S&P 500, FOMC, Dollar, USDJPY and GBPUSD Talking Points:

- The Trade Perspective: S&P 500 Bearish Below 4,075; USDJPY Bearish Below 134.00

- The Federal Reserve hiked its benchmark rate 75 basis points – the biggest increase since 1994 – in a bid to combat inflation

- Despite the tightening of financial conditions, the S&P 500 managed ended Wednesday higher; but be wary of opportunism on risk assets as recession warnings grow

That’s Not How the Basic Playbook Says the Markets Should Have Reacted

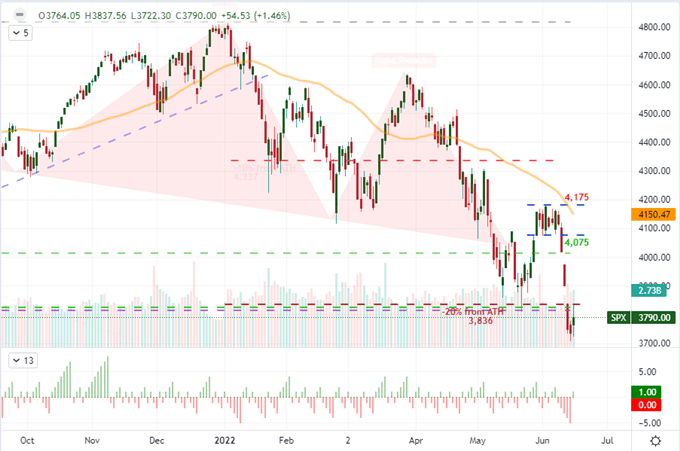

We have passed from the ‘before Fed’ era into the ‘after hike’ epoch. As a very basic assessment of what the US central bank announced Wednesday afternoon: the 75 basis point (0.75 percent) hike was the biggest increase since 1994 and their official forecast for interest rates through the rest of the year, and beyond, was revised sharply higher. By all accounts, that was a major hawkish shift. Yet, if you look at the markets most sensitive to this policy event – my preferred measures are the S&P 500 and US Dollar – the response looks like the kind of reaction you’d expect from a dovish outcome. Looking to the US index, it wouldn’t hold on to its full intraday gains nor climb its way back up to retake the technical level that triggered the ‘bear market’ designation we currently hold; but it was nevertheless a 1.5 percent advance. I won’t draw dubious comparisons to a similar break of a five-day slide from the SPX back in January that was a brief reprieve before we fell fully into a bear trend, but the fundamental and conditional backdrop make the comparison far more meaningful than bulls should be comfortable with. I still believe the prevailing trend in 2022 is bearish, but there is room for a bounce. Yet, if this benchmark can’t retake 3,835, the hope for even a passing bear market bonce will quickly fall apart.

Chart of S&P 500 with 20-Day SMA with Volume and Consecutive Day Moves (Daily)

