Wall Street managed to start the new week on a positive footing, but with some slight caution ahead of the key US CPI data release tomorrow as the S&P 500 VIX saw an in-tandem rise overnight (+1.6%). Nevertheless, the DJIA has pulled ahead with a 0.6% gain versus the Nasdaq’s 0.2% and with chatters of growth sectors doing the heavy-lifting for indices since the start of the year, more participation from value sectors ahead may bode well for the broader market strength. Thus far, the DJIA has yet to reclaim its December 2022 high.

Overnight, a series of Fedspeak largely confirmed market rate expectations of what is to come at the upcoming Fed meeting – a potential 25 basis-point (bp) hike followed by a prolonged rate pause through the rest of the year. The comments from Fed official Michael Barr, Raphael Bostic and Loretta Mester called for further rate increases but also indicated that the end of the Fed’s tightening cycle is in sight. The no-surprise saw Treasury yields reacted to the downside, with a retreat in the ten-year yields from its March 2023 high while the two-year yields also declined 9 bp, overall weakening the US dollar further.

Perhaps one to keep an eye on will be the significant underperformance in US May consumer credit (+US$7.24 billion vs +US$20.25 billion consensus), which highlight downside risks of a slowing consumer outlook. But at least for now, with still some pockets of resilience in the US economy, it may have to take more to challenge hopes of a soft landing.

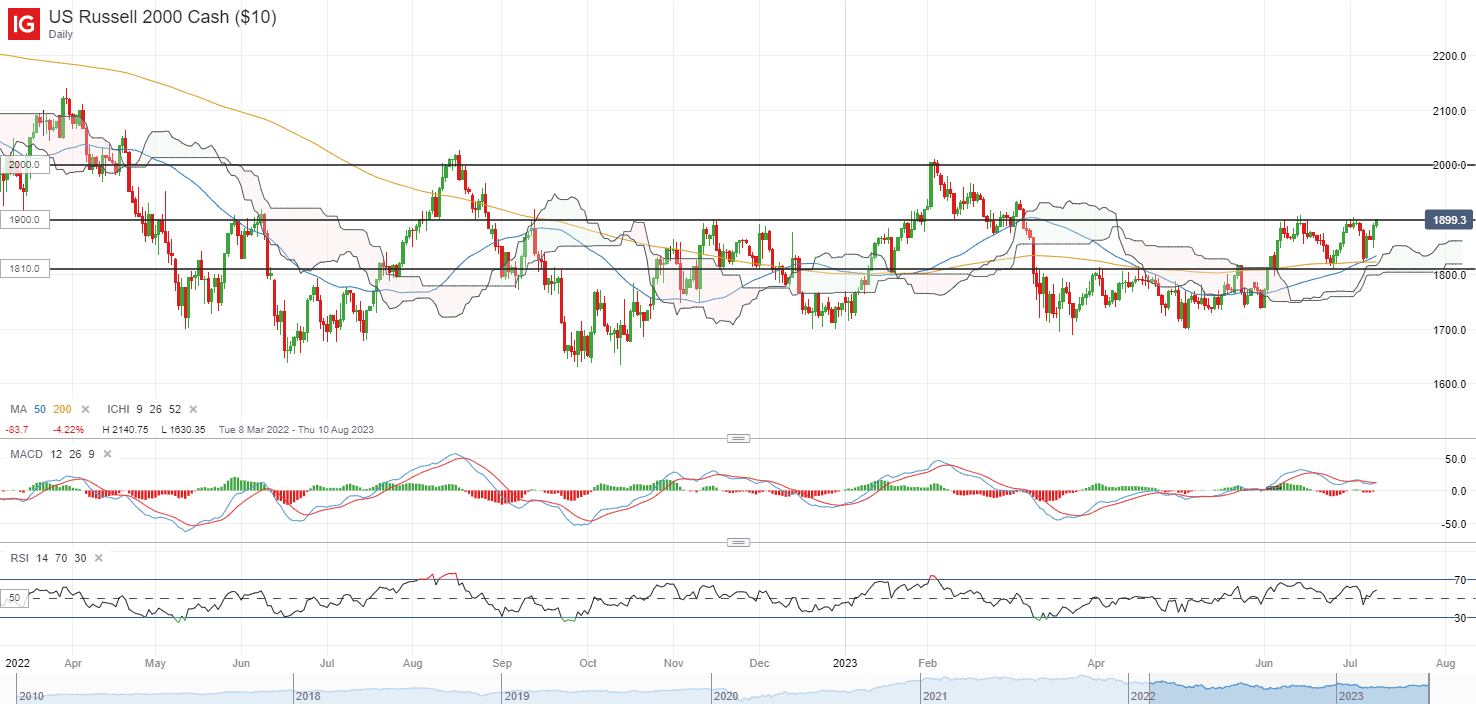

The Russell 2000 index is currently back to retest its 1,900 level of resistance for the fourth occasion since June this year. Multiple retests of resistance over a relatively short span of time may drain the supplies of sellers at that level and raise the odds of an upward break. Any successful move above the 1,900 level may pave the way to retest its year-to-date high at around the 2,000 psychological level next.

