Trade Wars, US-China Relationship, EU-US Trade Relations Talking Points:

- US-led trade wars with China and the EU likely to continue under Trump administration

- Multi-layered geopolitical issues not pertaining to trade may spill into trade discussions

- Biden administration may ease tensions with EU but less incentive to relieve China pressure

Donald Trump Becomes President

Doubling Down on China

If re-elected, President Donald Trump would likely double down on China and seek additional concessions through “Phase 2” of their long-awaited, comprehensive trade agreement. While “Phase 1” was signed, the coronavirus pandemic complicated what was an already-fragile situation. Domestic demand was hammered and as a result, China was unable to hold up its end of the bargain.

10 Key Dates in US-China Trade War Timeline

- January 22, 2018: US tariffs all imported washing machines and solar panels (not just from China)

- March 8, 2018: US orders 25% tariff on steel imports, 10% tariff on aluminum

- April 2, 2018: China imposes tariffs of up to 25% on 128 US products

- August 7, 2018: US posts list of $16 billion of Chinese goods to be taxed at 25%. China retaliates with 25% duties on $16 billion of US goods

- December 1, 2018: China and US agree to 90-day ceasefire, both sides talk to discuss resolution

- May 5,2019: After trade talks failed, Trump tweets intent to raise tariffs on $200b of Chinese goods to 25% on May 10

- August 1, 2019: US-China trade talks failed at G20, Trump announces 10% tariff on $300b of Chinese imports

- August 5, 2019: China halts US agricultural purchases, USD/CNY breaks past 7.000 exchange rate

- September 20, 2019: After 2-day meeting, USTR announces tariff exclusions on 400 Chinese products

- October 11, 2019: Trump announces Phase 1 deal. It is officially signed on January 15, 2020

There are an additional +30 key dates worthy of accounting, but the most recent developments at the time of writing are listed in this article.

Furthermore, reconciliation is made even more difficult based on different accounting methods both the US and China employ. Not entirely by coincidence, each sides’ approach favor their respective positions. Mr. Trump’s pivot towards greater leniency in the trade war in late 2020 may have been the result of a practical maneuver to avoid stirring economic and financial turbulence ahead of the election.

