Central Bank Watch Overview:

- The tone around the early-October theme strengthened over the course of the month: inflation pressures may not be so transitory after all

- Eurodollar contract spreads and the US Treasury yield curve are offering their strongest hints thus far that a more hawkish Fed is about to arrive.

- Fed rate hike odds are discounting five rate hikes through the end of 2023, with a 49% chance for six 25-bps rate hikes altogether.

On the Cusp of a More Hawkish FOMC

In this edition of Central Bank Watch, we’ll review comments and speeches made by various Federal Reserve policymakers in mid-October prior to the pre-meeting communications blackout window going into effect. The tone around the early-October theme strengthened over the course of the month: inflation pressures may not be so transitory after all, and that could require an immediate reduction in asset purchases which would continue at a brisk pace in the first half of 2022.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Taper Announcement a Done Deal

The 3Q’21 US GDP report may have proved disappointing in some respects, but not enough to have dissuaded policymakers that it’s now time to taper. Throughout October, several Fed policymakers suggested that they believe “substantial progress” has been achieved, and in context of persistently higher inflation pressures, that tapering should begin as soon as possible.

October 13 – September FOMC meeting minutes summarized that “participants noted that if a decision to begin tapering purchases occurred at the next meeting, the process of tapering could commence with the monthly purchase calendars beginning in either mid-November or mid-December.”

October 14 – Bullard (St. Louis president) commented on elevated inflation readings, noting that “while [he does] think there is some probability that this will naturally dissipate over the next six months, [he] wouldn’t say that’s such a strong case that we can count on it.”

Harker (Philadelphia president) said that it was time to start tapering, noting that he is “in the camp that believes it will soon be time to begin slowly and methodically -- frankly, boringly -- taper our $120 billion in monthly purchases of Treasury bills and mortgage- backed securities.”

October 19 – Barkin (Richmond president) suggested that US labor markets remain tight, observing that “we are hearing employers revising policies like drug testing, providing more in-house training, and reviewing hiring criteria to ensure relevant prior experience, when appropriate, can be recognized in place of a degree.”

Waller (Fed governor) said that “while there is still room to improve on the employment leg of our mandate, [he] believe[s] we have made enough progress such that tapering of our asset purchases should commence following our next FOMC meeting, which is in two weeks.” Furthermore, he noted that he believes “the pace of continued improvement in the labor market will be gradual, and [he] expect[s] inflation will moderate, which means liftoff is still some time off.”

October 20 – The Beige Book is released and says that while the US economy grew at a “modest to moderate rate” recently, persistent supply chain issues, labor issues, and delta variant concerns were weighing on growth prospects.

October 22 – Waller commented that if inflation expectations remain elevated, “we would have to be much more aggressive in our policy stance in 2022 than [he] was expecting.”

Williams (NY president) suggested that the changes in inflation during the pandemic have been atypical, noting that price pressures have seen a “very unique set of circumstances” over the past 18-months.

