Hedge Fund Advisor, Julian Brigden Key Points on Global Macro Strategy:

- The path to becoming a living legend in global macro investing

- Why trading FX & precious metals are a great way to cut your teeth in global investing - the new norm

- How inflation may play out to the surprise of everyone, even the Fed

- Why watching the dollar could be the smartest move you make

- What asset class could become more important in the next economic cycle

- The potential new investing landscape after ‘RIP Corporate Capitalism’

- Access Julian's treasured insights here through the trading year at 25% off through April 30

Listen to the full podcast here: iTunes or Stitcher

Source: Twitter

Source: RealVision

Introducing Julian Brigden of MacroIntelligence2

When Julian Brigden speaks, the biggest names in the market listen, and often they take notes. Julian has command of the global macro scene in a way few do or can approach. Julian and Tyler had an in-depth conversation on an ever-expanding career in global-finance where he now leads the macroeconomic research team at Macro Intelligence 2 Partners, LLC that he co-founded in 2011 and Co-Leads Real Vision’s premium offering, Macro Insiders where he was kind enough to generate a discount code for readers.

Julian’s primary focus is helping his client exploit trading opportunities inherent in macroeconomic and policy-related markets while explaining well what may be developing around the corner with impressive clarity of logic and decades of experience to support his probable views.

This article presents the highlights of the podcast so be sure to listen to the full interview below. However, the generosity of Julian encouarged me to share more in writing than we normally do. Enjoy!

Listen to the full podcast here: iTunes or Stitcher

How a Storied Career Grows to Legendary Market Operator Status

Tyler Yell: Julian, I've long appreciated the wisdom and humility you bring to markets. Would you mind casting light over your career and sharing with us what has allowed you to grasp so much so well, while at the same time, sharing well thought out views with a refreshing degree of humility?

Julian Brigden: As you’ve said, I’ve been in the market for 30-odd years and started on a trading desk. This will date myself and attach me to many of the storied institutions who are no-longer around (though they did not always fail while I was on the desk), but I started at Drexel on the FX & Precious Metals Desk, specifically IMM currency arbitrage and bullion sales.

I believe both of those markets (FX & Precious Metals) are perfect markets to cut your macro teeth in. FX is unique in particular because you’re always looking to two-sides of every trade. Two sides of the equation to balance out the relative value. This gives you an inordinate degree of appreciation for all-things macro, both in terms of data, flow, and helps to create an analytical mind.

I fell in love with this, and through the years I’ve been fortunate enough to work with some great people, and some great clients who have taught me a great deal along the way. My focus has been active clients (i.e., hedge funds and large asset managers.) As a young person, this gave me great insight into how people were effectively approaching the market.

After a period in banking, I moved over to Medley Global Advisors, which was transformative as it opened up to me the world of independent research. At Medley, it because obvious to me that there was a large disconnect between policymakers and markets. They really don’t mix all that well, and at Medley, we were not able to see on the market side of the business what the policymakers were doing.

The point is that it is in the interplay between what policymakers are thinking they are going to do and how they think markets are going to react, and how markets, in fact, react that you can make (I found) quite a lot of money.

I went back into the market at Credit Agricole, I started to write my own market commentary, where I generated thoughts for my clients that led to more business for me, and really, we got quite lucky.

I found that I needed to anchor views based on longer-term macro themes. The thing we began to do differently was foregoing the needlessly complex models found at central banks, that have a ludicrous amount of assumptions to the point of nullifying their use. Rather we took a piece of data that came out today, and twisted it from multiple angles, spun it until we were able to make it correlate to something that we cared about. So, let’s say, German data, which has a million subcomponents when looked at through IFA for things like the German Leather Clothing industry, which, I don’t know where I’m going with that and for the sake the show I’ll stop there, but the point is you can drill down into this data really deeply.

When you do that, once in a while you find a nugget of valuable input that gives you further insight on key economic drivers that affect the market like German Industrial Production or German GDP. We’ve done that with about 2000-odd models. This is done to forecast economic data, markets, and we use this to anchor the view, and then I have three other professionals with me at MacroIntelligence2, and collectively we have 130+ years of market experience, and we bring together our insights from managing active, leveraged, and real money, and we try and use these insights to the benefits of our clients.

