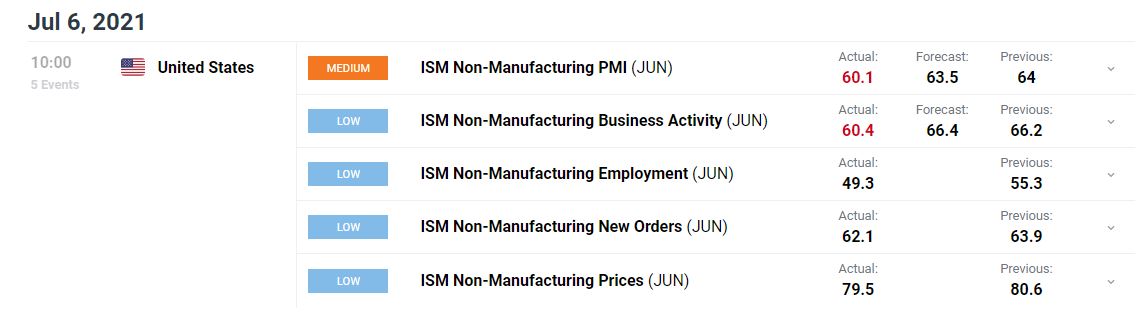

KEY POINTS ISM SERVICES:

- June ISM services drops to 60.1 from a record high of 64, but manages to grow for the 13th consecutive month

- Despite the deceleration, the data remains strong and suggests economic recovery is on course, although at a slower pace