Rates Suggest an Even More Hawkish FOMC

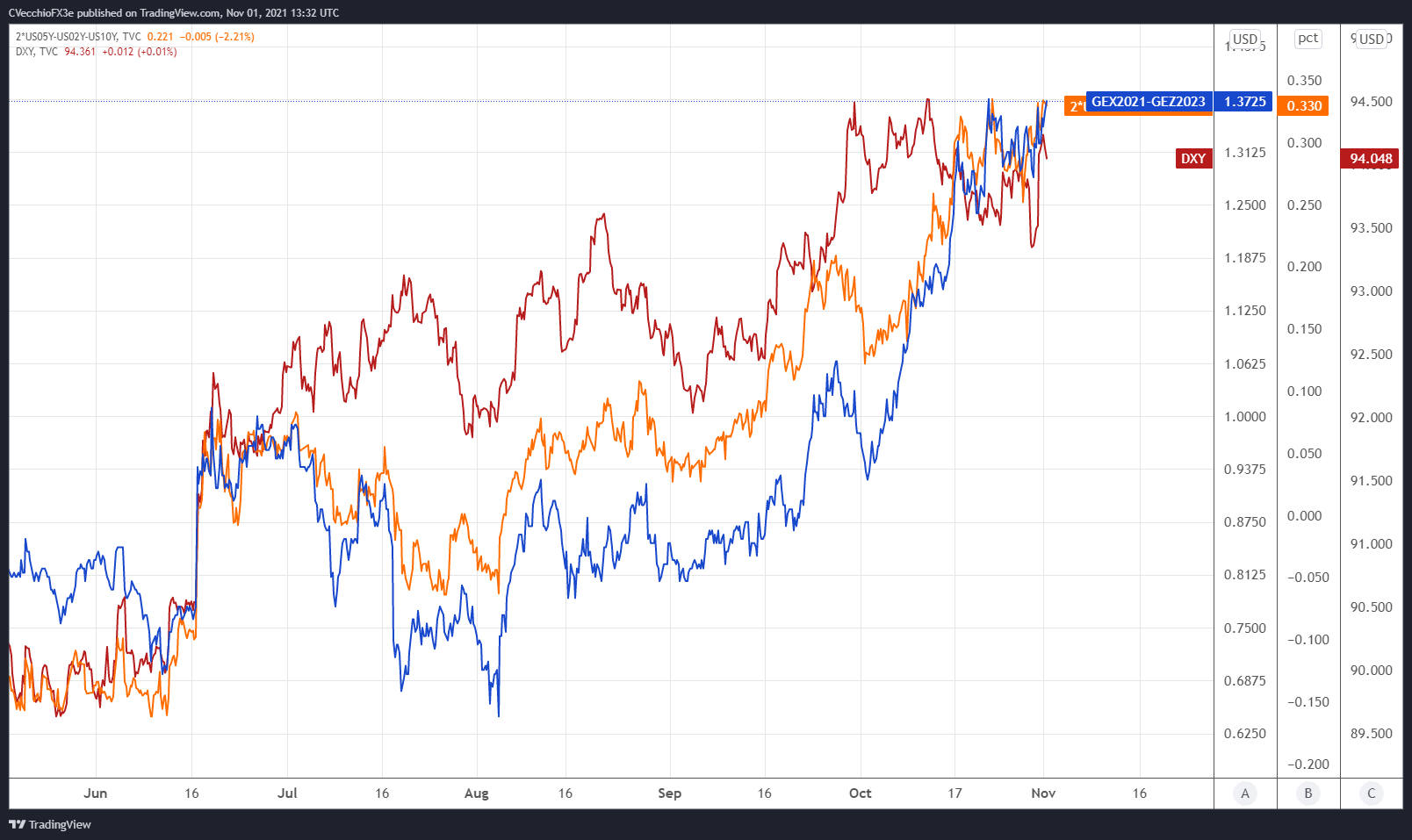

We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below showcases the difference in borrowing costs – the spread – for the November 2021 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (November 2021-December 2023) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: 4-hour Timeframe (May 2021 to November 2021) (Chart1)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

As has been the case for several weeks now, continually elevated Eurodollar spreads alongside action in the US yield are consistent with the 2013/2014 period that suggests a more hawkish Fed is soon to arrive.

There are 137.25-bps of rate hikes (that’s five 25-bps rate hikes plus a 49% chance of a sixth hike) discounted through the end of 2023 while the 2s5s10s butterfly recently reached its widest spread since the Fed taper talk began in June (and its widest spread of all of 2021).

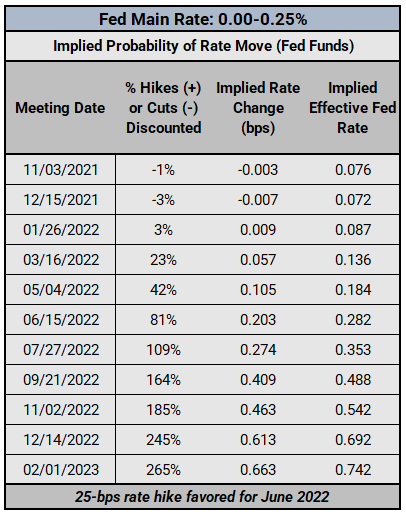

Federal Reserve Interest Rate Expectations: Fed Funds Futures (November 1, 2021) (Table 1)

Rate hike expectations escalated dramatically throughout October. At the start of last month, roughly two weeks removed from the September Fed meeting, markets were in a 104% chance of the first hike in December 2022; that’s a 100% chance of a 25-bps hike and a 4% chance of a 50-bps hike. Now, at the start of November, Fed funds futures are discounting an 81% chance of a 25-bps rate hike in June 2022. This is far and away the most hawkish that rates markets have been since the start of the pandemic.

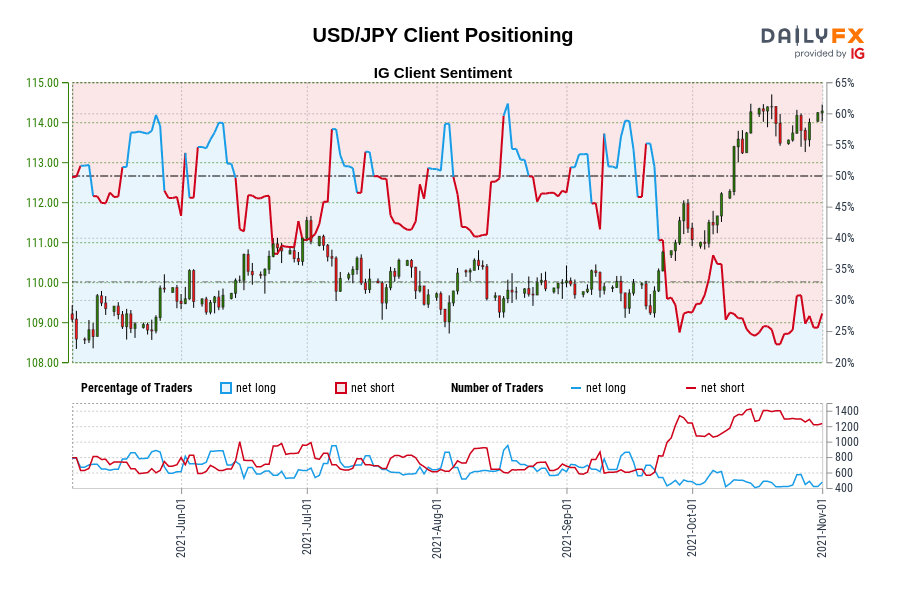

IG Client Sentiment Index: USD/JPY Rate Forecast (November 1, 2021) (Chart 2)

USD/JPY: Retail trader data shows 29.69% of traders are net-long with the ratio of traders short to long at 2.37 to 1. The number of traders net-long is 24.64% higher than yesterday and 13.02% higher from last week, while the number of traders net-short is 1.31% higher than yesterday and 10.32% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise.

Yet traders are less net-short than yesterday and compared with last week. Recent changes in sentiment warn that the current USD/JPY price trend may soon reverse lower despite the fact traders remain net-short.

--- Written by Christopher Vecchio, CFA, Senior Strategist