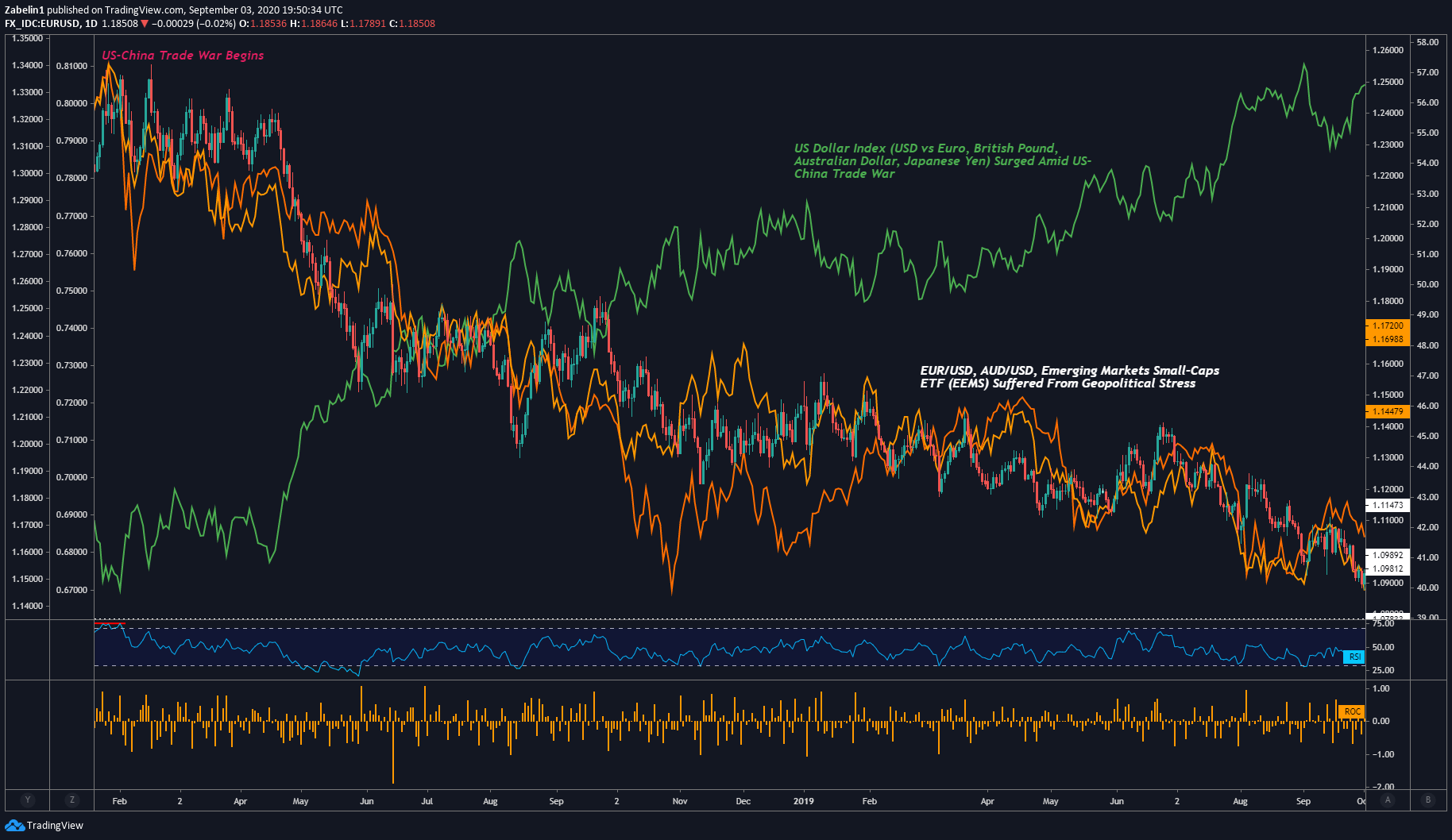

Impact of US-China Trade War on Foreign Exchange Markets – Daily Chart

Source: TradingView

Having said that, if re-elected, the President would likely revive pressure on China alongside an aggressive pursuit for the ratification of “Phase 2”. This may also occur in tandem with the diplomatic strains with Beijing over the sweeping national security bill for Hong Kong that has drawn international criticism. Growing tension over that geopolitical hot spot could spill over into trade talks like it did in 2019.

Another hot-button issue that may rattle stocks and cycle-sensitive assets are issues pertaining to China-based technology software. Controversy over TikTok, WeChat and Huawei’s 5G installations continue to be sticking points in cross-Pacific relations and will only likely be amplified under a Trump administration. The restriction of technology exports to Huawei has led China to start creating a plan to develop its own semi-conductors.

