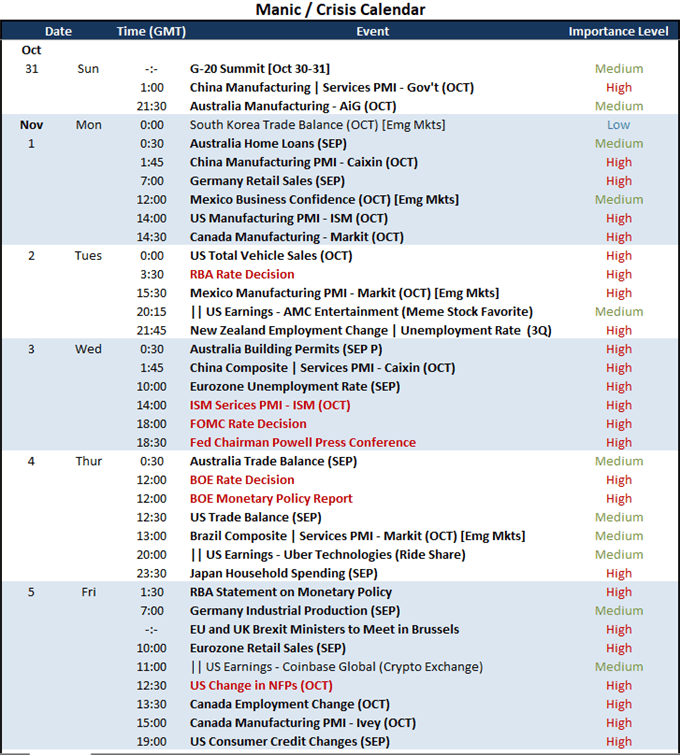

S&P 500, VEU ETF, Fed Decision, EURUSD and GBPAUD Talking Points

- The S&P 500, Dow and Nasdaq 100 all managed to end the week at all-time highs despite the added concern of Amazon and Apple earnings misses

- Risk appetite is not progressing evenly, which draws even sharper focus on the speculative charge of the US stock market as fundamental drag builds

- There is a clear theme to focus on in the week ahead in monetary policy while the Federal Reserve’s expected taper announcement is top event risk

US Indices Stray Further and Further from General Sentiment Trends

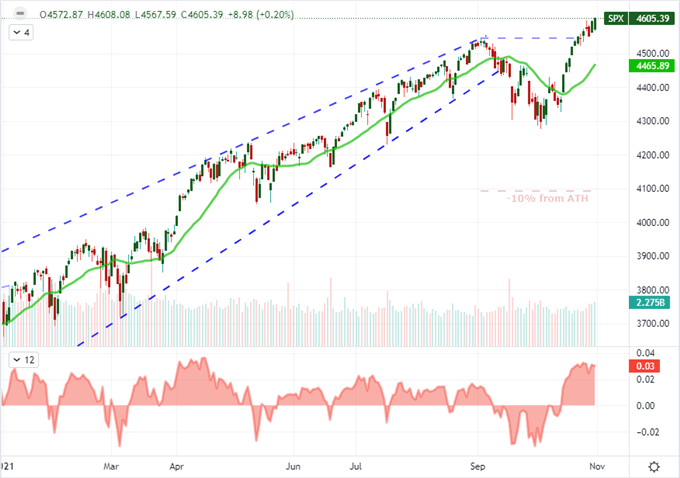

Through numerous fundamental hurdles this past week, the benchmark US equity indices – the S&P 500, Dow Jones Industrial Average and Nasdaq 100 – managed to notch record high closes Friday. Despite a flagging economic growth pace and recognition that global monetary policy was turning the corner, momentum persisted. Even the previously unflappable support from earnings reflected a threat speculative threat that traders readily parried. An optimist would say this is a sign that the market is exceptionally robust and has priced in all the negative news with a view that the opportunity still outstrips the risks ahead. I am not an optimist by nature, and so consider it a progress of complacency that progresses so long as nothing meaningful threatens the apathy. There remain such risks ahead.

Chart of S&P 500 with 20-Day SMA and Disparity Index (Daily)