Julian’s Models Help Him See Dislocations That Lead To Opportunities

Source: Twitter.com: Julian Brigden, @JulianMI2

Building a Global Macro View When Volatility Is Historically Low

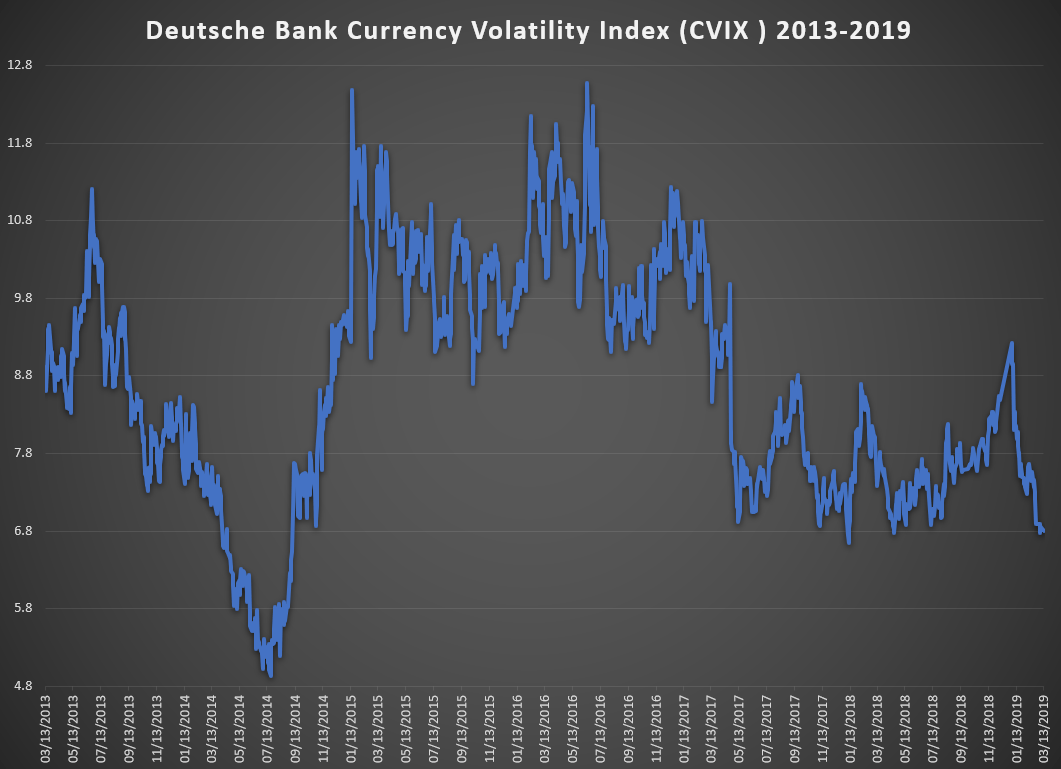

TY: You’ve spoken (quite correctly) about the dismal state of FX markets due to the FX Volatility ‘valley of death’ that we seem to be in now. I’m showing FX Implied Vol per the DB CVIX at 6.87 right above the Jan 2018 low before the risk heart attack, and below that the lowest since 2014 when the world was awoken with a cold shower by the Fed signaling hikes that caused the Dollar to rocket higher. As a trader, investor, and hedge fund consultant, how do you manage in these periods? Is it to look at the big picture, find tactical opportunities or something else altogether?