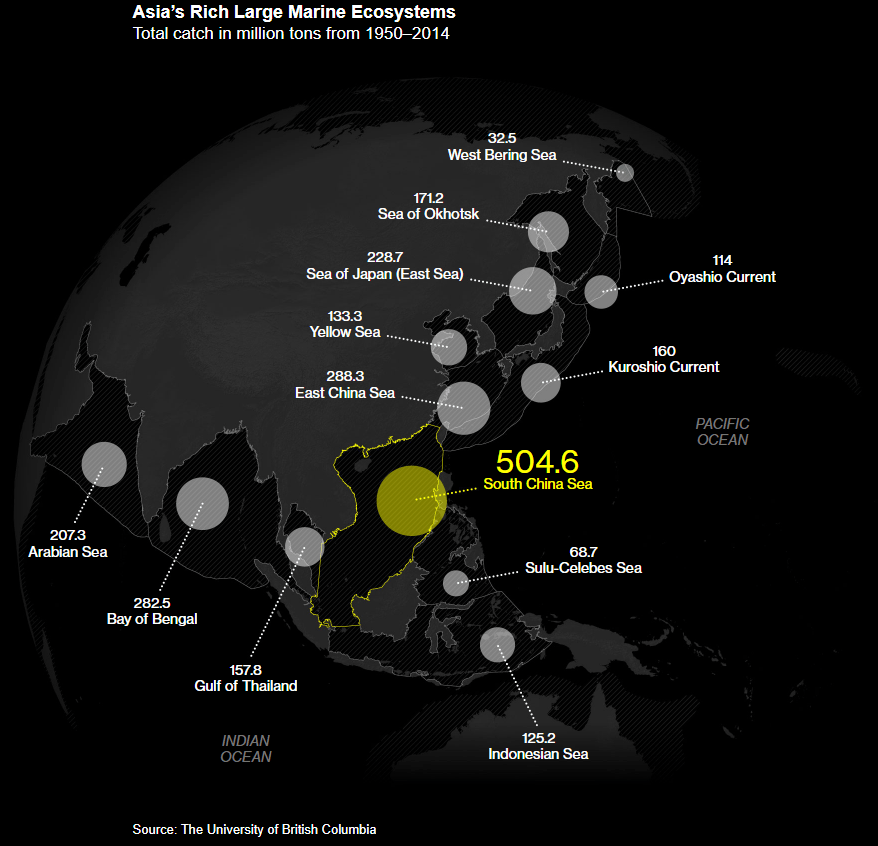

Political stress in the South China Sea over Beijing’s military and economic activities have also intensified US-China relations. In addition to island-building and base constructions, the Asian giant’s aggressive claim to strategic fisheries has further created regional discontent with Vietnam, Taiwan and the Philippines to name a few. The Trump administration’s stronger stance against China could raise the risk of a head-on conflict – though this is still a relatively low probability.

The South China Sea: A Fisherman’s Utopian Dystopia

Source: Bloomberg using image by University of British Columbia

Together, these geopolitical risks could put a premium on haven-linked currencies like the US Dollar and anti-risk Japanese Yen but a discount on growth-anchored FX like the Australian and New Zealand Dollars. They could be particularly susceptible to deteriorating US-China tensions given their strong reliance on the latter’s robust economic performance. This dynamic may be amplified if these issues spill over into trade talks.

Open a demo FX trading account with IG and trade currencies that respond to systemic trends.

Honing in on Europe

From a market-oriented perspective, the re-election of Donald Trump could push the US Dollar higher along with the anti-risk Japanese Yen based on trade considerations discreetly. In his first term, the President not only started a trade war with China that many believe throttled global growth prospects, but his administration’s policies also fractured relations with Europe. The latter was hit with aluminum and steel tariffs with threats of additional import duties.

Arguably the most formidable tax threat against Europe – which has not yet been taken off the table – is auto tariffs. This one in particular could be economically devastating since it would directly impact Germany – the region’s largest economy and biggest car manufacturer – the hardest. Last year, Trump almost used Section 232 of the Trade Expansion Act of 1962, a Cold War-era policy measure that would have increased auto tariffs by 25%.

The European Union responded in kind by using tariffs targeted at politically-strategic states with key exports. Orange juice and bourbon were two of the many products that were hit. The former is a key export from Florida, a swing state in US elections and the latter is a signature export of Kentucky - the state of Senate Majority leader Mitch McConnell.

10 Key Dates in US-EU Trade War Timeline

- March 1, 2018: Trump announces US is preparing to impose metal tariffs

- March 3, 2018: EU plans to retaliate with politically-strategic tariffs like Bourbon and orange juice

- March 8, 2018: US orders 25% tariff on steel imports, 10% tariff on aluminum

- March 22, 2018: US gives temporary exemptions to the EU among others

- May 22, 2018: US announces in investigation on whether auto imports pose a national security threat

- June 1, 2018: EU-US trade talks fail on permanent exemption from aluminum and steel tariffs

- June 6, 2018: US imposes tariffs on EU, Europe says ready to respond with €2.8b worth of duties

- July 1, 2018: EU warns US that nearly $300b of US auto exports may be hit with tariffs

- July 25, 2018: Trump and then-EC President Junker broker a deal, metal tariffs are lifted

Note: From July 25, 2018 on, the EU and US engaged in a multiple tit-for-tat trade exchanges and threats of additional countermeasures too long to list. The most recent one is listed in the paragraph below.

