US Dollar, Singapore Dollar, Thai Baht, Indonesian Rupiah, Indian Rupee, ASEAN, Fundamental Analysis – Talking Points

- US Dollar strengthened against most of its ASEAN counterparts

- Longer-term Treasury rates may continue uptrend, boosting USD

- Watch for BoC, ECB commentary on bonds. INR eyeing CPI print

US Dollar ASEAN Weekly Recap

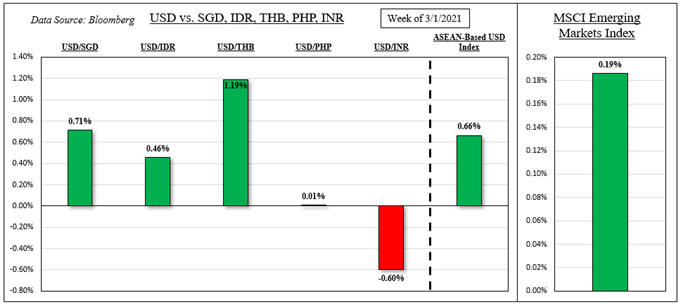

The haven-linked US Dollar mostly outperformed its ASEAN counterparts this past week, climbing against the Singapore Dollar, Indonesian Rupiah and Thai Baht. This is as rising longer-term Treasury yields continued fueling portfolio reallocation into value-oriented stocks as growth ones underperformed. Taking a look at developing markets generally, the MSCI Emerging Markets Index was relatively flat for the week.

Rising rates in the US are likely fueling gains in the Greenback, but there were a couple of notable exceptions within ASEAN and neighboring countries. The Philippine Peso held its ground as net foreign stock investment outflows slowed and the local central bank saw recent inflationary pressures as temporary. In India, the Rupee outperformed the US Dollar. Capital flows were positive as the Nifty 50 gained 2.81% this past week.

US Dollar, MSCI Emerging Markets Index– Last Week’s Performance

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

External Event Risk – All About Longer-Term Treasury Rates

Rising US longer-term rates remain a key risk for ASEAN currencies for a couple of reasons. The first is that it makes forgoing bonds for stocks increasingly more expensive, requiring higher returns from the latter to compensate. This can direct investment capital away from riskier investments, such as those in Emerging Markets. The second is that this dynamic can induce bursts of market volatility, favoring the anti-risk USD.

Commentary from Fed Chair Jerome Powell this past week seemed to show that the central bank is relatively sanguine about the bond market for the time being. As such, yields could continue climbing, especially as data from the world’s largest economy outperforms economists’ expectations. This has been the case recently, according to the Citi Surprise Economic Index.

Last week’s non-farm payrolls report underscored this dynamic. While average hourly earnings were in-line with expectations, the country added 379k positions in February versus 200k anticipated as the unemployment rate surprisingly fell to 6.2% from 6.3%. Combine this with the anticipated US$1.9 trillion Covid relief package and a subsequently-expected infrastructure bill, longer-term Treasury rates could continue rising.

It will be interesting to see how the Bank of Canada and European Central Bank will approach rising yields. Both central banks will have their latest interest rate announcements this week. Their actions could reverberate outwards. As for US economic data, CPI will cross the wires on Wednesday. A softer-than-expected print could cool the bond market. Then on Friday, consumer sentiment will cross the wires.

ASEAN, South Asia Event Risk – Philippine Unemployment, Indian CPI & Industrial Production

Focusing on the ASEAN economic docket, it will be a relatively light one. Philippine unemployment data and trade balance are due. But, USD/PHP will likely spend most of its time focusing on external events. USD/INR will be awaiting local CPI and industrial production data on Friday. A softer print from inflation risks cooling rising RBI rate hike bets looking a year out, opening the door to a push higher in USD/INR.

Check out the DailyFX Economic Calendar for ASEAN and global data updates!

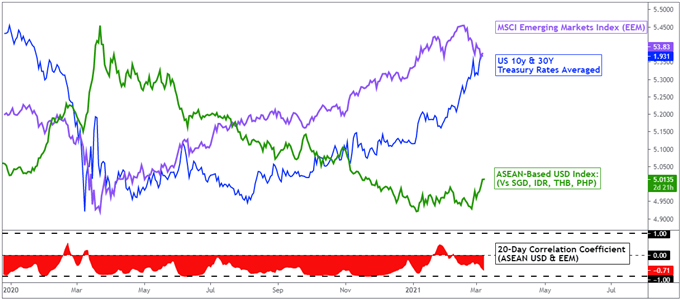

On March 5th, the 20-day rolling correlation coefficient between my ASEAN-based US Dollar index and the MSCI Emerging Markets index changed to -0.71 from -0.43 one week ago. Values closer to -1 indicate an increasingly inverse relationship, though it is important to recognize that correlation does not imply causation.

ASEAN-Based USD Index Versus ASEAN ETF Index and Treasury Yields – Daily Chart

Chart Created Using TradingView

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

-- Written by Daniel Dubrovsky, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter