Talking Points:

- Global equity markets continue to face aggressive selling; and China remains closed for the rest of the week. The bear flags we mentioned last week have been soundly broken, and as long as price action remains below those flagging-formations, the trend is bearish.

- Yields on Japanese Government Bonds moved into negative territory into the overnight, highlighting the possibility for a Bund-like move in JGB’s as investors direct safe-haven flows into Japanese Government Bonds.

- There are growing choruses for a move to negative rates from the United States, but this may bring some nasty repercussions for retirees and pensioners. Japan’s already begun to feel the impact of this, and this is a problem that isn’t going to go away until it’s addressed by Central Banks.

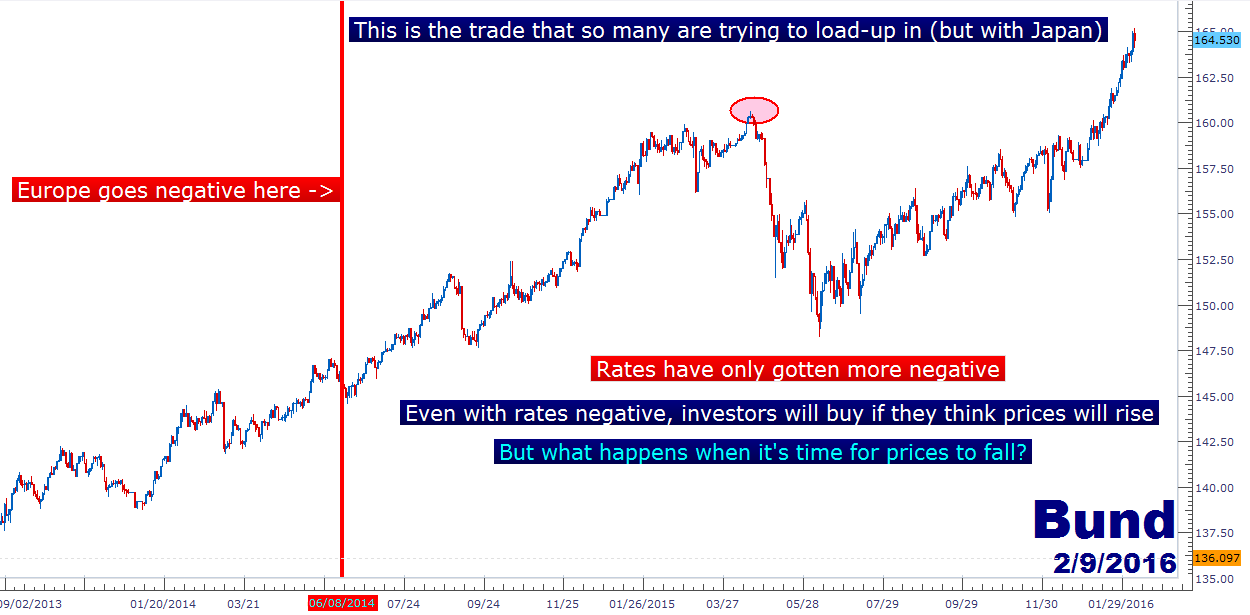

It was just over a week ago that hope enveloped Financial Markets after the Nikkei ran up by 3% on the back of the surprise announcement of negative rates from the Bank of Japan. As we had mentioned at the time, the concept of negative rates is still very experimental, and most of the examples that we have of its usage are in Europe over the last year and a half; so this wouldn’t exactly be a case study that you’d want to classify as ‘massively successful.’ Frankly, Europe is still in a very rough spot, and that negative rate policy was launched with a relatively new QE program. So Europe had both of these working together, and even then, they still had to go for more easing in December by cutting the deposit rate to be even more negative.

But the academic thought was rooted in good intentions: The idea that the Central Bank would charge negative rates to bank deposits appeared as though it may incentivize banks to go out and loan money. After all, if a bank can earn a return (any positive return) by lending the money to regular people, whether to buy a home or start a business, they’re going to earn a considerably more handsome return than if they just kept that locked up at the Central Bank, now earning a negative deposit rate (getting charged money, not earning it).

But this hasn’t happened… These negative rates have only scared banks and investors even more than they already were; and when Europe went negative, many European banks just sent their cash to American or Japanese branches so they can store it at a Central Bank that wasn’t going to charge them money. This creates a massive problem because it’s a clear example of Europe exporting their deflation to other major economies, and these capital flows bring additional strength into these target currencies; thereby making the prospect of recovery even more daunting. Japanese stocks have taken a considerable hit since this announcement and the Yen is seeing rampant strength.

Created with Marketscope/Trading Station II; prepared by James Stanley

So, if capital is leaving Japan – why is the Yen getting stronger?

That’s the thing – this isn’t a direct capital flight thing in the way that many of these Central Banks hoped that it would be. Because capital is coming back into Japan, too; there just aren’t many attractive areas around-the-world to lodge cash in right now. With the BoJ making the move to negative yields, this also drops the floor for bond purchases as part of their QE program. So, if you’re a buyer of Japanese Government Bonds, and the BoJ just told you that they’re buyers all the way to a yield of -.1% (and will likely be holding to maturity), this is like the greatest sense of support that an investor can get. Yes, the yield is negative, and that part is no good. But prices and yields move inversely, so if yields are at .1% right now and you think they’ll move to -.1%, well prices are going to have to rise to make that happen. And not only that, but you will have a Central Bank pushing those prices higher behind your trade!

A clear example of this is Germany, where rates have only gotten more and more negative after the ECB’s move to negative rates in June of 2014. Right now the German 2-year Bund is yielding -.53%. That’s right, it will cost you a little more than a half-a-percent to loan your money to the German government for 2 years. The 5-year Bund is at -.29% and if we go out to 10-years we can get that yield in positive territory at .2%.