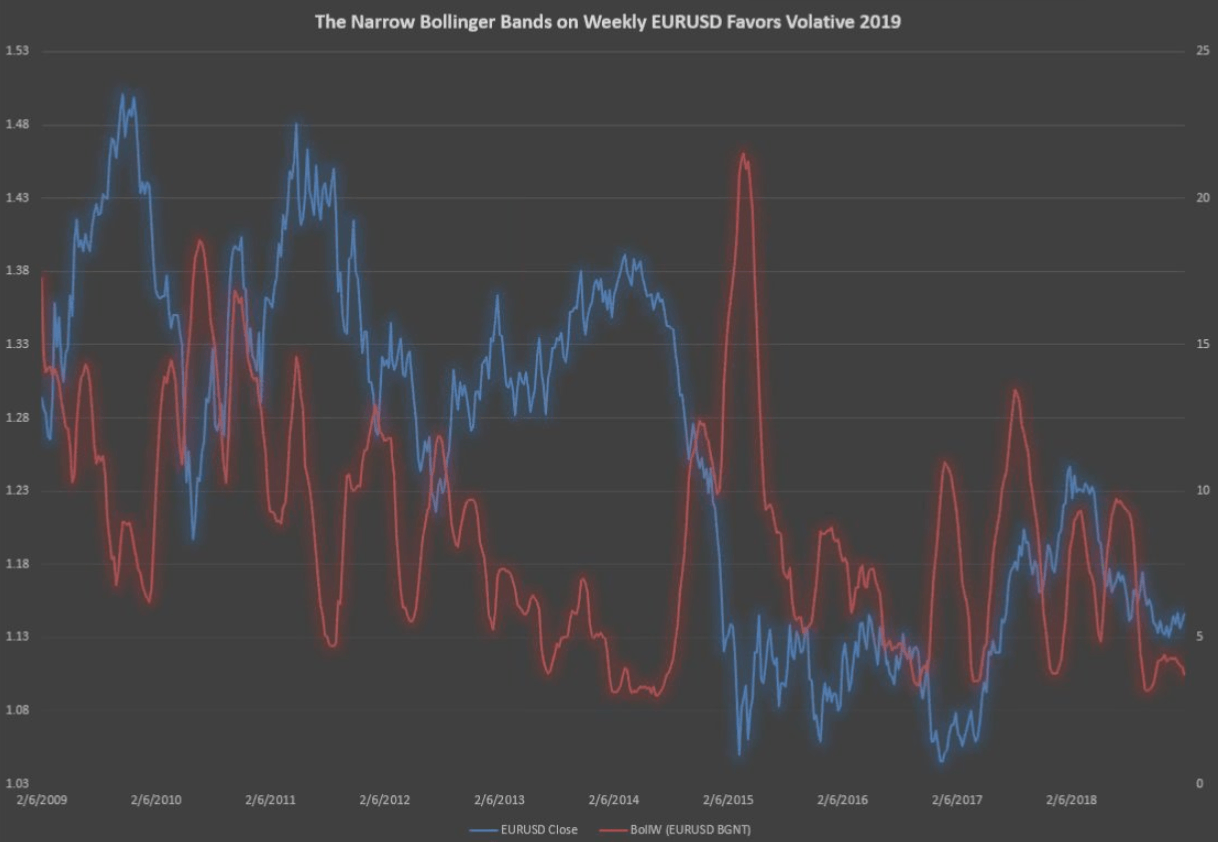

JB: Yeah, I was recently quoted on Bloomberg where they shared an insight I gave to clients about the EUR/USD Bollinger Band Width. This is one metric of volatility as you can also pull Implied or Realized Vol for a currency pair. EUR/USD itself saw such a tight band on the weekly chart that you had to go back to 1977 with the implied EUR to find a comparable period.

Even for an old git like me, I was a wee boy in my trading career in those days, and it makes for an incredibly frustrating trading environment. And traders have to be aware of the temptation that arises in times of low volatility with the flexibility to trade multiple markets to step away.

Those traders are often best served by stepping away. Focus your time and energy on other assets. While that's necessary to generate P/L, but it can also be dangerous and a mistake because when you fully take eyes off the markets, you can miss big moves.

A Broad View of FX Volatility From Deutsche Bank’s CVIX

Data Source: Bloomberg, Deutsche Bank

My approach is to enhance discipline and structure from a trading perspective. This is not the time to take massive bets. This is the time when you should have a very clear trading view to set realistic targets given the level of volatility, and very firm stops. More importantly, stick to the stops.

Volatility Is Low Now But That Often Precedes High Volatility Trading

Data source: Bloomberg

If I could verbalize possibly one of the biggest lessons, I learned that was physically painful to receive, that I got in my second week of trading at Drexel. I was on the desk, and my boss came over to me. He asked what I thought about DEM/USD (German Deutsche Mark to US Dollar). I told him that I thought it was going up.

He said, “Okay, where is it going to and where is your stop?” I said that I think it’s going to 80 and my stop is 10. He said okay go buy ten lots and then left. So I did.

He came back half an hour later, and he asked me, “so, where is it?”

I said, “Ah, it’s 90 below the figure.” He said, “okay, but did you take the stop?”

I told him “no” at which point I got slapped physically across the forehead with the comment, Trading is all about discipline, you take your losses and you run your profits.

That has always stuck with me, and I believe it’s precisely at times of low volatility that you have to go back to those fundamentals from a trading perspective.

From a consulting perspective, this is when I’m looking for opportunities because periods of super low volatility do not last. If you go back to the late-70s, it was relatively quickly that we saw a very sharp decline in the US Dollar. The point is that low volatility preceded a very active period.

We’re looking at, what are the facts behind this low vol, and what are the factors or signals that could shift us out of such a regime?

Can You Afford Not To Watch The US Dollar?

TY: When you look at the current market (March 2019), and we have such low currency volatility with the dollar as strong as it is compared to the last two times of low FX volatility, it’s hard not to be concerned with high volatility in FX alongside and aggressively strong dollar and the negative global market ramifications that could have.

JB: I think you’re absolutely right. You know, we’ve been very big US Dollar bulls. Clients of our institutional produce and Macro Insiders know this. I’ve been a steadfast bull. Right here right now, I’m a bit uncertain due to December.

As the equity markets cratered into the end of 2018, I was anticipating the typical pattern we see where capital gets scared and floods out of EM and riskier assets and piles into the US Dollar, which sees a blow-off top in the US Dollar. This often leads to massive Fed panic, and they bring out all the weapons to support risk sentiment and weaken the US Dollar, and often that markets a US Dollar top.

