GOLD PRICE OUTLOOK:

- Gold prices unable to capitalize as stocks, US Dollar retrace post-FOMC moves

- Steadily hawkish Fed policy outlook keeping interest rates up, bullion anchored

- Soft US payrolls growth, strong wage inflation may drive gold prices downward

Gold price participation was conspicuously absent this week as worries about the Fed’s hawkish intentions eased across the broader financial markets. Stock markets recovered, with the bellwether S&P 500 index erasing more than half of the drop from January’s high. The US Dollar retreated.

The yellow metal was little-changed in the meanwhile, consolidating in a choppy range near the $1800/oz figure. That keeps it near the middle of the larger sideways centered on the $1750-1850 zone. It has mostly contained price action since mid-2021.

The standstill probably reflects similarly stubborn performance on the rates front. The benchmark 10-year US Treasury yield has echoed gold’s sideways drift, hovering at 2-year highs just below 1.9 percent. The companion breakeven rate – a measure of priced-in inflation expectations – has likewise idled.

Taken together, this has kept real interest rates (nominal rates less expected inflation) relatively stable near the highest levels in 18 months, where they arrived after rising by the most in two years in January thanks to the Fed’s combative rhetoric.

The prospect of still-higher real rates ahead as the US central bank tightens undermines gold’s appeal as an alternative store of value, considering it yields nothing at all. Since this week’s risk appetite recovery did not seem to come with a dovish Fed outlook shift, gold has remained grounded.

GOLD MAY SUFFER ON SOFT US PAYROLLS DATA IF WAGE INFLATION HOLDS UP

The spotlight now turns to January’s US payrolls data. The economy is expected to have added a meager 125k jobs last month. Wage inflation is seen surging to 5.2 percent on-year however, underscoring that sluggish hiring reflects labor shortages rather than weak demand. Job ads are tellingly holding near record highs.

Such a report seems likely to embolden the Fed’s hawks. Indeed, Chair Powell pointedly said that raising rates in the current environment is supportive of the central bank’s inflation and employment goals following last week’s policy meeting. This implies that stabilizing wage expectations is seen as crucial to boost hiring.

Gold is likely to suffer in this scenario as the non-interest-bearing metal falls further out of favor as actual and expected yields advance. The US Dollar is also likely to rebound against such a backdrop, souring demand for the perennial foil to fiat money.

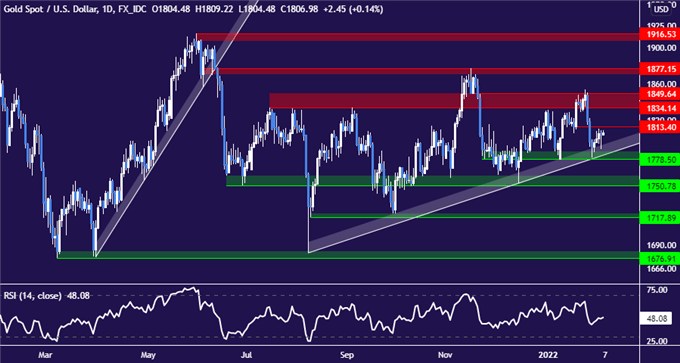

GOLD TECHNICAL ANALYSIS

Gold prices are sitting atop rising trend support guiding them higher since August 2021. Immediate resistance is at 1813.40, with a break above that exposing the 1834.14-49.64 area.November’s swing top at 1877.15 follows thereafter. A daily close below 1778.50 may confirm bearish reversal, targeting 1750.78 next.

Gold price chart created using TradingView

GOLD TRADING RESOURCES

- What is your trading personality? Take our quiz to find out

- See our guide to build confidence in your trading strategy

- Join a free live webinar and have your questions answered

--- Written by Ilya Spivak, Head Strategist, APAC for DailyFX

To contact Ilya, use the comments section below or @IlyaSpivak on Twitter