Talking Points:

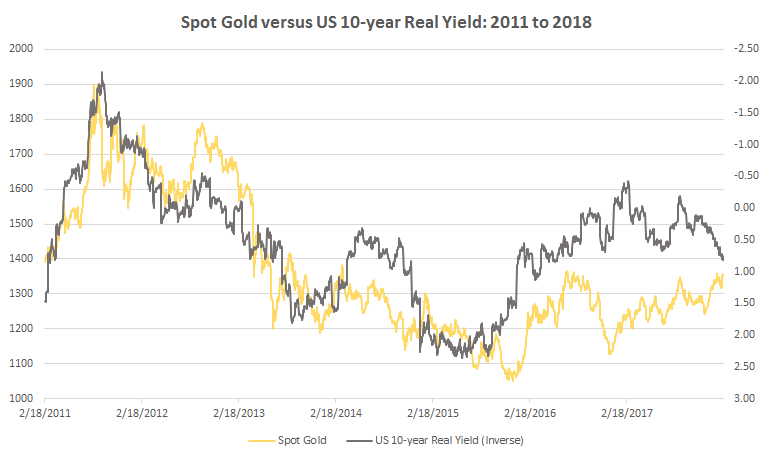

- Gold tracked US 10-year real yields from 2011 until 2017, but then the relationship began to erode.

- In recent months, the historical relationship has turned upsidedown, suggesting that new influences are driving demand for Gold.

- Rising yields may reflect rising political risk, not additional premia for inflation protection.

See our longer-term forecasts for Gold, the US Dollar, among others, with the DailyFX Trading Guides

Like other commodities, supply and demand play a role in the price of Gold. But unlike other commodities, even other precious metals like silver (electrical appliances, superconductors, batteries) and platinum (automobile production inputs), gold has few if any industrial uses on a widespread scale.

As such, rather than consumption playing the primary driver for gold prices, saving and disposal are the central factors. When we mean ‘saving and disposal,’ we mean reasons like as a hedge against inflation, a safe haven during times of market duress and geopolitical stress, or as an alternative to fiat currencies during periods of low or negative interest rates. Currently, a mix of these factors are driving Gold’s push higher.

Interest Rates Play a Dominant Factor in Gold’s Appeal

Real yields are inflation-adjusted yields: in this case, the US Treasury 10-year yield minus the headline inflation rate. Why does this matter? Investing is all about asset allocation and risk-adjusted returns. On the asset allocation side, it’s about achieving required returns given the investor’s wants and needs.

If inflation expectations are rapidly increasing, you would expect to see fixed income underperform: the returns are fixed, after all. Why would you want to have a fixed return when prices are increasing? On a real basis, your returns would be lower than otherwise intended.

Price Chart 1: Spot Gold versus US 10-year Real Yield Daily Timeframe (February 2011 to 2018)

For example, let’s say the US Treasury 10-year yield is currently 2.5% and headline inflation is 2%. The nominal interest rate is 2.5%, and the real interest rate is 0.5%. Then all of the sudden if inflation shoots up to 4.5% while US yields held steady, the real interest rate would move to -2%.

Falling US real yields means that the spread between Treasury yields and inflation rates are decreasing. If Gold yields nothing, has an estimated cost of carry of -2.4%, and only can return capital appreciation, it would best suited to rally when US real yields fell.

That is, gold’s appeal as an inflation hedge relative to the US Dollar increases not in an environment when inflation is just rising, but when inflation is rising and nominal interest rates are not rising at the same pace; or in sum when US real interest rates are dropping.

What Explains the Recent Divergence?

Something changed in recent months, however: the historical relationship between Gold and real yields has broken down. Even as real yields are rising – an environment that one would expect to be poor for precious metals – Gold has been able to advance. This may be another piece of evidence of a regime change across asset classes.

Price Chart 2: Spot Gold versus US 10-year Real Yield Daily Timeframe (February 2016 to 2018)

The National Bureau of Economic Research says that regime change is "the tendency of financial markets to often change their behavior abruptly and the phenomenon that the new behavior of financial variables often persists for several periods after such a change."

In the case of the the separation between Gold and real yields, it's rather apparent that behavior has changed abruptly - especially since the passage of the tax reform bill in Q4'17. Thus explains the divergence and Gold’s appeal: given the trajectory of the US deficit and debt, another US rating's downgrade this year seems very possible.

Read more: Central Bank Weekly: US Dollar Could Care Less about a March Hike

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist

To contact Christopher Vecchio, e-mail cvecchio@dailyfx.com

Follow him on Twitter at @CVecchioFX

To be added to Christopher's e-mail distribution list, please fill out this form