Such USD strength tends to bring a sharp sell-off that can bring wonderful buying opportunities for investors. But you look at the US Dollar through the risk route of 2018 and the USD didn’t budge. It didn’t move at all in Q4. I think the reason it didn’t move, which I discussed with my clients about how China and the US have agreed to some type of US Dollar cap. This is to prevent too much US Dollar strength. I’m concerned that this leads to abnormally low US Dollar volatility that could prevent the opportunities that often arise in market regime shifts.

We might get it, though at the moment we do not have signs of it. Instead, we may be slipping into a downward move on the US Dollar. We never get the final rush up in USD that leads to a bunch of distressed assets at great prices, and we’ll just slide into an extended period of US dollar weakness.

When I look at typical cycles, we seem to be entering into a stage where US Dollar weakness develops.

The Dollar Will Likely Be The Answer To The Next Cycle

TY: When I look at the current market (March 2019) it seems to me that the market needs, and I hate to use the word ‘needs,’ but for risk sentiment recovery it seems to me the world needs a weaker dollar for a global risk sentiment recovery. But, if something happens, and we see a cold shower similar to 2014 and the US Dollar pops higher, it could be very painful indeed.

JB: Look, I would see that as just a great opportunity to buy. That type of environment where US Dollar pops higher tends to freak out central banks. I agree with you. In October, we got very bearish on risky assets, and then on January 1, I wrote a piece to my clients titled ‘First Blood.’ I noted that it was time to take profits on their short trades as this sell-off is likely done, and we’re looking now to the reflationary wave similar to 2016 when Janet balked, and all the central banks cobbled together to reinstall confidence in global capital markets.

The big difference is that in 2016 the US Dollar then dropped quite hard, and this time it has not. I believe there are some very clear reasons why, but it makes me cynical about the Q1 2019 risk rally. I think in the last few days, there have been assets that should have done exceedingly well, think Precious Metals, that started to fade, and the missing element seems to be the US Dollar weakness.

It’s very difficult to see a concrete risk rally where the US Dollar is not weak.

Growth Is The Axis That This Market Spins Upon

TY: Seeing the US Dollar as the rudder on the risk sentiment ship of global investing, but recently, Jeff Gundlach noted the Corporate Bonds are ground zero for the next crisis due to leverage ratios and the likelihood that CBs have few, if any bullets left in their monetary canon, and what may be in there could be blanks. Are you focused on corporate debt or something else when you look at the horizon?

JB: Sure.Firstly, I saw the same interview, and I would not compare myself to someone of Jeffrey Gundlach’s record, I do think we share a handful of similar views even though we come to those views from different routes.

There is no question that corporate debt is a vast, huge scary, scary thing. I’ve had clients from very huge mutual funds that they can all see their peers in other big mutual funds and their corporate debt holdings and when they look at the liquidity provided from the market, and it’s a concern. The market liquidity has imploded from where it was a pre-financial crisis. Mutual Fund holdings of corporate debt are 40-50X higher vs. liquidity provided than before pre-GFC. They know, they will not be able to get out of it, and they’re just looking around thinking that they hope they’re the first ones out and hoping that others don’t run for the door because that will kill the market.

I’ve talked to plenty of people who’ve said that you could see major mutual funds gating or closing for redemptions their funds in that type of event. While cognizant of the risks, to me, the collapse of the credit market is a second derivative.

Rather, everything hinges on growth and liquidity story, and at that nominal growth or growth plus inflation. It’s only if and when growth falters that we’ll find problems in corporate credit. As long as the cash flow is coming in, and this has been the post-financial crisis and the post-QE lesson that as long as there is plenty of cash filling the system, you can keep the whole thing afloat.

It’s when the cash gets tight, and when the growth falters that you get the singular, and you start to look around and wonder which green bottle is going to fall on the wall. This is where our focus lies. It’s looking at the growth story and the pricing dynamics of assets and trying to figure out when an issue arises.

TY: That’s excellent. Looking at growth as that primary factor makes a lot of sense to be a cornerstone. I remember one time reading a research piece that was discussing why China has the fixed growth targets they do. The argument was that they have to reach their set targets to have a chance to get out of the “middle-class” trap and a failure to hit those growth targets would bring a whole host of other negative issues to the Chinese economy. I think you can transfer this lesson beyond China that growth is the only way to thread the needle.

JB: Right, and I would stress that when we discuss growth, we’re looking at nominal growth. That’s real growth plus inflation. That’s key. I think that is the key thing going forward which will determine if we can get out of this or not.

