.31% respectively, at the time of writing.

Bottom Movers on the DAX

Source: Refinitiv, prepared by Richard Snow

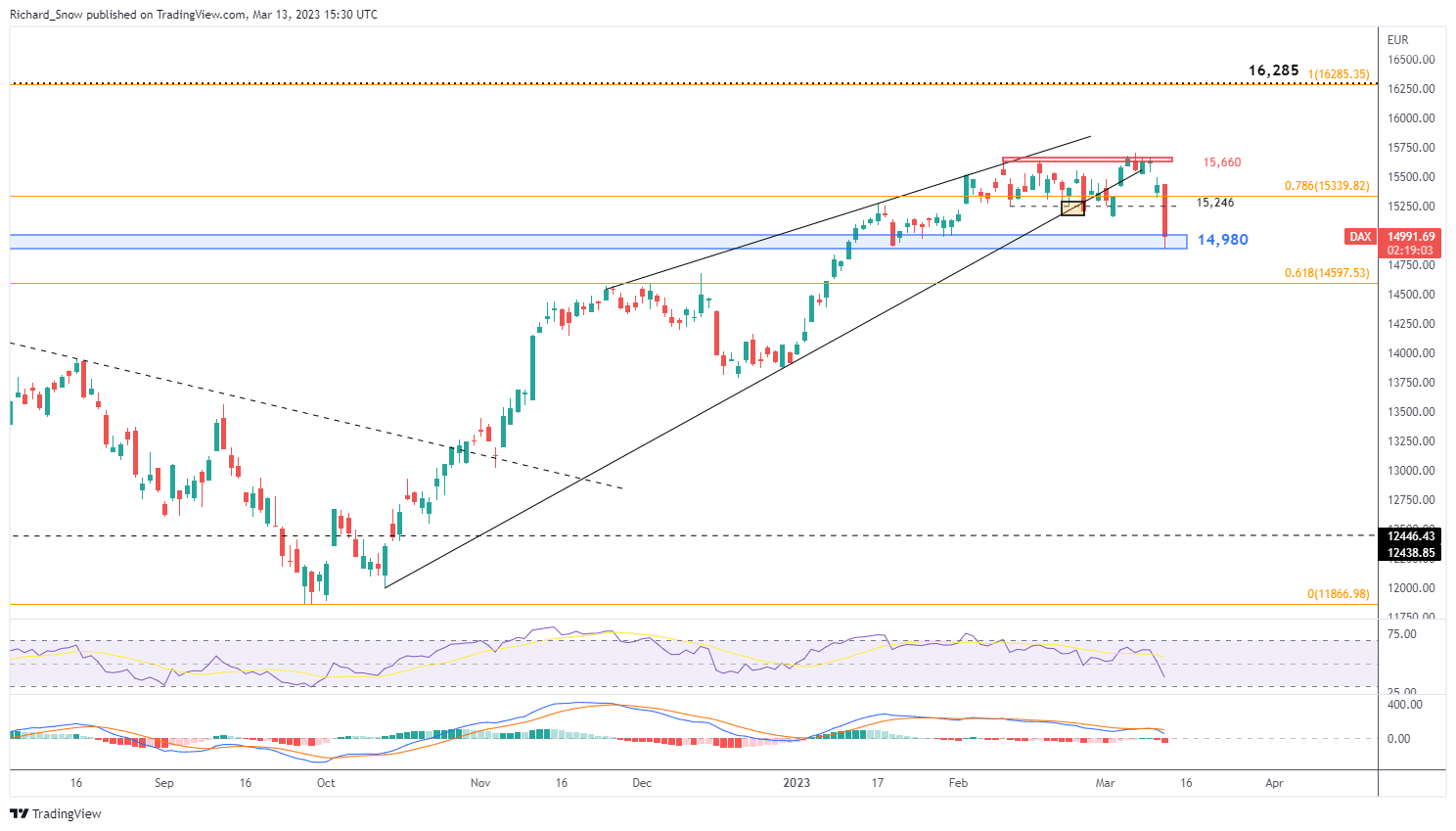

The German index had fared well compared to most until today where it has revealed a sharp 2.6% decline, making its way through levels of support with ease. The under-side of the consolidation zone at 15,246 failed to contain selling and price action now tests the zone of support around the psychological level of 15,000 flat.