An almost two-decade trade dispute with the World Trade Organization (WTO) over illegal subsidies to aircraft giants Airbus and Boeing are another force widening the US-EU rift. The most recent ruling tilted in favor of Washington, which was given the largest arbitration award in the organization’s history. It authorizes the US to legally impose $7.5 billion worth of tariffs on European goods – and Washington took it.

This came much to the chagrin of EU policymakers who were hoping to reach a tariff-free resolution. In mid-August, Washington said it would keep a 15% tariff on Airbus and a 25% tariff on other European goods. Brussels is now waiting to hit back with its own tariffs should it be afforded WTO approval for illegal US subsidies to aeronautical giant Boeing.

Diverging foreign policy approaches in the Middle East – specifically towards Iran – may also add another layer of geopolitical tension that hinders cross-Atlantic cooperation. After Trump backed out of the 2015 nuclear deal and re-imposed sanctions on Iran, EU policymakers scrambled to find ways to incentivize Iran to stick to the agreement. This came much to the disdain of key officials in the Trump administration.

European officials created what is known as the Instrument in Support of Trade Exchanges (INSTEX). This special purpose vehicle (SPV) allows European firms to circumvent US sanctions by facilitating non-SWIFT and non-US Dollar denominated trade with Iran. Washington warned that such an action could result in the sanctioning of EU firms, but Brussels made it clear that such policies could result in tariffs on US firms.

Joe Biden Becomes President

Lighter Pressure on China

Given what Democratic nominee Joe Biden and his running mate Kamala Harris have said in the election cycle, it appears their approach to China on trade will have a lighter touch. Mr. Biden said that “America’s farmers have been crushed by [Trump]’s tariff war with China”. Harris echoed this sentiment, saying that the economic conflict was “punishing American consumers [and] killing American jobs”.

Having said that, the removal of tariffs may come with strings attached. In order to avoid being labeled as ‘soft on China’, especially with Beijing’s national security bill in Hong Kong, Biden may also have to stand up to the Asian giant. In addition to growing tension in the South China Sea, he may have to leverage alleviating pressure on trade in exchange for strategic geopolitical concessions in the aforementioned areas.

The prospect of reconciliation - or at least not escalating tension - could boost market sentiment and help restore confidence in the gradual restoration of international trade norms, a considerable contribution to global growth. Cross-continental equity markets would likely rally from this prospect along with growth-anchored currencies like the Australian and New Zealand Dollars. The anti-risk Japanese Yen and US Dollar, however, may not thrive in this environment.

Reconciling With Europe

In line with Biden’s comparatively more conventional approach to policy, cross-Atlantic reconciliation would likely be high on the agenda. Repealing the $7.5 billion worth of tariffs on European products and general normalization of bilateral trade relations could be one part of a broader multi-pronged effort to restore fractured relations. This could help lift equities but undercut demand for havens like the US Dollar.

Having said that, Biden may encounter some friction with EU policymakers on issues pertaining to digital sovereignty, through perhaps to a lesser degree than what Trump has faced. In 2019, France almost signed into a law a digital tax that appeared to overwhelmingly target US firms. The Trump administration fell back on their modus operandi and subsequently threatened to impose tariffs if the bill became law.

The so-called GAFA group – Google, Apple, Facebook and Amazon – have also had run-ins with EU lawmakers. What a resolution under Biden’s administration would look like is unclear, but what is almost certain is the expectation of continued tension between EU officials and US tech giants. Uncertainty here may hurt technology stocks, but the ripple effect may be comparatively smaller than if Trump were to deal with it.

--- Written by Zabelin, Currency Analyst for DailyFX.com

To contact Dimitri, use the comments section below or @ZabelinDimitri on Twitter