The Fed Have Potentially Trapped Themselves In An Equity Corner

TY: So that brings me to my next question, Charles Goodhart once stated that "When a measure becomes a target, it ceases to be a good measure." This has become known as Goodhart’s law. Funny enough, it seems to be the case that presidents and chairpersons of central banks see their respective benchmarks or currencies as targets instead of measures. What markets or stress measures do you look to that helps you see if pain or pleasure is most likely on the investor’s horizon?

JB: These days, increasingly, when it comes to pain or pleasure or risk-on and risk-off it now all seems to come down to the US Equity market. For that, we look to positioning data or technical.

There are key measures like volatility, but one that is overlooked is a correlation. When looking to the correlation of sectors, it’s important because it’s a driver of performance in the Long/Short equity space.

What I think is key is that in terms of stress, you tend to see correlations rise alongside volatility. If you look at it as a Long/Short equity guy and correlations rise from 40% to 80%, then your whole strategy is falling apart.

If that gets stressed with equity volatility, then fund managers end up in a state of panic in a hurry. This is something we watch quite closely. The other thing frankly is to watch the macro to figure out when the central banks are going to ease or tighten.

One reason why we’ve been bearish on equities is that we’ve been looking at what the central banks have been doing, and I know in conversations I’ve had with policy related friends, and they’re struggling with this. The Fed sees the heightened correlation of the Fed’s Balance Sheet and asset prices. And now, the Fed thinks it is important because the market thinks it is important and there you can see the feedback loop. They don’t care as much about the correlation as they do about how much the market cares about the correlation.

The reality is that if you look at a broad metric of US equities like the Value Line Geometric Index that takes 1,600 equally weighted stocks and look to the correlations between stocks and the Fed Balance Sheet at the peak of QE1, QE2, & QE3, at the cycle high the correlation between the Fed Balance Sheet and the equity index was near 90%.

In Quantitative Tightening (QT) or Balance Sheet Run Off, the correlation hit that same level, but as stocks were moving lower. So, what the hell do they expect? The expression we use to clients is that they’ve created a crack addict who knows they are utterly beholden.

Recently, I was lucky enough to have dinner with an ex-Fed chairman, and I said to him, what are you going to do? You’ve inflated all these asset prices, and the minute you stop inflating the asset prices they drop. When we look at our models, the correlations show weakening equity prices also hurt employment as well as capital expenditures (i.e., company growth projects) and weak GDP.

We’ve gotten to the point now where even if the SPX500 trades sideways for the next 10-years, which would be a fortunate outcome given the sharp rise from 2009, you’re going to see a lot of cost cutting in terms of jobs, projects based on the way the CEOs are compensated as they’ve become shepherds of an equity price. Not necessarily to produce a thing, but simply to keep the equity price in check. But as soon as the price stops rising, they’re cutting costs, jobs, capex.

In that world, you’d be lucky to generate 1.5% GDP growth. It’s truly frightening. I’m looking at this thing now, and I think, ‘I know the Fed likes to think of themselves as tough, and that they’ll be able just to slow QT,’ but I don’t know if people get it.

They’ve talked very dovish, which I call cooing, but they haven’t been that dovish. They’re still removing balance sheet, and all the inclinations and everything we hear in the market is that ‘they’re slowing, but they’ll keep reducing.

Here’s the problem, if investors and companies that are beholden to the stock prices to hire and grow and push up wages are likened to crack addicts who need another hit, slowing the tightening is not enough. They need more. The Fed has got to ease, or the market will be a fit, and I think the current Q1 2019 risk rally environment is not going to be sustainable without a major dovish turn (i.e., more easing) by the Fed.

Inflation & Growth in Light of the Fed Balance Sheet

Source: Bloomberg

Have Investor’s Become Addicted to Fed Policy?

TY: That reminds me of a Dick Fisher (former Dallas Fed President) interview on CNBC in 2014 where he said (after he left the Fed) that they basically pumped the markets full of cocaine and heroin.

JB: That was the best! You’ve got to love Texans. They are straight shooters. I refer to that interview on many occasions. I remember the British guy on CNBC being floored. They seemingly tried to reel him in, and say, ‘what about the wealth effect?’ or ‘weren’t you trying to suppress yields? Fisher looked at them and said, ‘no. It was always about the equity market.’ Brilliant interview.

TY: I remember [Dick Fisher] flippantly saying, ‘we’re going to see a 20-30% correction in markets when they have to find a new equilibrium,’ and I think there is something to that.