Momentum has shifted and leans towards the recent bearish momentum and the RSI has not yes reached oversold levels, opening the door to further selling.

DAX Daily Chart

Source: TradingView, prepared by Richard Snow

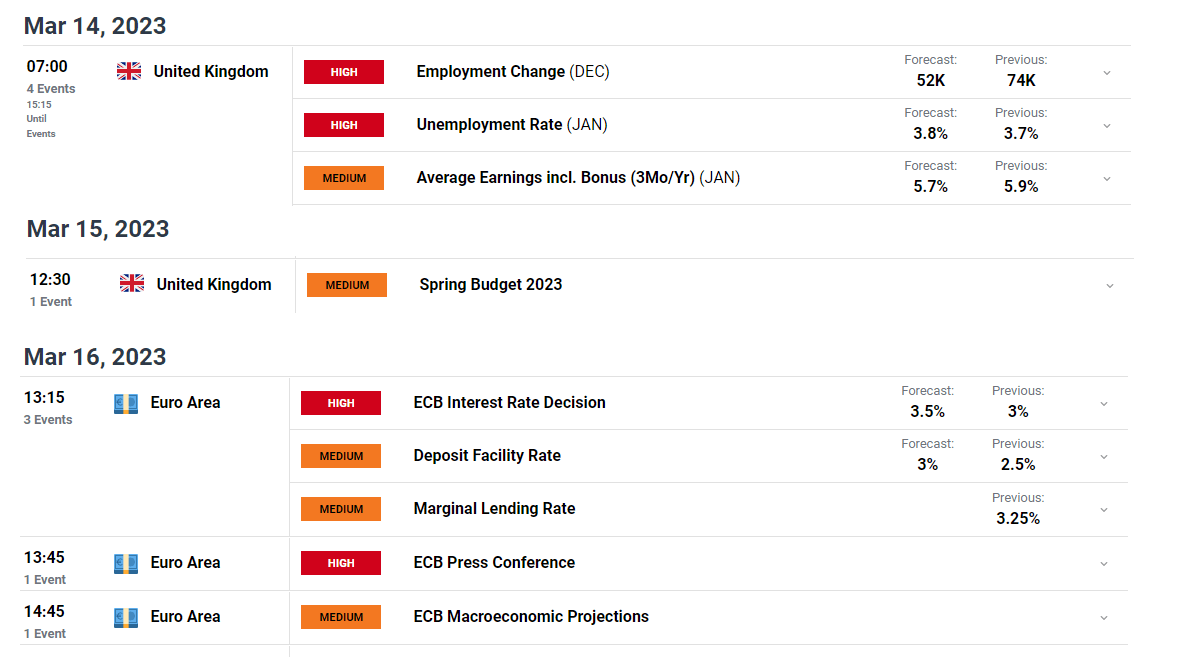

Major Risk Events

This week provides some important economic data/events within the UK and EU to add to the volatility of the banking stocks rout. Tomorrow, we get UK employment data and, possibly more importantly, we get insight into average earnings which had accelerated the most in more than 20 years and remains high up on the Bank of England’s concerns.

Wednesday ushers in the UK Budget Statement, where analysts suggest it may be a rather prudent exercise as the UK government has committed to reducing public debt over the next 5 years.

On Thursday, the European Central Bank (ECB) announces whether interest rates will rise by 50 or 25 bps. The bond market has revealed a sharp turnaround as implied probabilities now lean towards a 25 bps hike in light of the SVB failure. Just two weeks ago such an outcome seemed impossible given the continued hawkish rhetoric from governing council members, with one in particular calling for four 50 bps hikes. The picture is very different, which highlights how fast things can change when financial conditions tighten aggressively.

Customize and filter live economic data via our DailyFX economic calendar

--- Written by Richard Snow for DailyFX.com

Contact and follow Richard on Twitter: @RichardSnowFX