Source: IG charts

Asia Open

Asian stocks look set for a positive open, with Nikkei +0.58%, ASX +0.88% and KOSPI +1.09% at the time of writing. Chinese equities has displayed some resilience yesterday despite a set of lacklustre inflation figures reinforcing the slowing economic outlook, as the data was perceived to provide more room for supportive measures over the coming months. There was a slight glimpse of that in its property market overnight, with China authorities extending loan relief and stepping up pressure on financial institutions to ease terms for property companies to ensure that homes construction are completed.

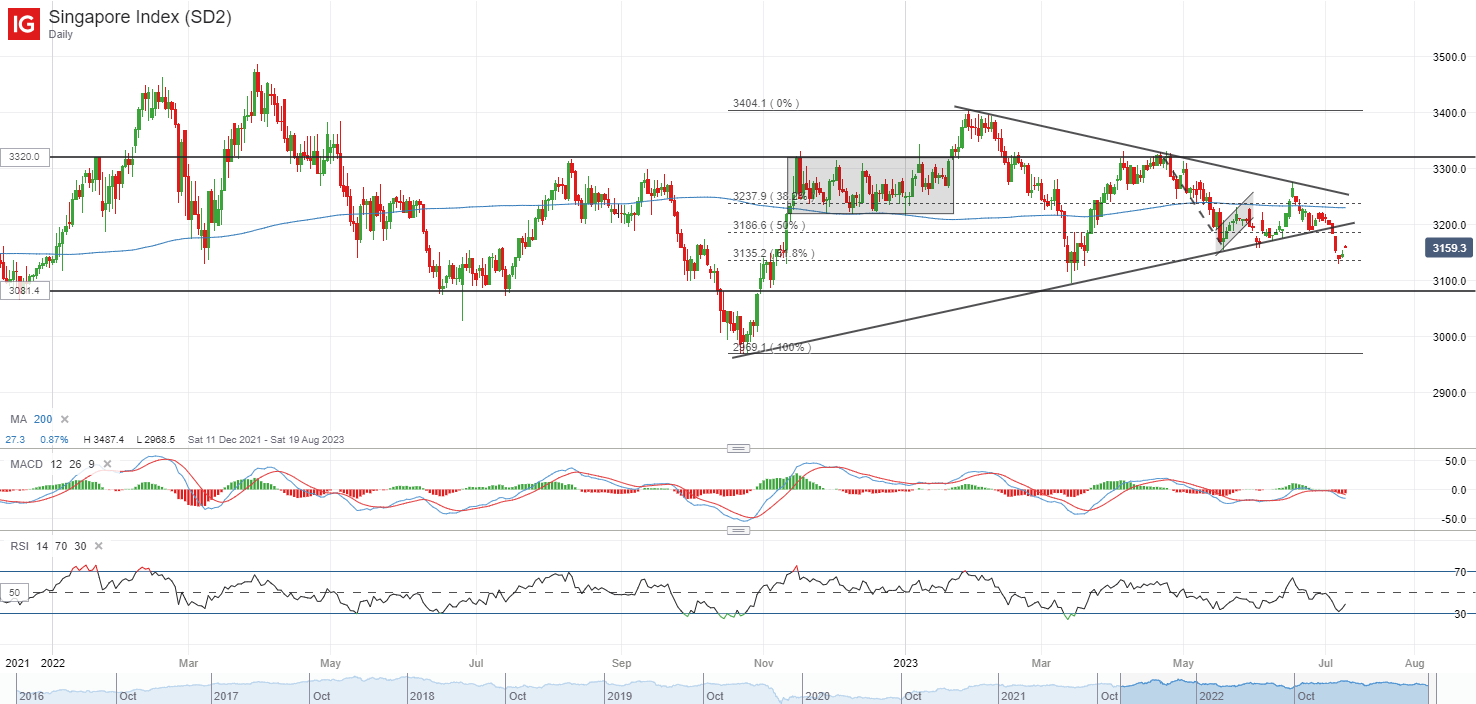

Closer to home, the latest SGX fund flow data has revealed S$109 million net outflows from institutional investors last week, bringing the past four weeks’ net outflows to S$314 million. Further paring of exposure in financial services (-S$89 million) and REITs (-S$45.1 million) were presented. On the technical chart, the lower trendline of a symmetrical triangle pattern has been broken down last week, putting sellers in control after months of indecision. While the index may attempt to tap on the broader risk environment for some intermittent bounces, the overall bias leans to the downside for now, with declining MACD below zero and RSI below the key 50 level.