But this trade isn’t about the yield. It’s about the price. On the chart below, we’re looking at the performance in the Bund since the announcement of negative rates in Europe:

Created with Marketscope/Trading Station II; prepared by James Stanley

In a market full of fear with few investment options looking attractive, and a market in which banks are appearing reticent to loan out the funds that have been driven into the financial system via Quantitative Easing, the long-bond trade can seem pretty attractive, even with an abysmal yield.

So, while some banks may be sending cash outside of Japan to avoid the BoJ’s negative yields on Central Bank Deposits, it appears that even more flows are coming into Japan to buy JGB’s; at least that’s what the chart of the Yen combined with movements in Japanese government bonds are currently indicating.

This is one of the reasons why we called the Japanese Yen as the safe-haven vehicle of choice back in September of last year; because it was unlikely that we’d see an increase in Japanese QE.

But puzzlingly, we’re already hearing choruses for negative rates in the United States

To put matters in perspective, the S&P 500 is still 14.3% above the high from the Financial Collapse. And it’s 176.2% off the lows in 2009. The same index is down by 10% this year. And we’re already hearing choruses for more action from the Federal Reserve in the form of experimental negative rates. To call this premature would be an understatement, and perhaps further to the point, dangerous for the long-term health of the global economy.

Interest rates have a legitimate purpose in a properly-functioning society; they’re not just for hedge funds and banks to play with. Retirees and pensioners depend on interest payments. Without those interest payments, those pension funds draw down to dangerous and potentially unsustainable levels, and then people begin to get upset because they’ve been promised something for their entire working life that just isn’t there anymore. Just look at what happened in Greece over the last few years where pensioners had their retirement benefits cut to virtual pennies on the dollar. The response here is never pretty, for the people or their governments.

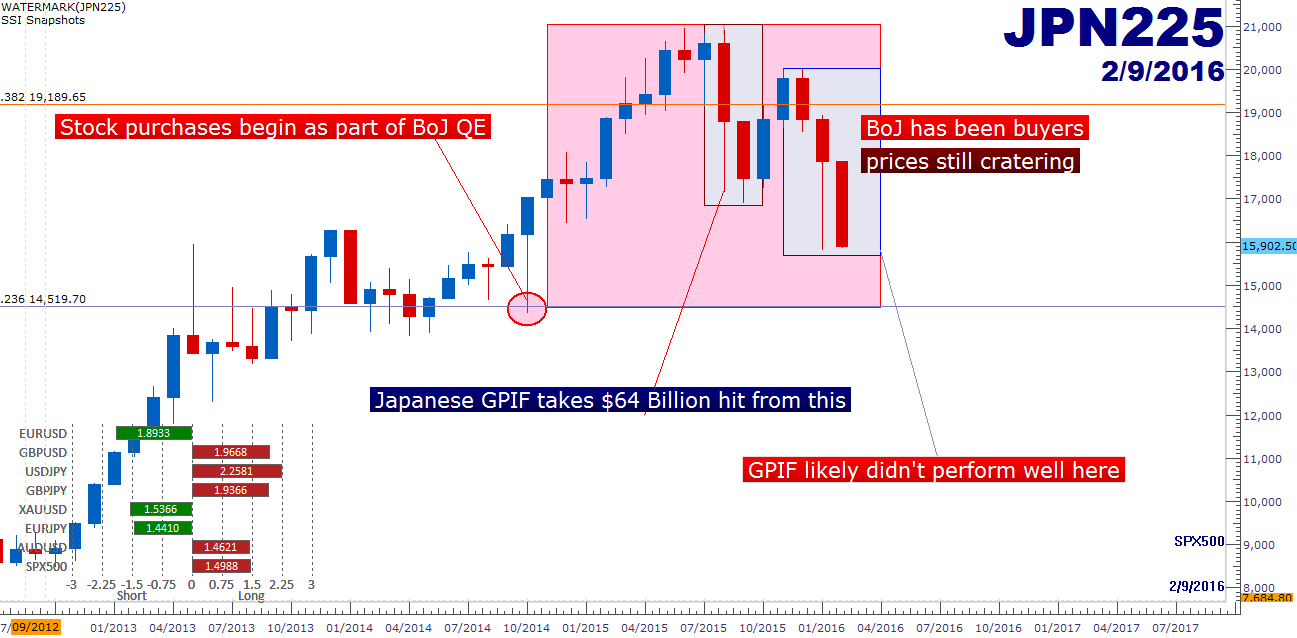

This leads to social unrest and whole other litany of actual problems that politicians don’t want to deal with. So this is why there is such a drive to get the global economy off of ‘emergency-like’ measures and back to ‘normalized’ interest rates, so that the aging populations in Japan and the United States don’t get blind-sided by Social Security or Japan’s GPIF drawing down. Japan’s already taken a hit on this fund; in October of 2014 they started buying Japanese and international stocks (in the form of ETF’s) with their QE program. This seemed like a bad idea at the time, but Japanese stocks had been going up for two years on the back of Abe-nomics, so the idea didn’t seem as glaringly bad as it should have.

After the initial throes of volatility in August and September, the GPIF reported a $64 Billion loss, a drawdown of -5.5%. And this was for a pension fund. Perhaps more disconcerting – if we look at the chart of the Nikkei, notice that we’re fast approaching the level that we were at before the Bank of Japan announced stock purchases (Halloween 2014). So when you look at the below chart, keep in mind that the BoJ has been protecting the bid, and yet the Nikkei is still putting in outsized moves lower. This indicates that some significant selling is going on.

So, just doing more and more QE doesn’t really appear to be a relevant option any longer.

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX