US CPI Preview:

- Consensus forecasts are looking for headline US inflation to come in at +8.1% y/y and the core reading to come in at +6.5% y/y.

- At present time, rates markets are favoring a 75-bps rate hike at the next Federal Reserve rate decision in November.

- We’ll discuss the impact of the September US inflation report on the US Dollar, gold prices, and US stocks starting at 8:15 EDT/12:15 GMT on Thursday, October 13, 2022. You can join live by watching the stream at the top of this note.

Inflation May Not Have Peaked

The upcoming September US inflation report (consumer price index) might offer only scant evidence that peak inflation is in the rearview mirror. According to a Bloomberg News survey, headline US inflation figures are due in at +0.2% m/m from +0.1% m/m and +8.1% y/y from +8.3% y/y, while core readings are expected at +0.5% m/m from +0.6% m/m and +6.5% y/y from +6.3% y/y.

Stubborn readings could translate into sustained elevation in Fed rate hike odds, which while good news for the US Dollar, will likely not be the case for US stocks and gold prices.

How Will the Fed Respond?

The Federal Reserve has raised rates by 300 basis points this year, with another 75-bps effectively priced for the November FOMC meeting. While there is a “long and variable lag” between a rate hike and when it filters through to the economy, there are fresh signs that the economy could be beginning to cool.

Consumer inflation expectations dropped sharply in September, as the Federal Reserve continues to move aggressively to prevent inflation from becoming entrenched. 12-month inflation expectations fell to 5.4%, down from 5.75% in August. Despite this, 3-year inflation expectations did tick higher to 2.9%, up 0.1% from August’s survey. As we continue to remain some ways off of the Fed’s 2% inflation target, signs continue to indicate that inflation may remain elevated for some time.

The NY Fed survey showed that household spending growth for the next 12-months is expected to be +6%, down sharply from August’s forecast of +7.8%. Survey respondents notably said that they only expect home prices to rise by +2%, the lowest print since June 2020. Recent tightening has seen 30-year mortgage rates skyrocket to 7% as the Fed looks to cool a robust housing market. Consumers also see notable increases in gas and food costs, rising by +0.5% and +6.9% over the next 12-months, respectively.

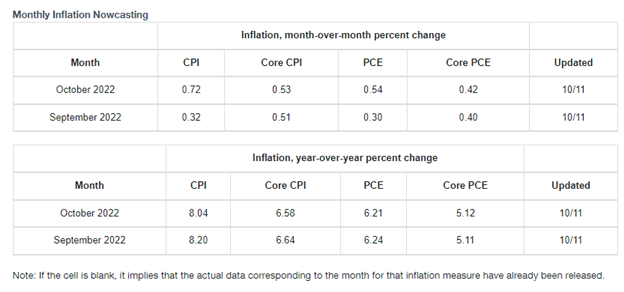

Cleveland Fed Inflation Dashboard (October 11, 2022) (Chart 1)

According to the Cleveland Fed inflation nowcasting tool, the US economy experienced headline inflation of +0.32% m/m and +8.2% y/y in September, with core inflation at +0.51% m/m and +6.64% y/y. It should also be noted that headline 3Q’22 US inflation came in at an annualized rate of +5.59%while the core reading settled at 6.35%.

We’ll discuss the impact of the September US inflation report on financial markets starting at 8:15 EDT/12:15 GMT on Thursday, October 13, 2022. You can join live by watching the stream at the top of this note.

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

--- Written by Christopher Vecchio, CFA, Senior Strategist and Brendan Fagan, Research Contributor