Source: SGX, IG

Source: IG charts

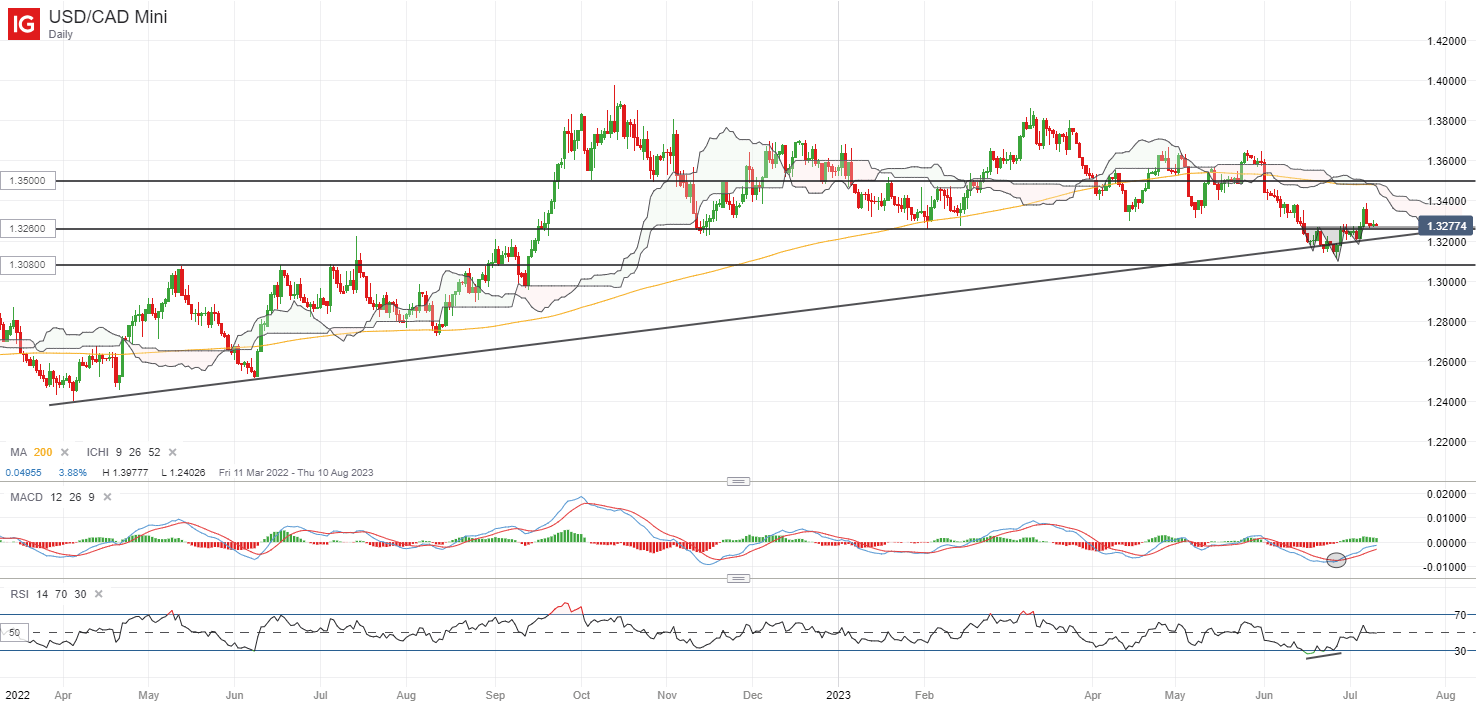

On the watchlist: USD/CAD retesting key support ahead of Bank of Canada (BoC) meeting this week

Ahead of the BoC meeting on Wednesday, the USD/CAD is hanging at its key support at the 1.326 level, with rising MACD and a reclaim of the RSI above its 50 level lately suggesting buyers’ attempt to take back some control following a 4% sell-off since June this year. Current expectations are leaning towards another 25 basis-point hike from the BoC at its upcoming meeting, but signs of a softer labour market and receding inflation have called for a prolonged rate pause thereafter. Any confirmation of the central bank heading towards a pause once more may be viewed as less hawkish, which could drive the CAD lower.

For the USD/CAD, the 1.326 level may be a crucial support to hold, where it serves as the neckline of a minor inverse head-and-shoulder formation, in coincidence with a key horizontal support. Defending this level may form a new near-term higher low and leaves the 1.350 level on watch next.

Source: IG charts

Monday: DJIA +0.62%; S&P 500 +0.24%; Nasdaq +0.18%, DAX +0.45%, FTSE +0.23%