Chart Created on Tradingview Platform

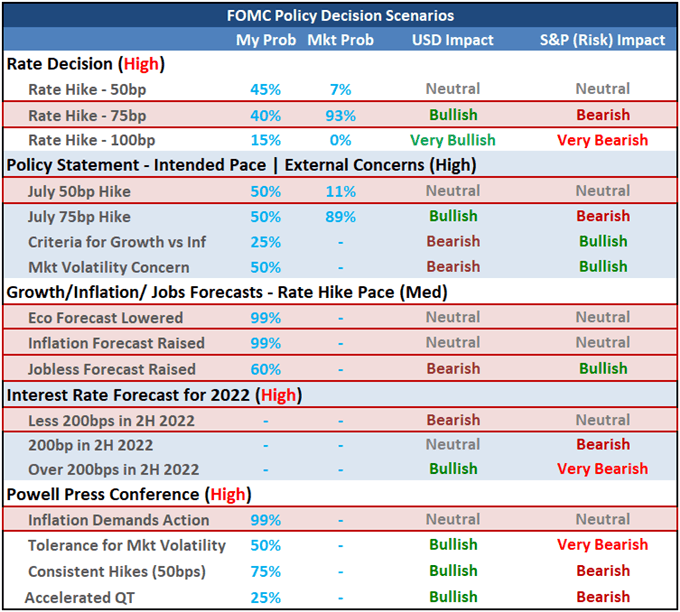

With the market’s response considered first, let’s now talk about the Federal Open Market Committee’s (FOMC) actual policy mix. First and foremost, the group did announce a 0.75 percent hike to raise the benchmark range to 1.50-1.75 percent. While that is an extraordinary milestone on a historical basis, it wasn’t exactly a shock to the markets. While I thought the spread of possible outcomes (50, 75 and 100 basis points) was a little more evenly distributed, Fed Fund futures had all but priced in this particular outcome. The US CPI and UofM sentiment survey on Friday bolstered the risk/probability, but it was also the likely strategic leak to WSJ’s Nick Timiraos to get around the technical embargo which stunted their typical channel of forward guidance. While there were other interesting elements to this monetary policy meeting, it was the official rate forecast though year’s end from the Summary of Economic Projections (SEP) which seems to have had the greatest sway. My focus was on whether the forecast was greater than, equal to or lower than a forecast for another 200bp worth of hikes in the second half of the year. As it happens, after the big rate hike this past session, the forecast shifted to ‘lower than’. It is that opening which offers some very short-term ‘relief’.

Table of FOMC Policy Decision Scenarios and Market Response

Chart Created by John Kicklighter

Rate Expectations and the US Dollar

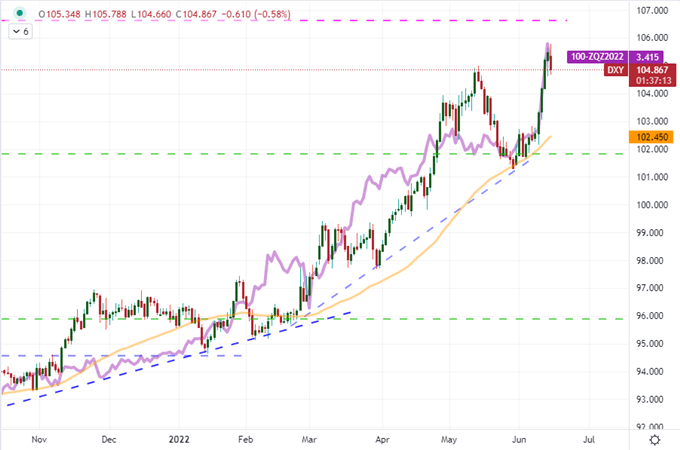

The forecast for risk trends after this mixed overview of Fed policy is reasonably disjoined; but what about the US Dollar. Looking at the currency objectively, the trade-weighted DXY index suffered a hearty retreat from its approximately two-decade highs following a five-day rally. Rate forecasts have certainly picked up behind the Greenback, but there has also been a tangible build up in purely safe haven interest behind the currency. With the ebb in capital market fear, there is reason to ease up on the Greenback’s ‘last resort’ bid. While I believe sentiment has a serious capacity for returning to its prevailing bear trend, my confidence in a rebound bid for the currency is far more constrained. The problem is not that the Dollar doesn’t have haven properties nor that the Fed isn’t committed; rather the rate forecast for the US is far from unique amid so much hawkish policy lean. Further, with a pair like EURUSD on the cusp of a two decade low around 1.0635 and USDJPY pushing similarly historic highest just below 136, the US currency is not in exactly trading at a discount.

Chart of the DXY Dollar Index Overlaid with the Implied Rate from Fed Fund Futures Year End (Daily)

Chart Created on Tradingview Platform

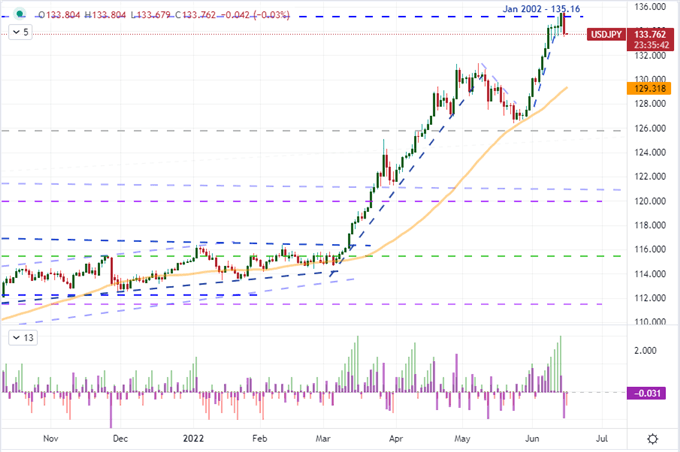

With EURUSD, we know that the gap in policy bearings is beginning to close – albeit slowly. While the ECB is not running anywhere close to the pace of its US counterpart, it has nevertheless turned the corner on its extremely accommodative policy with last week’s warning that inflation would lead to rate hikes in 2H 2022. In fact, that warning has led the markets to respond across the financial spectrum including an acute rally in European yields. The pressure seems to have been so acute that the ECB called an emergency meeting Wednesday at which they discussed a vague program aimed at curbing excessive yield spreads. Meanwhile, the BOJ has offered no such reassurances. The contrast between the Fed’s and BOJ’s policy bearings are exceptionally different, and we see that playing out in USDJPY price action pushing to highest not seen since October 1998. That said, the Fed outlook and risk appetite combo made for a very interesting USDJPY session Wednesday. The second biggest single day drop from USDJPY in 7 months was technically notable, but is was more importantly a sharp retreat from significant highs. There is plenty of reason for further pullback here, but I am looking for technical confirmation to suggest the market will extend its retreat.

