S&P 500, CPI, Dollar, EURUSD and NZDCAD Talking Points:

- The Dollar’s post-CPI rally was cut short by otherwise rote remarks by Fed Chairman Powell…the same type of comments fostering Fitch’s downgrade warnings

- Monetary policy is a more global consideration for those overly confident of the S&P 500’s persistent charge as global central banks are backing away from stimulus

- Top event risk ahead revolves around event risk like Chinese GDP and US earnings, but my attention will hold to the critical risk-influence of stimulus

Central Banks Are Trying to Back Out of a Critical Support Role Without Causing a Structural Collapse

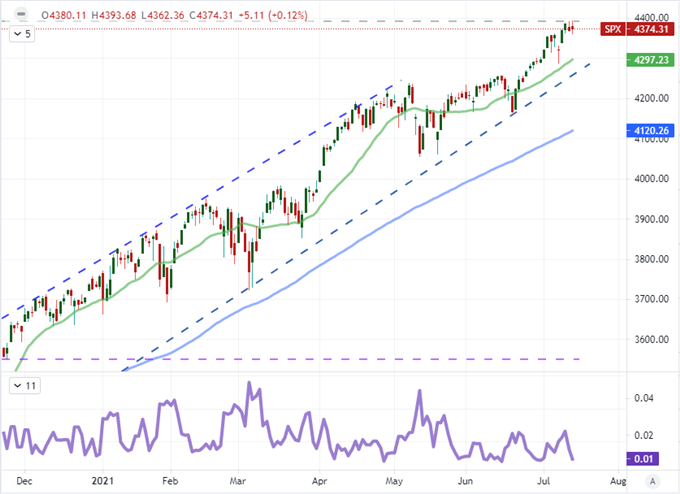

Monetary policy is the systemic theme most ominous on my radar and the most as-risk markets are the lead speculative benchmarks like the US indices. While traders and the headlines may have gotten wrapped up in specific changes in language from specific updates – like Fed Chairman Powell’s hymn-like reassurance that inflation is transitory – their was a significant shift away from persistent, extreme accommodation this past session. Speculative comfort in the markets now is built upon years of exceptional support issued by central banks the year over; so while the markets may be discounting the risk of pulling back the punchbowl, any introspective recognition of this dependency could prove an overwhelming collapse for exaggerated risk benchmarks. In practical terms, we seem either destined to maintain a measured pace of climb or face an expediated tumble for the likes of the S&P 500. Choose your strategy accordingly.

Chart of the S&P 500 with 20 and 100-Day Moving Avgs and 3-Day Range (Daily)

Chart Created on Tradingview Platform

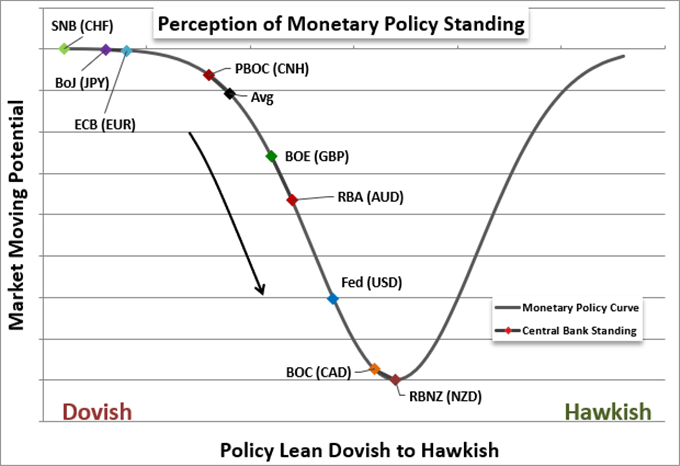

While it is easy to get caught up in the sharp response of relative monetary policy bearings through pairs like EURUSD or NZDCAD, the systemic sway of a shift in global monetary policy can be an overlooked threat until it is too late. If we look back over the past few months of central bank policy decisions, forecasts and member statements; there has been a tangible shift away from the bottomless accommodative stance taken in the immediate aftermath of the pandemic. Both the Bank of Canada and Reserve Bank of New Zealand have tapered, the Reserve Bank of Australia and Bank of England have emanated some commentary to suggest a reduction in asset purchases is not far out, and the Federal Reserve’s interest rate forecast is projecting a first hike perhaps before the end of 2022. While these may not register a global run of rate hikes, they are a critical reversal in the tools most heavily used over the past years of monetary policy. The capital markets obviously seem capable of overlooking this risk for now, but recognition is inevitable depending on circumstances. If fear can gain a foothold before liquidity recovers after the summer doldrums, beware.

