Talking Points:

- Risk trends leveled off from the progressive risk aversion earlier in the week, but the fundamental pressure hasn't diminished

- The US-China standoff still hangs on President Trump's $200 bln threat, meanwhile the EU will start 2.8bln in tariffs Friday

- Leaders of the Fed, ECB, BoJ and RBA weighed in on monetary policy Wednesday; the BoE and Carney will take over Thursday

See how retail traders are positioning in EUR/USD, other key Dollar pairs and global equity indices as monetary policy adds to concern already stoked by trade wars. Find speculative positioning on the DailyFX sentiment page.

That Familiar, Uneasy Calm

A calm in the global markets nowadays draws more anxiety that it does relief. In contrast to the convenience of unquestioned complacency of the past, market participants nowadays are far more aware of the discrepancy between stability and the growing drum beat of global trade wars. Merely holding course on an already overindulgent speculative exposure is a costly endeavor against the threat of volatility and illiquidity moving forward. Nevertheless, the retreat in speculative markets cooled Wednesday with US equity indices exhibiting that familiar return to undeserved balance. For the S&P 500, the session was an 'inside day' arresting the progress of its otherwise inconsistent slide. The tech-focused Nasdaq would reach for a 'technical' record high close with the favorite-FAANG group gapping to its own historical high water mark. In contrast, the Dow managed its first gap higher on an open in four trading days but it nevertheless notched a 7th consecutive decline - still the worst run for the market since March 28, 2017. Looking to other global risk assets with a particular trade war orientation, the Shanghai Composite edged higher after its painful tumble this past week while the Emerging Market ETF (EEM) did the same. Neither move is particularly convincing.

Trade Wars Have Not Been Resolved

It is important that we don't read this past session's move to stabilize as evidence that trade wars have in turn been resolved. Quite the opposite, the situation for international trade has actually worsened through the past session. For the engagement for the United States and China we are still hanging on the latest threat of escalation by the US President Donald Trump. He vowed to raise the tax tab against China astronomically by $200 billion in response to the country implementing in-kind tariffs of its own on US products as a retaliatory move. There is a fundamental disconnect on where this situation 'started' and clearly a willingness to move the stakes higher rather than to meet low risk compromise. It would be dangerous to approach the markets with belief that 'cooler heads will prevail'. Meanwhile, we were reminded that this is not just a one-front trade war with news the European Union that it would start 2.8 billion in tariffs on certain US products in its response to the US metals duties announced at the end of May. It is not unreasonable to worry that the US could escalate the situation on this line as well. If that happens, the situation will be materially worse for global growth and financial stability.

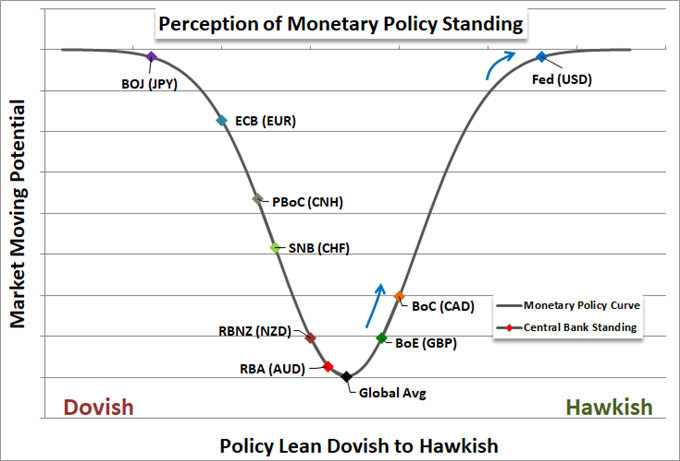

Monetary Policy is Still a Critical Theme

It is easy to get lost in the uncertainty and provocations of trade wars, yet this is not the only critical fundamental theme that investors must keep a vigilance on. Monetary policy is still a crucial pillar for speculative appetite (and lesser source of growth). Long after the financial crisis had passed and even after its effectiveness for building economic growth and inflation, the world's largest central banks continued to pump stimulus into the system hoping for trickle-down confidence via the wealth effect. Hitting the viable limitation of the banks' collective options, officials and markets have recognized the end. Yet, the full implications for either their exit or a test of economic/financial trouble on firefighters out of water hasn't prompted full speculative rebalance. Wednesday, the final day of the ECB hosted central bank policy summit in Sintra, Portugal saw the heads of the Federal Reserve, European Central Bank, Bank of Japan and Reserve Bank of Australia speak on a panel. The all voiced direct concern of trade wars, but the policy views were as disparate as we have come to evaluate. The ECB's Draghi reiterated his group's dovish - but limited - intentions moving forward. The Fed's Powell on the other hand, kept the hawkish rhetoric in place; but offered a crack of doubt by suggesting the neutral rate may be only 100 basis points higher and a material worsening of trade policy could alter the Fed's course.

BoE Decision and Carney Ahead; Kiwi, SNB and Oil Worthy of Attention

There is a lot of event risk due over the next 48 hours. A run of PMI data will give a global economic update and the start of the EU tariffs are broad. Yet, a more concentrated event risk over the next session comes for the Pound. The Sterling this past session held steady despite the compromise reached between the UK government and Parliament on the progress of the EU Brexit bill. Now, we have to evaluate monetary policy. The BoE rate decision is on tap and there is very little chance of a move at this gathering. That said, the expectation of a hike before the end of the year is still very high. The group's statement or Governor Carney's remarks later at the Mansion House speech can set speculation moving forward - and the latter event could also revive concerns over Brexit. Far less anticipation is set in the SNB rate decision also due Thursday. The group has lost credibility and interest in changing policy, but we shouldn't write it off. The New Zealand Dollar has been greased by the broad trade (current account) and GDP figures for 1Q, we'll see if that can make a technical move for NZD/USD. Oil is also carving out some technical opportunity as fundamental anticipation heats up into the OPEC meeting. We discuss all of this and more in today's Trading Video.

If you want to download my Manic-Crisis calendar, you can find the updated file here.