NASDAQ 100, HANG SENG INDEX, ASX 200 WEEKLY OUTLOOK:

- Dow Jones, S&P 500 and Nasdaq 100 indices closed +0.80%, +1.17% and +2.14% respectively

- Investors shrugged off Russia-Ukraine tensions amid stabilizing commodity prices, paving the way for an extended rally in global equities

- China reported lower new Covid-19 cases on Sunday, alleviating pressure on its stock market

Global Stock Rebound, Ukraine, Hang Seng Index - Asia-Pacific Week-Ahead:

The Nasdaq 100 index extended a four-day rally on Friday as investors shrugged off Russia-Ukraine tensions amid stabilizing commodity prices. A majority of S&P 500 sectors closed higher, with the technology sector outperforming. As the Fed painted a clearer picture about its monetary policy at the FOMC meeting last week, investors may have returned to the market for bargain hunting after weeks of selling. Looking ahead, there may be more risk-on priceaction down the road amid a relatively quiet event calendar this week. Japanese markets are shut for a holiday on Monday.

US president Joe Biden and Chinese leader Xi Jinping had a call on Friday, in which they exchanged views on US-China relations, the Ukraine situation and other issues of mutual interest. The call ended with no concrete outcomes however, as Biden’s outreach seemingly failed to prod Xi to commit to leveraging Chinese influence to end Russia’s invasion of Ukraine, at least for now.

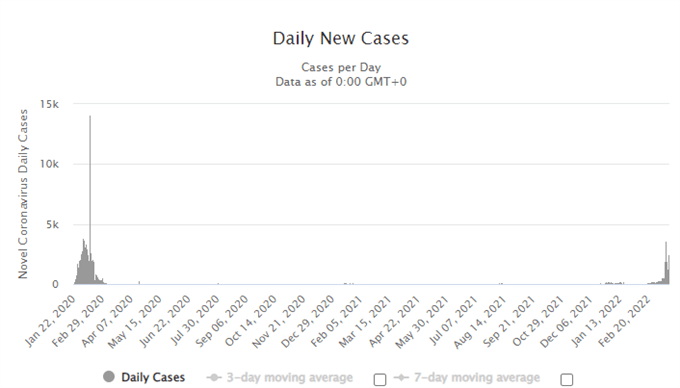

In China, new Covid-19 cases have fallen to 1,737 on Saturday from 2,228 a day ago. The Jilin province alone reported 1,191 cases. Falling new cases underscored the country’s prompt and stringent measures, including lockdowns and mass tests, in containing the rapid spread of the virus. This may help to boost investor confidence amid the country’s most severe viral outbreak since 2020. In Hong Kong, new Covid-19 cases have declined to 14,149 on Sunday from 16,597 a day ago. Falling cases suggest that the worst of the pandemic wave may be behind us, and the city’s policymakers may start to review its Covid-19 restrictions soon.

Daily New Cases in China

Source: worldometers

APAC markets look set to kick off the week on the front foot following a positive lead on Wall Street. Futures in Japan, mainland China, Australia, Hong Kong, South Korea, Taiwan, Singapore, India and Indonesia are in the green, whereas those in Malaysia and Thailand are in the red.

Chinese tech giants listed on US exchanges rallied on Friday, setting a positive tone for their HK counterparts. Tencent (+6.42%), Alibaba (+7.90%), NIO (+10.84%) and JD.COM (+5.15%) were among the top gainers. Last week, high-level Chinese officials made an unusual announcement to shore up the stock markets after shares listed in Hong Kong plunged to their five-year lows. This may mark a “policy bottom” for both mainland and Hong Kong shares as authorities’ attitude towards platform companies appears to “U-turn”.

For the week ahead, UK inflation datadominates the economic docket alongsideUS durable goods orders and Markit manufacturing PMI readings. Find out more from the DailyFX calendar.