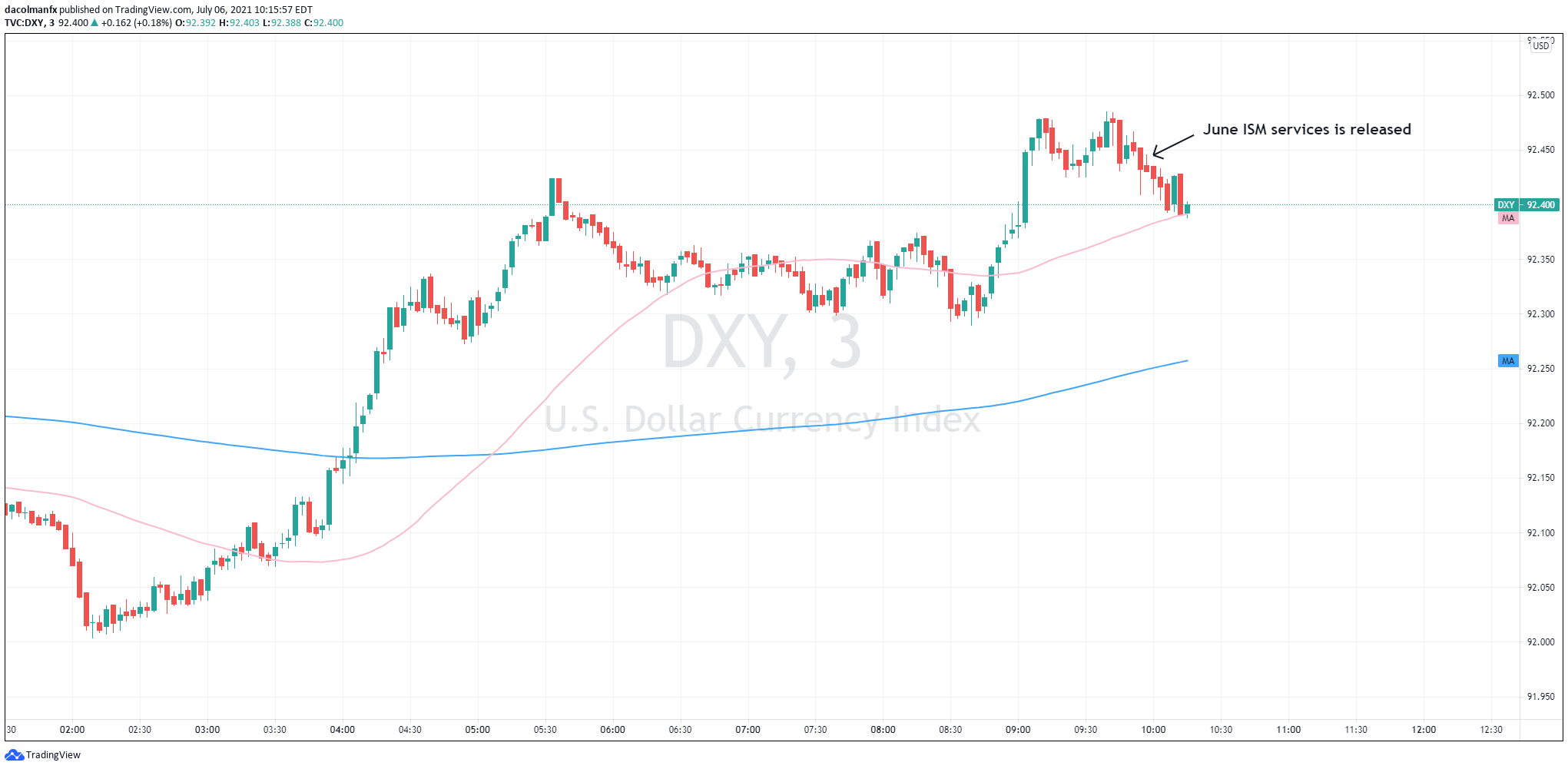

- U.S. dollar ticks lower after the ISM report, although the reaction is very moderate

Most read: Why Most Traders Fail and How to Increase Trading Success

The services segment slowed, but still grew at a strong pace last month, supported by robust demand as the economy moved toward full reopening thanks to fewer or almost no pandemic-related restrictions across the country. According to the Institute for Supply Management, the June services PMI declined to 60.1 from May's record high of 64.00, below forecasts of 63.4. Although the data disappointed expectations, the sector in which most Americans work managed to expand at a healthy pace for the 13th consecutive month, a sign that the recovery is on course, albeit less dynamic. As a reminder, any print above 50 indicates an expansion in activity, while readings below that mark signal a contraction.

The table below summarizes key results from the ISM survey:

Source: DailyFX economic calendar

Given that the service sector accounts for roughly 70% of GDP and the bulk of U.S. jobs, it can provide clues about the overall health and direction of the economy. However, the lack of market reaction in the US dollar (DXY) suggests that the data may have slightly less relevance this time around, as it was released just after the June nonfarm payrolls report.

DXY CHART (3 MINUTES)

Last Friday ahead of the long weekend, the Labor Department released its latest employment survey. According to the agency, the U.S. economy created 850,000 jobs in the previous month, moderately above the Wall Street consensus. Though hiring accelerated at the fastest pace since March, the unemployment rate rose to 5.9% from 5.8%, a clear indication of persistent slack in the labor market. This mixed-bag report failed to convince investors that the economy has made sufficient progress to satisfy the Fed's criteria for reducing asset purchases. Today's ISM data appears to validate the theory the US economy needs to advance further before monetary policy normalization.

In any case, to better understand the central bank's current stance, it would be important to watch the Minutes of the June FOMC meeting to be released tomorrow afternoon. The document could shed some light on the Fed's internal discussions and give a more detailed view on the preliminary QE tapering debate.

If the Fed minutes suggest that the institution is moving much closer to tightening monetary policy, it would not be surprising to see a moderate rise in the dollar. On the other hand, if the institution is perceived as dovish and hesitant to begin normalizing policy despite mounting inflationary pressures, the dollar could weaken further in the near term.

EDUCATION TOOLS FOR TRADERS

- Are you just getting started? Download our beginners’ guide for FX traders

- Would you like to know more about your trading personality? Take our quiz and find out

- IG's client positioning data provides valuable information on market sentiment. Get your free guide on how to use this powerful trading indicator here.

- Subscribe to the DailyFX Newsletter for weekly market updates and insightful analysis

---Written by Diego Colman, DailyFX Market Strategist

Follow me on Twitter: @DColmanFX