Chart of Relative Monetary Policy Standing of Major Central Banks

Chart Created by John Kicklighter

Apparently, Boilerplate Assurances Can Still Override Data

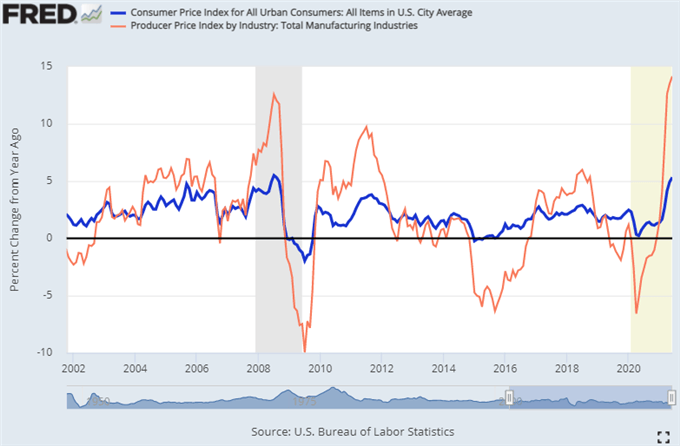

The US CPI (consumer price index) update on Tuesday was a strong market mover for the likes of the US Dollar, Treasury yields, junk bonds and Fed Funds futures. The implications of a higher probability rate hike before the end of 2022 took its toll on these sensitive markets, but the inevitability of normalization didn’t seem to truly take traction according to the technical response of the broader financial system. Risk aversion, despite its sensitivity, didn’t collapse; so the probability of another complacent bounce was high. We found that recovery this past session despite further reinforcement from inflation data. The Producer Price Index (PPI) for June hit a modern calculation series high of 7.3 percent. That suggests an imminent reversal in consumer costs is unlikely and action from the Fed to curb its contribution to excesses is more pressing. Yet, the hawkish data didn’t seem to gain serious traction. That was likely a save by Fed Chairman Jerome Powell who was testifying to the House of Representatives on the economy. He repeated his transitory inflation chant and the markets seem to accept the succor. That said, his remarks seemed to confuse an aim for transparency on the timing of taper without having a clear model to base that timetable. I’ll point out that credit rating agency Fitch remarked in its US evaluation that the risk of a downgrade in its AAA-status could result from “a decline in the coherence and credibility of US policymaking…”

Chart of US CPI and PPI Year-Over-Year Change (Monthly)

Chart of from FRED Fed Economic Database with Data from BLS

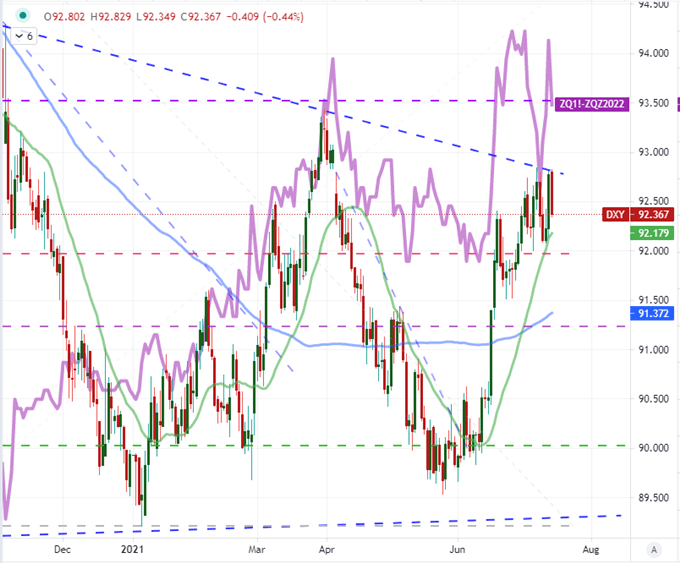

While I believe the Fed’s mantra sounds more and more hopeful rather than prescriptive, the markets seem nevertheless soothed by the assurances. Interest rate forecasts measured by Fed Fund futures cut projections of total rate hikes through the end of 2022 from 23.5 basis points Tuesday to 20 basis points through Wednesday. In practical terms, that is reducing the probability of a standard 25bp rate hike by December 2022 from a 94 percent to 80 percent probability. Even though the first stage of monetary policy change will be via a taper rather than interest rates, the Dollar clearly responded to the shift in mood with the DXY Dollar Index suffering its biggest single-day drop in three trading weeks. That makes for a well-timed and technically-precise range reversal.

Chart of DXY Dollar Index with 20 and 100-DMAs, Implied Fed Rate Hike Through 2022 (Daily)

