Crude Oil, US Dollar, British Pound, GBP/USD, BoE, USD/JPY, Gold, - Talking Points

- Crude oil prices took a breather from being pummelled today

- US Dollar eased after recent rampant rallies as markets take stock

- Central banks are the focus for price action. Will crude get caught in the melee?

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Crude oil is under pressure as perceptions of global growth going forward continue to be questioned with interest rates soaring again today.

Overnight, Federal Reserve Bank of Cleveland President Loretta Mester re-iterated the higher for longer rates mantra, sending yields up across the curve.

The 10-year Treasury yield is at its highest since 2010, trading as high as 3.93% today. Bonds in all developed markets are lower in price and higher in yield.

This tightening of economic conditions has the WTI futures contract near US$ 77 bbl while the Brent contract is a touch below US$ 85 bbl.

The US Dollar is a bit weaker through the Asian session today but is still generally above where it started the week against most currencies and other risk assets. Most notably, GBP/USD is still struggling to gain traction.

Yesterday’s statement from the Bank of England (BoE) has done little to allay market concerns for the viability of the UK government’s new fiscal policy revealed last Friday.

Fiscal loosening at the same time as monetary tightening would seem to be an unorthodox approach to managing a nation's economy. Sterling and Gilts have been hit hard as markets question the logic of this strategy.

USD/JPY continues to edge toward 145 despite the Bank of Japan (BoJ) announcing an unscheduled round of bond purchases. A move above 145 will be closely monitored for another round of physical FX intervention from the BoJ

RBNZ Governor Adrian Orr hinted that rate rises might be tapering when he said, “the tightening cycle is very mature.” Kiwi is a touch higher today on the softer US Dollar.

Gold is slightly firmer, nudging above US$ 1,630 going into the European session. APAC equities were fairly stable today and futures are pricing in a mildly positive start to the US cash session.

There are a number of speakers from the European Central Bank, BoE and the Fed crossing the wires today. Of note will be the BoE’s Chief Economist Huw Pill and Fed Chair Jerome Powell.

The full economic calendar can be viewed here.

{{GUIDE|HOW_TO_TRADE_CRUDE_OIL}}

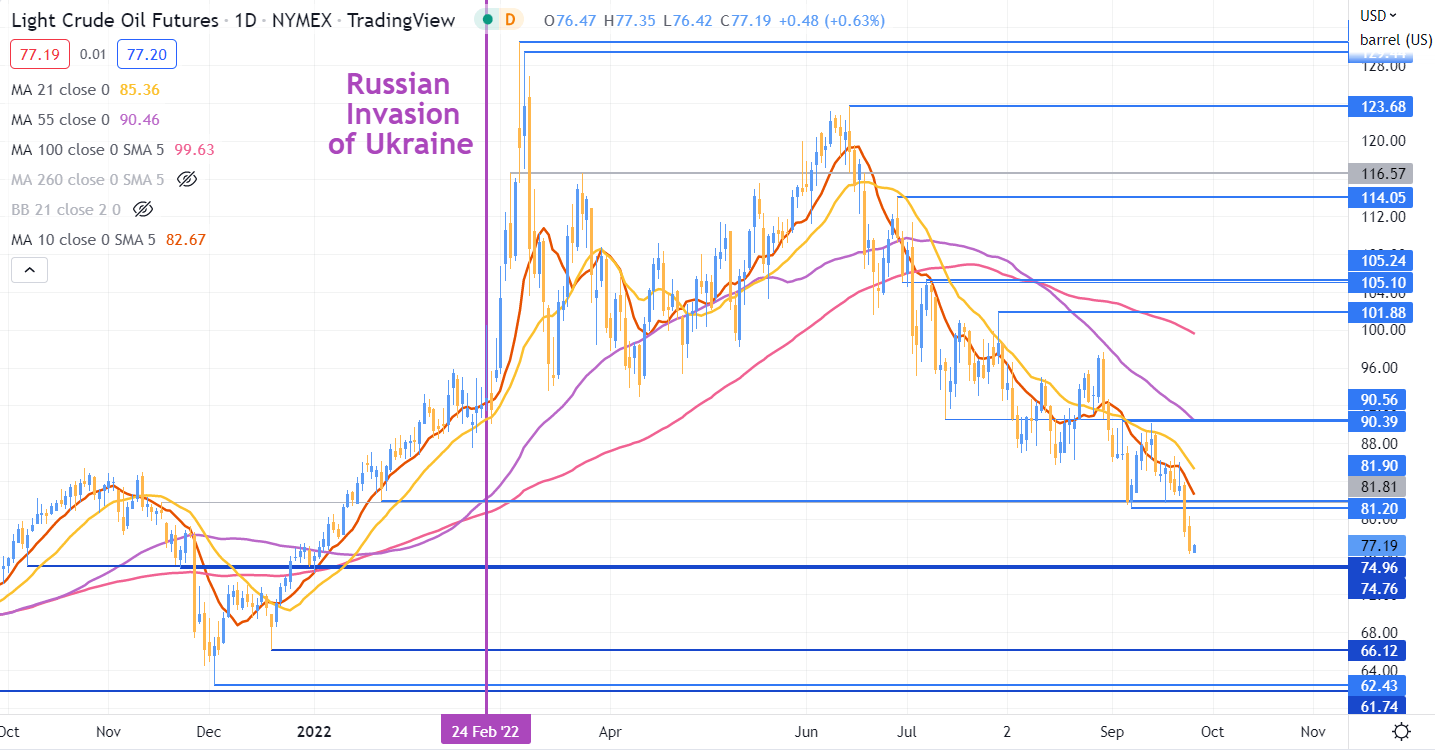

WTI CRUDE OIL TECHNICAL ANALYSIS

WTI crude oil is back to levels seen in January and the impact of the Ukraine war is unwound.

Bearish momentum might be evolving with a number of simple moving averages (SMA) above the price and displaying negative gradients.

Support could be at the historical break point zone in the 74.76 – 74.96 area.

On the topside, resistance could be at the break points of 81.20 and 81.90.

--- Written by Daniel McCarthy, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @DanMcCathyFX on Twitter