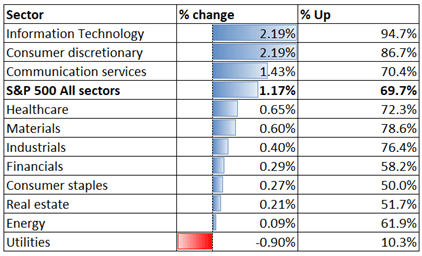

Looking back to Friday’s close, 10 out of 11 S&P 500 sectors ended higher, with 69.7% of the index’s constituents closing in the green. Consumer discretionary (+2.19%) and information technology (+2.19%) were among the worst performers, whereas utilities (-0.90%) and energy (+0.09%) trailed behind.

S&P 500 Sector Performance 18-03-2022

Source: Bloomberg, DailyFX

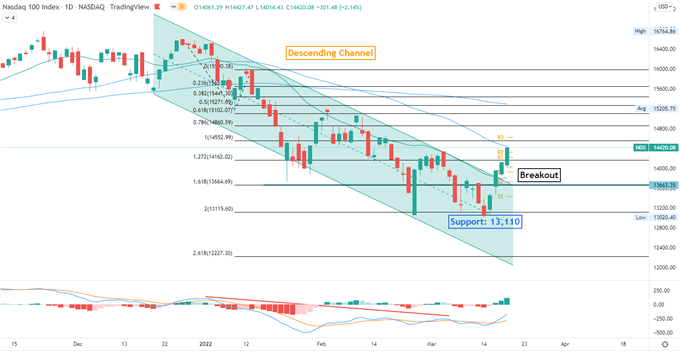

Nasdaq 100 Index Technical Analysis

The Nasdaq 100 index breached above the ceiling of a “Descending Channel” as highlighted on the chart below, opening the door for further upside potential. An immediate resistance level can be found at 14,550 – the 100% Fibonacci extension. The MACD indicator formed a bullish crossover and trended higher, suggesting that near-term buying pressure may be dominating.

Nasdaq 100Index – Daily Chart

Chart created with TradingView

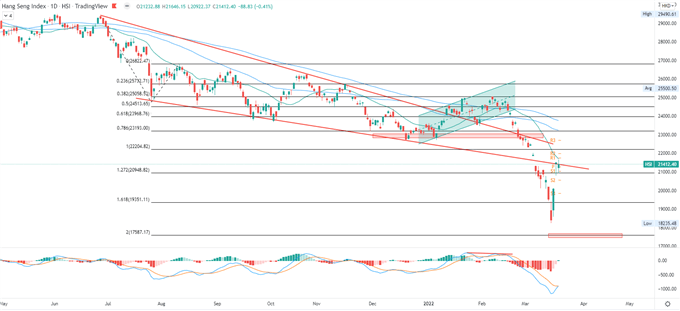

Hang Seng Index Technical Analysis:

The HSI rebounded sharply last week, underpinning strong upward momentum in the near term. Prices are testing the 21,420 trendline resistance, breaching which may intensify buying pressure and expose the next resistance level of 22,200. The MACD indicator formed a bullish crossover, suggesting that buying pressure may be building.

Hang Seng Index – Daily Chart

Chart created with TradingView

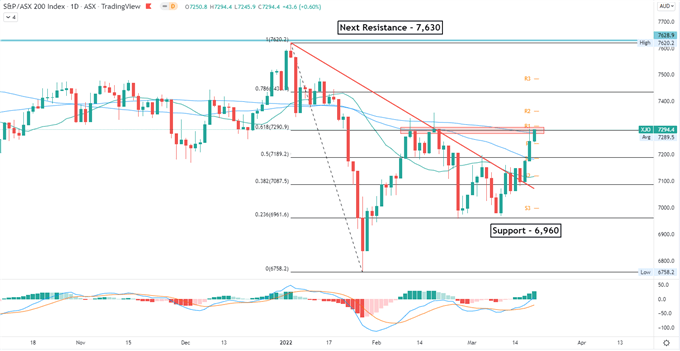

ASX 200 Index Technical Analysis:

The ASX 200 index breached above a trendline support as shown on the chart below. Prices are hitting an immediate resistance level at 7,290, breaching which may open the door for further upside potential with an eye on 7,435. The MACD indicator is trending higher, underscoring upward momentum.

ASX 200 Index – Daily Chart

Chart created with TradingView

--- Written by Margaret Yang, Strategist for DailyFX.com

To contact Margaret, use the Comments section below or @margaretyjy on Twitter