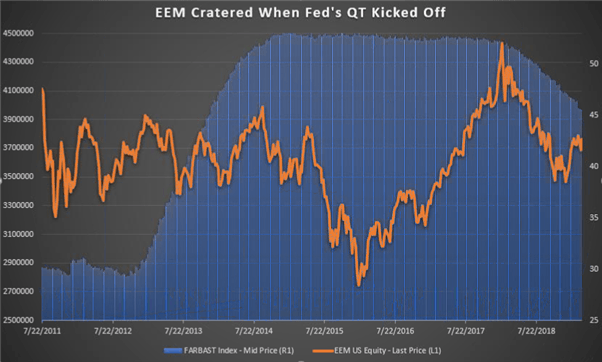

JB: Yes, I mean, look at Emerging Markets. When did EEM (iShares MSCI Emerging Market ETF) peak? It peaked when the Fed began to drain liquidity from the system. Emerging markets are doubly affected by QT because they mainly produce commodities that are priced in dollars and they borrow in dollars because their capital markets locally are typically not deep enough for the growth.

Emerging Markets Look To Fed’s Balance Sheet For Support

Data source: Bloomberg, Federal Reserve

For all of the bullishness that we’ve seen on CNBC since the end of last year, the growth has been rather derisory. I think the reason is that we haven’t seen the Fed ease yet, there are still winding down the balance sheet and draining liquidity from the system. That is almost certainly why we haven’t seen the US Dollar slip yet.

Using Commodities, EMFX To Frame Your Global Macro Strategy View

TY: So, how do you frame or utilize commodities, and emerging market currencies or bonds to help build a global investing framework at any given time?

JB: I see them as beneficiaries or fall-out from the US Dollar cycle. If you look at 2016, Janet Yellen comes out at the beginning of the year after the Renminbi devaluation scares the market. All the central bankers are in Davos, Switzerland in January, sitting around and drink a bit too much and think, ‘Oh, Jesus, we have to reflate this thing.’ And they do.

Global Elite Unite In Davos

Source: World Economic Forum

Janet (Yellen) stops hiking, every other central banker comes out with comments, and immediately the US Dollar starts to decline. At that time, the Crude Oil market takes off; Emerging Market Debt does well, Precious Metals do well. Either way, it was so bloody predictable.

It set you up to some superb trades in the second half of the year because you had a falling US Dollar and rising oil that is a recipe for inflation and specific bond market trades. The bond market has to have its feet set in reality, unlike the equity market. So, the bond market is sitting there saying, ‘the data is horrible’ since data is lagging while the central banks are easing through the data, but then you get to the middle of the year, and our models showed inflation is about to be a problem and that inflation would accelerate.

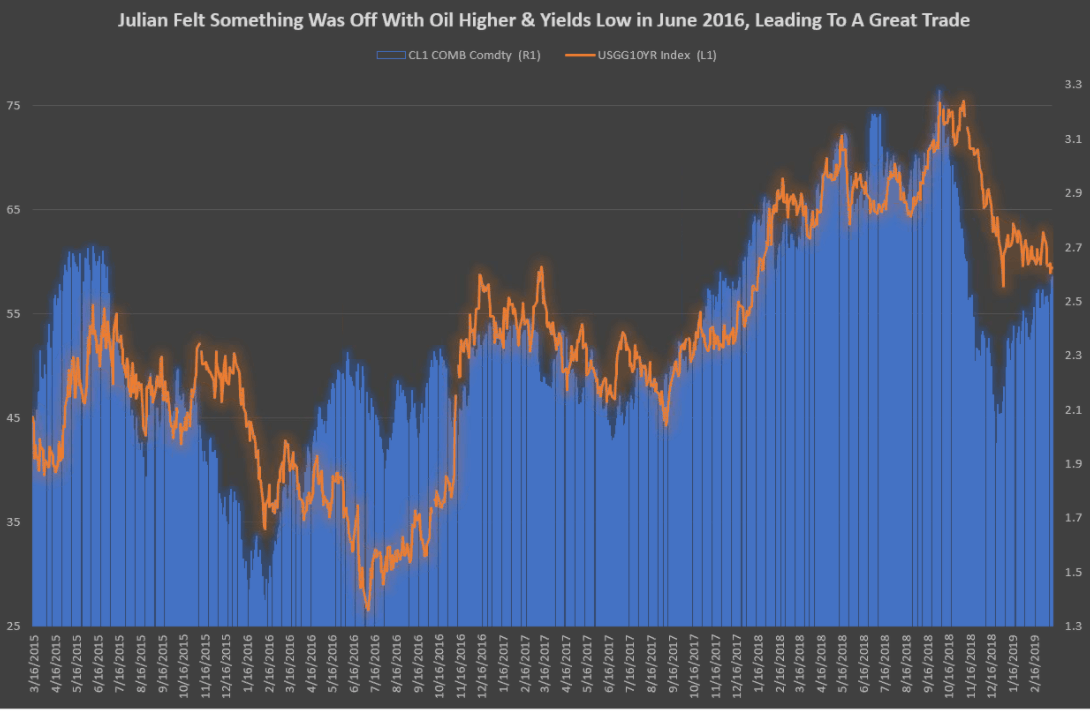

Crude Oil Bottomed When The Central Bankers Turned Against USD

Data Source: IG UK Price Feed on ProRealTime Charting

For us, oil is a key driver in inflation and its rate of change with a few tweaks here and there. However, all our factors were beginning to accelerate while traders were continuing to buy bonds, which do well in a disinflationary period.