Chart of USDJPY with 20-Day SMA and Consecutive Candle (Daily)

Chart Created on Tradingview Platform

Life Does Not End With the Fed…

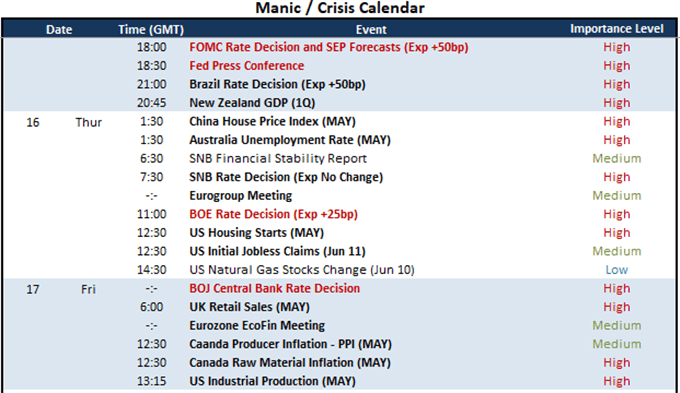

…but the US central bank policy decision will nevertheless continue to influence market activity for weeks and months to come. That said, the macro economic outlook will stir different opportunities of focus moving forward. We have already registered the influence of Brazil’s confirmed 50bp rate hike, New Zealand’s weaker-than-expected 1Q GDP reading and a significant beat in the Aussie employment data – all without a dramatic market response from their respective markets or currency. That fundamental response curb may end starting tomorrow with a run of major central bank policy insight starting with the Swiss National Bank’s (SNB) update. This group is not expected to announce any changes, but its general strategy has boiled down to ‘doing just a little more than the ECB’. That said, with ECB President Lagarde warning that rate hikes are ahead, perhaps the Swiss authorities are considering where and when it would be appropriate to tighten to combat inflation without triggering EURCHF fallout.

Calendar of Major Macro Economic Event Risk

Calendar Created by John Kicklighter

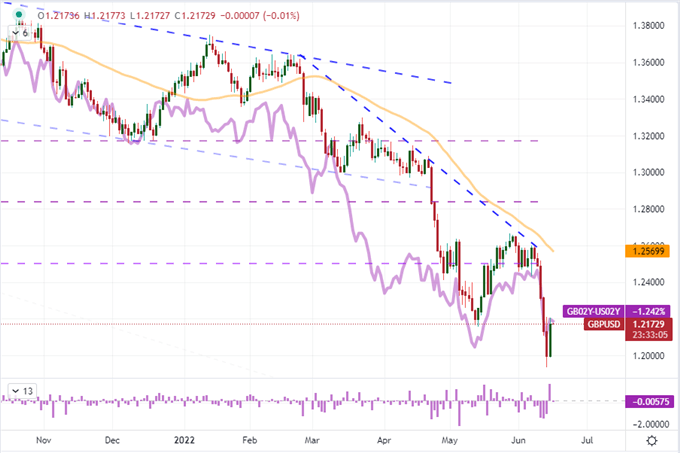

While the SNB decision is interesting, the BOE (Bank of England) policy call will likely exert greater market response beyond local markets. In the wake of the Fed’s 75bp move – which pushed it to the second most hawkish of the major groups’ policy stances – the forecast for a 25bp hike from the MPC makes its effort look paltry. That isn’t exactly a screaming endorsement for a Cable rally, but GBPUSD still posted its biggest rally (1.51 percent) since October 21, 2020. If the UK central bank does indeed take a small step forward to combat inflation that has urged the Fed to a sharp hike and the ECB to capitulate, I wouldn’t expect the bid on the Pound to last for too long. A little further on the curve, it would be wise to keep tabs on the BOJ rate decision due for release Friday morning in Tokyo. It is unlikely that policy changes here, but that is in itself a problem between inflation pressures and the pressure on expensive and necessary imports.

Chart of GBPUSD Overlaid with the UK-US 2-Year Yield Differential and 1-Day ROC (Daily)