US Dollar, Singapore Dollar, Thai Baht, Indonesian Rupiah, Indian Rupee, ASEAN, Fundamental Analysis – Talking Points

- US Dollar aimed mostly higher against ASEAN currencies last week

- Weakness in Chinese and Emerging Market equities fueling volatility

- Key event risk: Chinese PMI, Fed ending SLR exemptions and NFPs

US Dollar ASEAN Weekly Recap

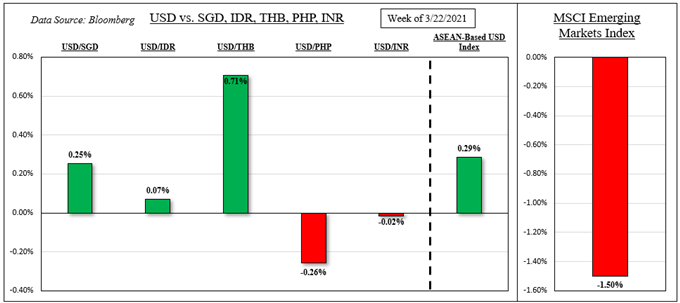

The haven-linked US Dollar aimed cautiously higher against its ASEAN counterparts this past week, gaining 0.25% and 0.71% against the Singapore Dollar and Thai Baht respectively. The Indonesian Rupiah was fairly flat while the Philippine Peso managed to appreciate slightly. This is while the MSCI Emerging Markets Index (EEM) weakened about 1.50%.

Gains in USD/THB occurred despite the Bank of Thailand leaving benchmark lending rates unchanged at 0.50%. The central bank cut the outlook for GDP due to the Covid outbreak and a fragile tourist industry. The latter is a key contributor to growth. At the same time, the Bank of Thailand left the doors opened to further monetary support. The local 10-year government bond yield weakened and remains under February peaks.

Meanwhile, the PHP’s resilience may be due to fading dovish expectations from the Philippine Central Bank. The BSP left benchmark lending rates unchanged, highlighting downside economic risks, but also reiterating that current settings remain appropriate. The local stock market index, the PSEI, gained this past week as capital inflows likely supported the Philippine Peso.

US Dollar, MSCI Emerging Markets Index– Last Week’s Performance

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

External Event Risk – Chinese Stocks, Treasury Yields, Fed, NFPs

ASEAN currencies can be quite sensitive to capital flows, influenced by overall market sentiment. While US equities mostly rose this past week, Chinese ones flirted with correction territory. China’s government has been trying to address what it thinks may be a market bubble. This is as the PBOC has been slowly tightening policy this year to keep inflation from taking off.

Meanwhile, rising longer-term Treasury rates and a stronger US Dollar have been pressuring Emerging Market equities. Albeit, the bond market appeared to stabilize this past week, halting a 7-week winning streak for the 10-year yield. This followed lackluster demand at a series of government debt auctions as Fed Chair Jerome Powell continued to highlight the risks to the economy at a testimony before a Senate panel.

Treasuries also paid little notice to slightly softer core PCE data this past Friday, which is the Fed’s preferred gauge of inflation. The central bank has been underscoring that it will likely view a near-term rise in inflation as transitory. So softer underlying prices can cool the bond market further. For that, all eyes turn to the US non-farm payrolls report. More attention may be given to average hourly earnings.

The Fed is also expected to not extend emergency SLR exemptions in the coming week, opening the door to fewer demand for Treasuries from banks. That may offer upside momentum to bond yields. As such, the US Dollar could remain elevated against its ASEAN counterparts as the latter tend to focus on external developments.

ASEAN, South Asia Event Risk – Thailand, Indonesia, Chinese Manufacturing PM

Focusing on the ASEAN economic calendar docket, Thailand and Indonesian Markit manufacturing PMI are due. Thailand will also release the next set of current account figures. Chinese manufacturing PMI may also be worth watching as the nation is a key trading partner for ASEAN members. Rosy data from the world’s second-largest economy could create positive spillovers to neighboring nations.

Check out the DailyFX Economic Calendar for ASEAN and global data updates!

On March 26th, the 20-day rolling correlation coefficient between my ASEAN-based US Dollar index and the MSCI Emerging Markets index changed to -0.74 from -0.82 one week ago. Values closer to -1 indicate an increasingly inverse relationship, though it is important to recognize that correlation does not imply causation.

ASEAN-Based USD Index Versus EEM and Treasury Yields – Daily Chart

Chart Created Using TradingView

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

-- Written by Daniel Dubrovsky, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter