NASDAQ 100, HANG SENG, ASX 200 INDEX OUTLOOK:

- Dow Jones, S&P 500 and Nasdaq 100 closed -0.26%, +0.36 and +1.51% respectively

- President Joe Biden proposed a $2 trillion infrastructure spending plan, which is smaller than markets had anticipated

- Hang Seng and ASX 200 indices traded mildly higher amid tech rebound

Infrastructure Plan, US Data, Tech Rebound, Asia-Pacific at Open:

The Nasdaq 100 index rallied 1.51% after President Joe Biden announced a smaller-than-expected infrastructure spending proposal. The $2 trillion stimulus plan aims to revamp roads and bridges, create millions of jobs and address climate changes. The size of the package came below markets’ earlier forecast of $3-4 trillion, resulting in some profit-taking activity among the reflation-centric sectors such as energy, real estate and materials. The infrastructure bill will be partially funded by higher corporate tax as the President intends to raise it to 28% from current 21%.

The heavily watched US 10-year Treasury yield closed at a 14-month high at 1.746% as traders continued to price in a reflation outlook in the bond market. Rising longer-term rates may exert downward pressure on non-yielding precious metals and risk assets in general, as risk-free rates (discounting rates) rise.

A handful of overnight economic data was encouraging, with UK Q4 GDP contracting less than expected. Germany unemployment change fell by -8k vs. -3k forecast. US ADP private payrolls added 517k jobs in March, the most seen since September 2020. Although the figure came slightly below the baseline forecast of 550k, it marked a strong rebound from February’s reading and showed a decent jump in hiring activity.

US ADP Private Payroll Report - March 2021

Source: Bloomberg, DailyFX

A strong rebound in the tech sector overnight may boost sentiment in Asia-Pacific markets, with futures across Japan, Hong Kong, Taiwan, Singapore and India pointing to trade higher. Australia’s ASX 200 index opened marginally higher, led by information technology (+1.07%), materials (+1.05%) and communication services (+0.65%) sectors, whereas real estate (-0.89%), industrials (-0.65%) and consumer staples (-0.41%) trailed behind.

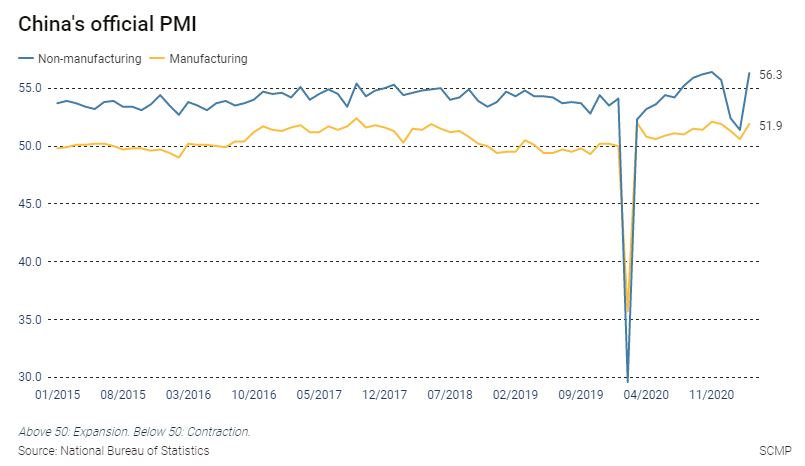

Hong Kong’s Hang Seng Index (HSI) closed 0.70% lower on Wednesday despite much stronger-than-expected China NBS PMI readings. China NBS Manufacturing PMI came in at 51.9 vs. 51.0 forecast, and non-manufacturing PMI surged to 56.3 from 51.4 a month ago. The manufacturing industry rebounded strongly after the Lunar New Year as recovery of production accelerated. Growth in the service and construction sectors appeared to have gained momentum as sporadic local outbreaks of Covid-19 were largely put under control in March.

Source: SCMP

Looking ahead, US weekly initial jobless claims data headlines the economic docket alongside US Markit and ISM manufacturing PMI readings. Friday’s US nonfarm payrolls data will be closely monitored by traders around the world for clues about the recovery of US labor market. Find out more from the DailyFX calendar.

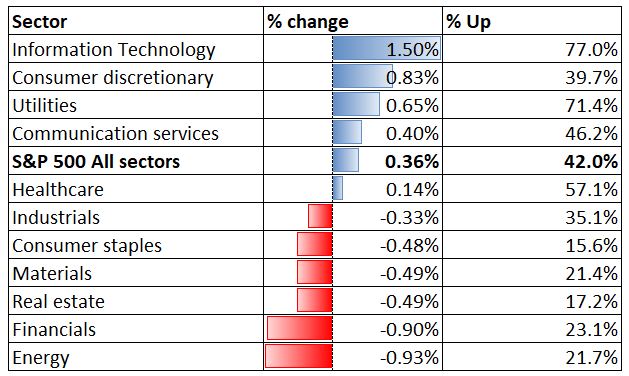

Looking back to Wednesday’s close, 5 out of 11 S&P 500 sectors ended higher, with 42.0% of the index’s constituents closing in the green. Information technology (+1.50%), consumer discretionary (+0.83%) and utilities (+0.65%) were among the best performers, while energy (-0.93%) and financials (-0.90%) trailed behind.

S&P 500 Sector Performance 31-03-2021

Source: Bloomberg, DailyFX

Nasdaq 100 Index Technical Analysis

The Nasdaq 100 index pierced above the 20- and 50-day SMA lines and is now facing an immediate resistance level at the 100-day SMA (13,170). Breaking above this line may intensify the near-term buying pressure and expose the next resistance level of 13,257 ( the 61.8% Fibonacci retracement). An inverse “Head and Shoulders” pattern has likely formed on its daily chart, although some more consolidation at the right “shoulder” was observed. The MACD indicator is trending up after the formation of a bullish crossover, suggesting that buying power is building up.

Nasdaq 100 Index – Daily Chart

Hang Seng Index Technical Analysis:

The Hang Seng Index (HSI) is trending lower within the “Descending Channel” as highlighted in the chart below. The index is challenging the ceiling of the channel with an attempt to break out. A successful attempt may open the door for upside potential with an eye on 28,900 for immediate resistance. A failed attempt however, may lead to a deeper pullback towards 27,930. The MACD indicator is trending lower beneath the neutral midpoint, underscoring downward momentum.

Hang Seng Index – Daily Chart

Chart by TradingView

ASX 200 Index Technical Analysis:

The ASX 200 index appears to have entered a range-bound condition between 6,660 and 6,860 since early March, waiting for fresh catalyst for a clearer direction. The MACD indicator is oscillating around the neutral midpoint, giving little signal in terms of momentum.

ASX 200 Index – Daily Chart

--- Written by Margaret Yang, Strategist for DailyFX.com

To contact Margaret, use the Comments section below or @margaretyjy on Twitter