Chart Created on Tradingview Platform

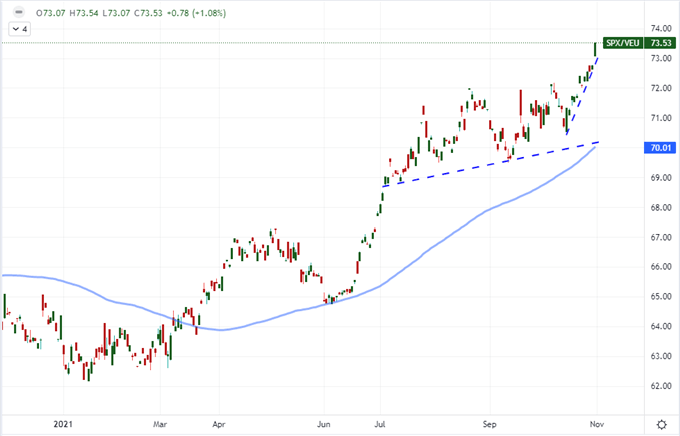

Beyond the pressure that will be exerted on general market confidence, there also remains a glaring disparity in perspective represented by US stocks and the course for the rest of the spectrum of ‘risk’ leaning markets across the world and across asset types. I’ve discussed repeatedly the outperformance of the tech-heavy Nasdaq 100 versus just the so-called ‘value index’ of the Dow, pushing us to levels last seen since the Dot-com boom and bust. Beyond the speculative concentration highlighted between these close peers, the charge to fresh record premium for US equities relative to global counterparts (S&P 500 to the VEU ETF below) makes an even more dramatic impression.

Chart of S&P 500 to VEU ‘Rest of World’ Equity ETF Ratio and 100-Day SMA (Daily)

Chart Created on Tradingview Platform

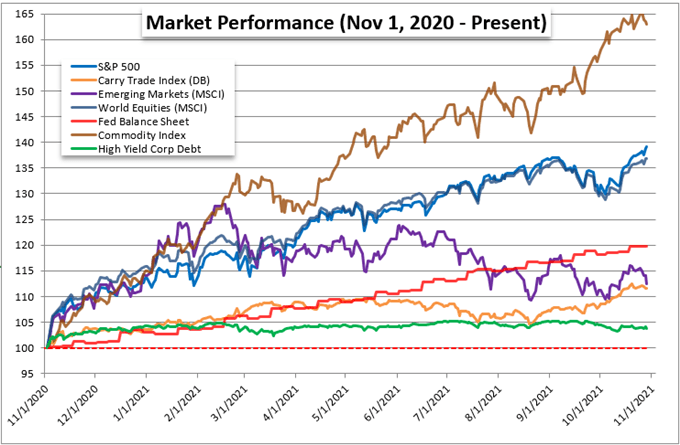

As remarkable as the disparity in US and global stocks may be, my benchmark for global investor sentiment is the degree of correlation and intensity of move across various assets across the world that tend to align to the ‘risk on, risk off’ model when speculative conviction is charged. Below, we have a range of popular asset types that align to the theme, but further show a widening divergence to stocks overall. Emerging markets, junk bonds and carry trade are all showing a distinct struggle relatively speaking amid the shift in global monetary policy and a slowing pace of economic recovery. The exception is commodity prices, but this is more likely an indication of unwanted inflation pressure rather than a reflection of speculative intent.

Chart of Relative 12-Month Performance of Various ‘Risk’ Benchmarks (Daily)

Chart Created by John Kicklighter with Data from Bloomberg

What Will Steer the Markets Ahead: Complacency or Systemic Fundamentals?

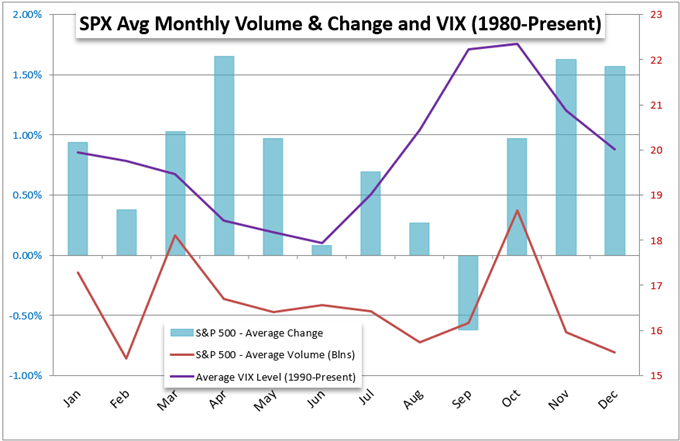

While it may not be delivering a consistent benefit, risk appetite is still offering a favorable course setting across the financial markets. Often times, there is an existent course setting for sentiment such that the bias can filter the incoming fundamental updates by leveraging the weight of news that reinforces pre-conceived views and downgrades those that conflict. At present, it seems like the market is simply overlooking brewing trouble which does not set a strong course for continuity for the likes of the S&P 500 – much less encourage other assets to follow its lead. Perhaps the most familiar argument for a ‘complacent’ bullish momentum is the seasonal perspective which has shown the S&P 500 has historically advanced through November and December while volume and volatility tend to fade. This is statistically relevant, but would it really hold up against a serious fundamental threat?

S&P 500 Performance, Volume and Volatility Monthly Seasonality

Chart Created by John Kicklighter with Data from Bloomberg

On the other hand, the economic docket through the coming week has quite the run of run of ‘high’ and ‘medium’ level of event risk. Last week, there were multiple, high-level themes that carried the fundamental weight that could steer the market to a systemic course correction – much less charge targeted volatility. While there are plenty of individual listings that I would point out as capable of generating volatility for specific currencies, local capital markets or specific equity sectors; there is only one universal theme that I would hold above all else: monetary policy. Earnings is slowing down after last week’s tech giants reported. Economic health has been updated with October PMIs as well as the official 3Q GDP figures from the US, Eurozone and China. That leaves a string of three key central bank updates where expectations have grown unmistakably hawkish.