Chart Created on Tradingview Platform

The Majors to Watch Ahead: EURUSD, GBPUSD, NZDCAD and a Begrudging USDCNH

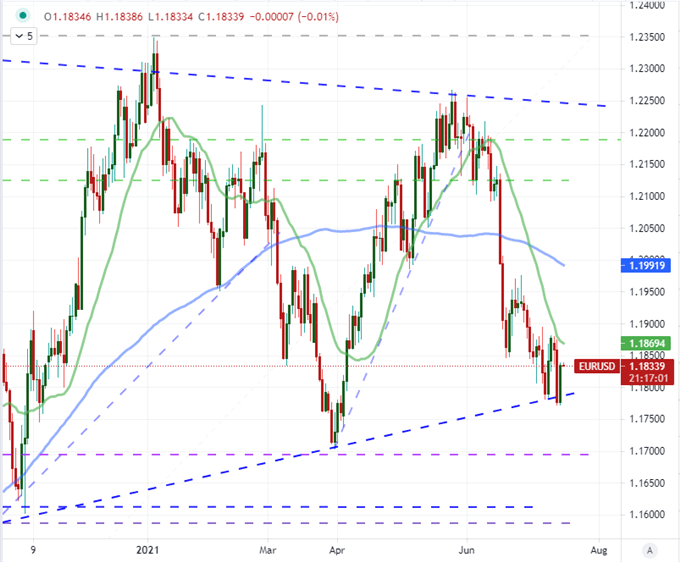

With the Dollar’s quick turn from its failed breakout attempt, EURUSD would naturally reflect its own range reversal. The pair was attempting to clear 1.1800 support and clear a 12-month wedge, but the ability to override market restraint didn’t prove fruitful. Trading back into established ranges is more aligned to the market conditions we are currently facing versus charging a break with follow through. I am keeping a weathered eye on speculation around US policy intent and the Greenback’s responsiveness; but Powell day two, import/export inflation and initial jobless claims are likely to struggle to urge the same kind of market response as CPI or Powell day one.

| Change in | Longs | Shorts | OI |

| Daily | -1% | -4% | -3% |

| Weekly | 4% | -10% | -5% |

Chart of the EURUSD with 20 and 100-Day Moving Averages (Daily)

Chart Created on Tradingview Platform

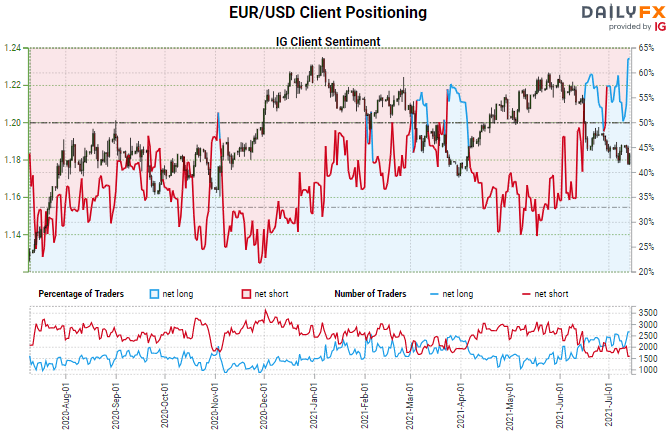

Speaking of comfort with ranges, retail traders naturally prefer such technical formations because the boundaries are easier to identify and the implications of a quick swing better the shorter-term time frames of the average person in this category. As it happens, the retail crowd at IG leaned aggressively against a bearish EURUSD break this past session. In fact, the IGCS positioning reading showed nearly 64 percent of the traders in the measure were long – the highest reading in well over a year. Retail traders often fall victim to cognitive biases or inexperience; but in range markets, their preferences can actually align to prevailing winds.

Chart of EURUSD with Speculative Positioning from IG (Daily)

Chart from DailyFX with Data from IG

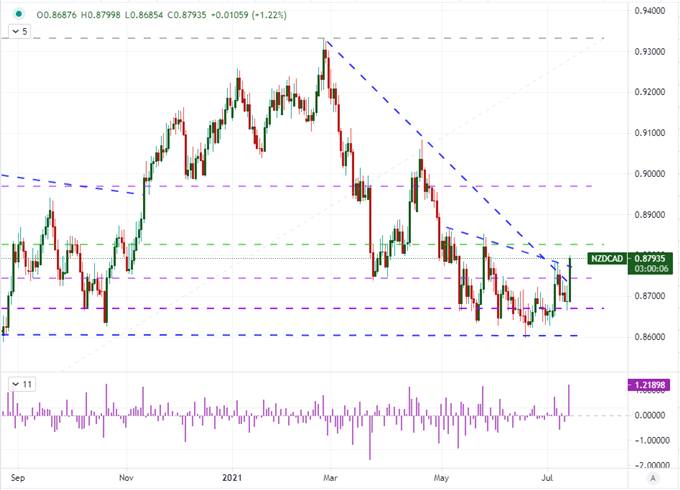

Outside of the generic watch-and-wait around US monetary policy, there are a range of fundamental factors that are more calendar based over the coming 24 hours. US earnings will span further beyond the banking sector Thursday with Alcoa and TSM accompanying Morgan Stanley with their quarterly numbers. The British Pound which enjoyed a rally this past session on heated UK inflation stats and BOE member rhetoric this past session will find employment data to back up the heightened interest. Chinese GDP and June economic statistics are arguably top listing, but the market moving capacity of the data is historically limited as the surprise quotient is notoriously low. However, amid all of this, I will be watching a pair like NZDCAD as the ability to render more from a shift in monetary policy – more precise here – can define the systemic view of risk trends.

Chart of the NZDCAD with 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

.