So, we got to July, and when the US 10Yr yield hit 1.318% in July (indicating traders were afraid of growth and inflation), we told our clients, ‘that’s it, short them’ because yields are going much higher because this inflation thing is coming out, and it was such an amazingly easy trade because this is what reflation is all about.

I think if the Fed is going to do it again, we’ll likely repeat the same pattern (oil higher, us dollar lower, and yields reversing aggressively higher). The big difference is that we will not be starting with CPI at 0%, we’re staring with CPI at 1.5-2% meaning it will be a lot more dangerous for them to play a reflation game, which I think ultimately, they’ll have to or we’ll slip back into a recession. However, they are going to have a much harder time to fix it nowthan they did back then.

Sometimes The Market Shows Massive Disconnects in Correlations

Data source: Bloomberg

Inflation Can Come Quick, Will the Fed Have the Will to Stop It?

TY: You’ve long discussed with rare clarity in our world about inflation. When looking to central banks, it appears that they have chosen to worship a false god in inflation. Pity them. I’ve long been drawn to your insights on inflation pressures and factors that seem to be building whether through China (exported inflation), commodities, sovereign yields, or metals. Looking into 2019, do you see the inflation picture changing at all, or as the German bund yields are doing, do you see the slope of hope continuing to fall for CBs?

JB: First, I think you need to step back and sort out deflation vs. disinflation. We’ve arguably lived in a disinflationary environment for centuries. Since common land was distributed more appropriately in the 1500s in the UK. Prices have fallen steadily since then, while productivity has risen steadily. However, deflation and disinflation are very different.

Lucky for us, the Bank of England keeps bizarrely wonderful records, and they’ve charted over 500 years of inflation. They noticed that you would often see in the data these brief periods of inflation spikes of around 7-8 years. During these times, you will see an aggressive jump in inflation. I think that is precisely what we could be on the cusp of now.

Central bankers are always backward looking and fighting the last battle. Their view is understandable given their distaste and concern around deflation. They see deflation as something worth fighting because of its relative danger and inflation as something worth pursuing since they believe they have the tools to fight inflation (rates, balance sheet tightening, etc.)

An ancillary problem is whether or not they have the will to deliver or utilize the tools. Why didn’t they use the tools to choke off inflation in 1966-67. They didn’t then, they panicked, and inflation got out of hand ten years later in the late 1970s. People often forget pre-1965 that inflation went nowhere. Then five years later, we went from 1.6% in 1965 CPI to 5.8% in 1969. Four years! How does this happen? You get behind the curve, and you get reluctant while at the same time fiscal spending takes hold.

Then, you start to look at what happens if the US Dollar starts to fall. If you see a 4-5 year 10-15% correction on the US

Dollar. Inflation increases could compound.

Look At Inflation Through The Eyes of History

Data: Bloomberg

What’s impressive to me is the inflation we have had given the correlation to the US Dollar and US CPI as inflation. I think the US Dollar strength we have had is due to US President Trump goosing the heck out of the economy.

If you throw in a weak US Dollar, the Fed could get rapidly behind the curve.

Now, I see inflation as partly our salvation for inequality that has divided the US between baby boomers and millennials. Baby boomers need to see their savings and income eviscerated, and millennials need real wage inflation so that they can buy their homes, bonds, or equities at discounted prices.

Central bankers are kidding themselves if they think it will be easy to fight this. The cycle has changed I believe. I see 2016 as the low (in yields and inflation), we currently have a temporary inflation correction, and then we get the next cycle of inflation. What traders need to watch out for is if this new cycle of higher inflation begins with yields at 2.25% and moves higher or wherever then we’re likely going through the last high and on through to the other side.

Are Big-Tech’s / FANG's Best Days in The Rear View Mirror?

TY: FANG market cap rose 300% from 2014 to mid-2018, and after the Q4 route, there has been a retracement at 61.8% of the drop. Do you think the love affair with FANG is still ongoing, ending, or over, and if so, why, and what could that mean?

JB: FANG’s were some of our favorite shorts in September of last year. We flagged NFLX, NVDA. However, it was for no other reason than they seem to fit the chart pattern that we call ‘classic bubble.’