Calendar of Major Macro Event Risk for the Week

Calendar Created by John Kicklighter

Monetary Policy Has Turned the Corner and the Fed Represents the Core

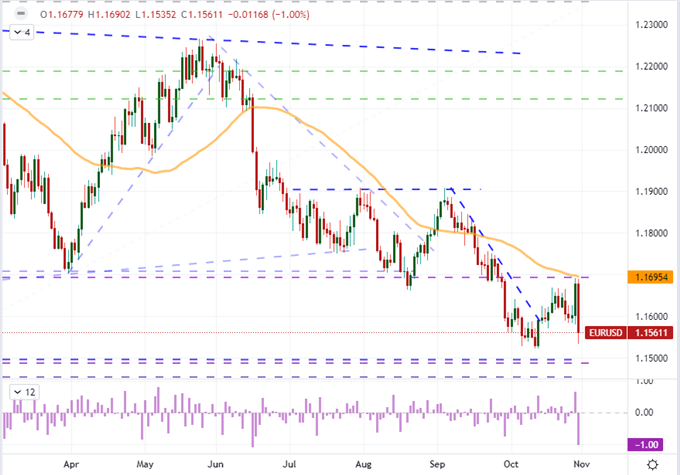

While the ISM services sector survey and Friday’s NFPs are critical event risk for the Dollar and US markets this week, there is no doubt that the Federal Reserve’s monetary policy meeting is the principal concern of the global markets. This is not one of the so-called ‘quarterly’ meetings where the standard rate decision and monetary policy statement is accompanied by updated forecasts in the Summary of Economic Projections. Yet, that forward guidance matters a lot less when the event itself is expected to result in an important change. While the Fed is not on course to change its rates for at least a few quarters, it is very likely to announce its taper plan. That means the central bank will lay out its schedule for reducing its monthly asset purchases (currently $120 billion) – a critical policy adaptation before the eventual first rate hikes. This now seems to be the baseline case expected by the market and we find the rate forecast in Fed Funds futures and swaps reflect the accelerated time frame. That said, FX traders will have noted the unmistakable restraint for the US Dollar despite this confidence. So, is the currency just waiting for the official word or is the ‘buy the rumor’ phase simply very tepid? With EURUSD so close to 1.1500 support, it may be better to remain incredulous.

Chart of EURUSD with 50-Day SMA and ROC (Daily)

Chart Created on Tradingview Platform

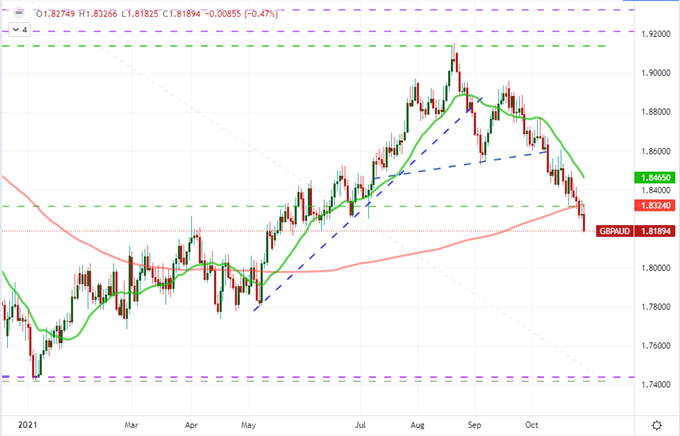

While Wednesday’s FOMC decision is top billing for the global markets, it isn’t the only central bank on tap – and not the only group that faces heavy speculation around its intent. Earlier in the week (Tuesday morning Asia session), the Reserve Bank of Australia is set to announce its policy views. No change in the benchmark rate is expected, but a surge in the short-term government bond yields suggests there has been a dramatically hawkish shift in just the past few weeks. That will likely mean a rate hike earlier than previously expected (now mid-2023 is the hawkish view) and an end to stimulus in the opening quarter of next year; but perhaps the yield curve control effort will be dropped to allow flexibility against inflation. Meanwhile, the Bank of England’s (BOE) decision and monetary policy report released during Thursday’s London session is expected to bring a hawkish timeline of its own. Swaps have moved the anticipated start of hikes sharply forward these past weeks such that debate has even shifted to a possible December move. GBPAUD, GBPUSD and AUDUSD are capable of great volatility but are fraught when it comes to setting out probabilities of a clear course; so chose counterparts wisely.

Chart of GBPAUD with 20 and 200-Day SMAs (Daily)

Chart Created on Tradingview Platform