Central Bank Watch Overview:

- Rates markets continue to get more aggressive with respect to the Fed’s taper and hike cycle – which is good news for the US Dollar.

- Traders are expecting the Fed to raise rates in June 2022, which also coincides with an accelerated pace of tapering asset purchases in the first half of next year.

- Fed rate hike odds are still discounting five rate hikes through the end of 2023, with a 73% chance for six 25-bps rate hikes in total.

FOMC Walks a Fine Line

In this edition of Central Bank Watch, we’ll review comments and speeches made by various Federal Reserve policymakers this month after the communications blackout window around the November Fed meeting ended. While FOMC officials agree that it was necessary to begin tapering asset purchases, it’s clear that markets think more need to be done as US inflation rates have surged to 30-year highs.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Rate Hikes Coming Soon?

The decision to announce a taper to asset purchases at the November Fed meeting was a well-telegraphed, unsurprising development for anyone following commentary in recent months. But even as US inflation rates have soared, Fed policymakers are still peddling the idea that stimulus withdrawal will be a slow, deliberate process, so as to not upset the economic recovery underway. Moreover, policymakers have pushed back against the shifting narrative in rates markets, too.

November 5 – George (Kansas City president) suggests she still sees inflation as a transitory episode, noting “I would not disagree with those who say inflation should back off a bit.”

November 8 – Clarida (Fed Vice Chair) says that the “necessary conditions” to raise the Fed’s main rate will likely have been met before the end of 2022.

Harker (Philadelphia president) notes that he does not believe that rates will rise until the taper is complete.

Evans (Chicago president) comments that he still believes that the rise in inflation is “temporary,” and doesn’t think rate hikes will be warranted until 2023.

November 9 – Daly (San Francisco president) says that the Fed will have a better idea about whether or not inflation’s rise is transitory by “the summer of 2022.”

November 10 – Bullard (St. Louis president) talks up potential hikes in 2022, suggesting “based on where I think we are today I actually have two rate increases penciled in for 2022 ... that could change by the time we get into the first half of next year in either direction really.”

Daly pushes back against the idea that the Fed will act quickly, noting “right now it would be premature to start changing our calculations about raising rates,” and that while “we have a challenge right now. Inflation is high – it’s eye-popping – and it catches people’s attention and it hurts their pocketbook…the issue is that we still have Covid.”

November 15 – Barkin (Richmond president) asks for patience, saying that “it's very helpful for us to have a few more months to evaluate, is inflation going to come back tomore normal levels? Is the labor market going to open up?” and “I think it's helpful to have some time to see where reality is in thiseconomy” before rates are raised.

More Hawkish, You Say?

Even though Fed officials have continued to strike a dovish tone by all accounts, rates markets are taking a different perspective on the matter altogether. In fact, rates markets are now discounting a more hawkish Federal Reserve over the coming years – more hawkish than at any other point in 2021.

We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below showcases the difference in borrowing costs – the spread – for the December 2021 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (December 2021-December 2023) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: Daily Timeframe (January 2021 to November 2021) (Chart1)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

As has been the case for several weeks now, continually elevated Eurodollar spreads alongside action in the US yield are consistent with the 2013/2014 period that suggests a more hawkish Fed is soon to arrive – even if the narrative being pedaled by FOMC officials is quite different.

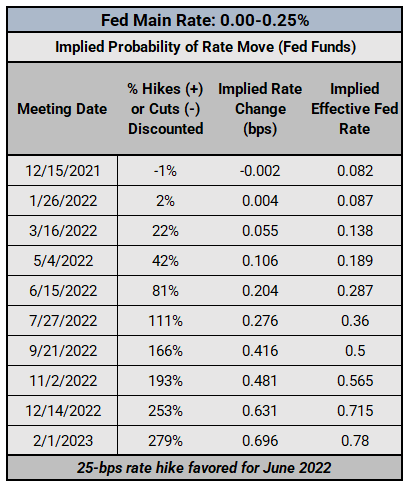

There are 143.25-bps of rate hikes (that’s five 25-bps rate hikes plus a 73% chance of a sixth hike) discounted through the end of 2023 while the 2s5s10s butterfly recently reached its widest spread since the Fed taper talk began in June (and its widest spread of all of 2021).

Federal Reserve Interest Rate Expectations: Fed Funds Futures (November 16, 2021) (Table 1)

Rate hike expectations remain quite elevated through mid-November, holding onto their gains from October and rebounding from their dip after the November Fed meeting. Earlier this month, ahead of the November Fed meeting. Fed funds futures were discounting an 81% chance of a 25-bps rate hike in June 2022 – and that’s exactly where they remain today. This remains the most hawkish that rates markets have been since the start of the pandemic.

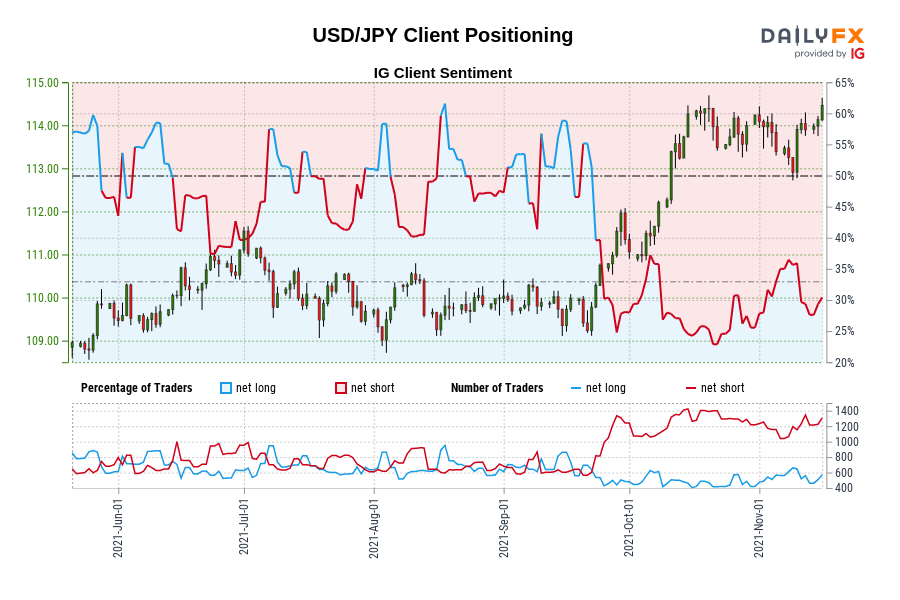

IG Client Sentiment Index: USD/JPY Rate Forecast (November 16, 2021) (Chart 2)

USD/JPY: Retail trader data shows 29.74% of traders are net-long with the ratio of traders short to long at 2.36 to 1. The number of traders net-long is 2.71% lower than yesterday and 15.01% lower from last week, while the number of traders net-short is 3.42% lower than yesterday and 10.71% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise.

Positioning is less net-short than yesterday but more net-short from last week. The combination of current sentiment and recent changes gives us a further mixed USD/JPY trading bias.

--- Written by Christopher Vecchio, CFA, Senior Strategist