Talking Points:

- Day 2 of Janet Yellen's testimony yielded no clearer a path to the future nor a resolution for the Dollar at major support

- Risk assets including equities and emerging markets advanced, but the Aussie and Kiwi Dollars led for intensity

- Top event risk includes US CPI, US consumer sentiment and bank earnings; but themes and market conditions matter more

Dollar is threatening a break of the midpoint to its three decade range while the S&P 500 is luring in bulls with close proximity to fresh record highs. Download our 3Q forecasts to see what the DailyFX analysts expect from these markets over the next 3 months.

The Dollar and US equity indexes seem so close to marking critical - and opposing - technical breaks, but the breakout with conviction seems to constantly elude anxious traders. Where does this curb on speculative ambition truly originate? Are the technical levels simply too robust? Have event risk and themes prompted more skepticism than enthusiasm? Or, perhaps investors are simply wary of their already-exceptional exposure and are no longer willing to add overly-expensive assets to their portfolios. Given the dynamic between these three very different analysis techniques, it is more likely that conditional factors are dictating which fundamentals matter and what technical patterns can achieve. With that hierarchy of influence, the technical charge behind benchmarks like the DXY Dollar Index and S&P 500 looks somewhat dubious.

This past session, Fed Chairwoman Janet Yellen participated in her second day of testimony before Congress. Her remarks did further shape the outlook for the economy, financial system and monetary policy; but that did not translate into meaningful traction for the Greenback. It is true that the Chair is careful with what she says to avoid generating volatility in the markets, but the theme itself has significantly shifted in terms of influence. The Fed's hawkish 'advantage' over its counterparts doesn't afford leveraged premium anymore as others start to follow suit. Instead, US policy is a baseline for the global shift away from extreme accommodation. That holds deeper implication for sentiment across the globe; but such a deep current is more difficult to divert. That is perhaps where much of the reticence for the S&P 500, other global equity indexes and risk-leaning assets arises. In turn, expectations for a break from the S&P 500 above 2,440 or the DXY below 95.50 should be judged by the strength of the ignition and/or the restrictions on run.

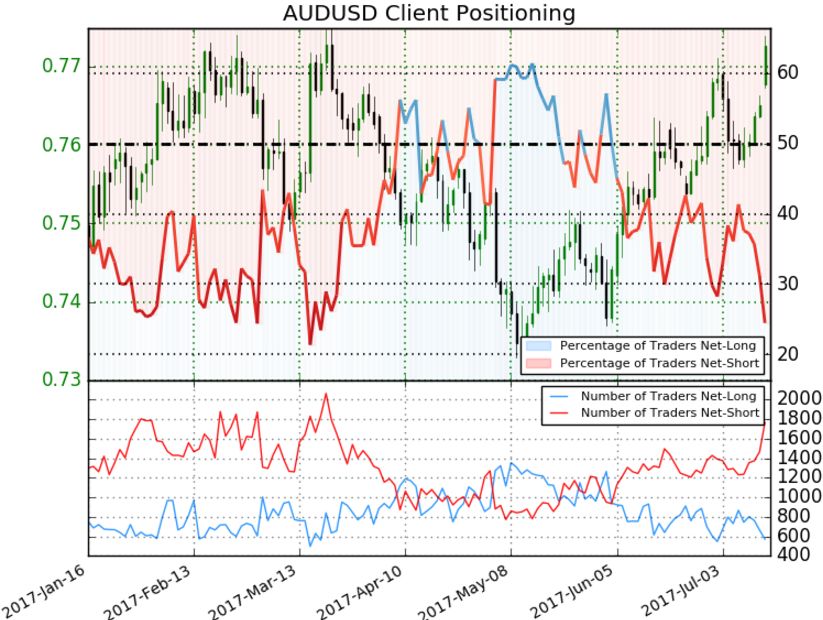

For top event risk, the US docket is carrying a significant round of event risk that can span interest in politics spill over, monetary policy and financial stretch. The UofM Consumer Confidence report is generally treated as a simple economic indicator, but its value comes in its relationship to the environment. Over the past 8 months, significant lift has been found through confidence of business and economic-friendly policies being fast tracked through the political system; yet little-if-any progress has been found. How long can this positive wind from a critical global force (the US consumer) last on anticipation. The US CPI is a critical inflation measure still, but the leverage a pick up or slide in rate expectations affords the Dollar has clearly dropped. In bank earnings (Citi, JPMorgan and Wells Fargo), we will see measure of the 'rich valuations' now showing up even in Fed member language; but don't expect explicit bombshells. In contrast, the Australian and New Zealand Dollars have proven exceptional movers with little high profile motivation. Does this high intensity compensate for a lack of motivation with various technical breaks from pairs like AUD/USD, AUD/JPY and NZD/CAD? We discuss trading opportunities and market conditions in today's Trading Video.

To receive John’s analysis directly via email, please SIGN UP HERE