I’m not out to offend anyone. It is a simple pattern recognition. I’m not poking fundamentals of any company, and with me living up a mountain, I’d be stuffed without Amazon. However, the shares of Amazon and others have reached parabolic proportions. The stocks became froth frenzies separated from reality where there is greed that we saw into September and October fears.

You need to understand about FANGS is that as growth stocks, they grow when money is super cheap. They grow when they chew through your cash and can issue debt at incredibly low costs like Tesla or Netflix. I love the line from Barron’s Alan Abelson who said, “As financing becomes more expensive, when these companies who have gorged on debt and rely on that debt to keep going, it’s going to become less salubrious.”

That for me is why we saw the stocks correct last year. Now, after the bounce, it’s a difficult call, but bigger picture is a clearer view where we are, but tactically (next few weeks to months) it’s tougher to say if Netflix charges higher, break through the highs and we negate the current ‘bull trap set up’ where we fail here and crash to new lows that’s all difficult to say.

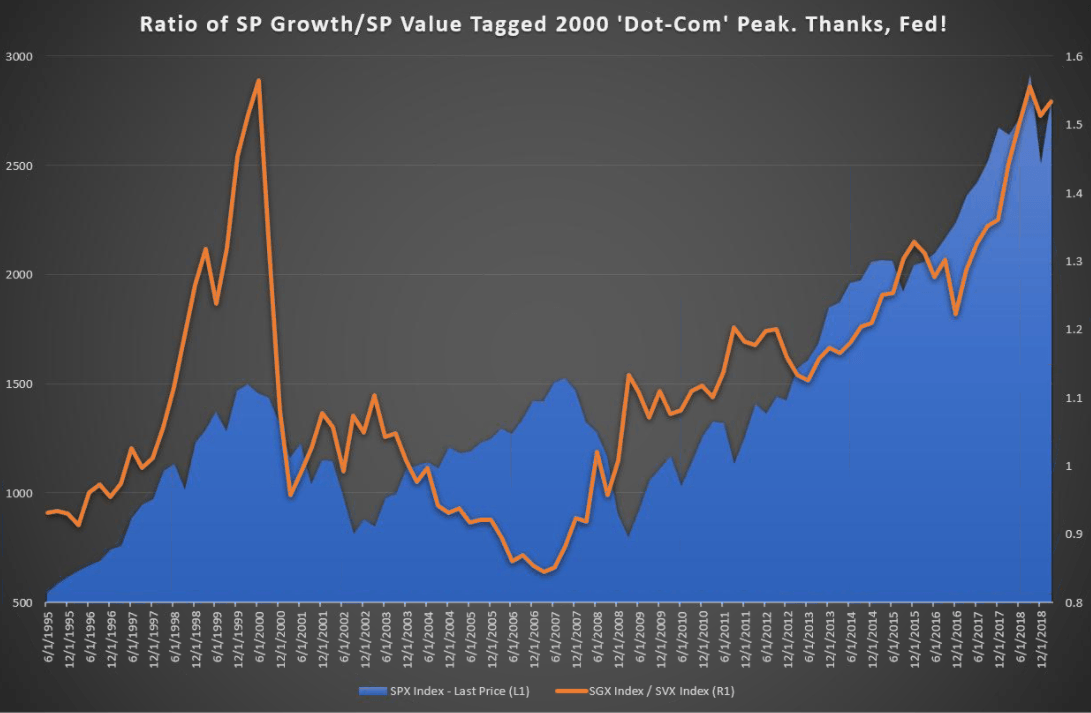

As I look out over multiple years, and I pit growth vs. value, and we have a chart we shared with our clients, where we show that the multiple of S&P growth and value metrics that we just pinged in October.

Well Done, Fed! You’ve Pushed Multiples Back To 2000 Extremes

Source: Bloomberg

It’s not going to be easy for the Fed to get themselves out of this one. The FANGs have recently recovered due to rotations. The data doesn’t seem to support the valuation, but if we go back to ultra-easy policy, these valuations could extend.

In June 2000, when the Fed held after the snap back, and growth tried to retry the highs, but growth ultimately failed. I am not sure whether or not we’re going back to the ultra-easy environment. If the Fed eases again, you would likely see the long end come under a lot of pressure, which would lift the price of capital and increase the hurdle for them to grow.

I have a hard time seeing them be the leaders again like they were over the past 3-5 years. They’re doing well now as the Fed coos and talks dovish. One of my bigger themes is that the environment is turning against them.

This to me suggests we’re unlikely to see new highs across the board in the FANGS. I’m more focused on value, and I’m particularly focused on companies that will have pricing power in a higher inflation environment.

I do think it pays to be realistic and anticipates the central bankers will intervene again. Extremes for individual assets remain important. Central Bank liquidity does not have to go into specific assets. They can go into bonds as we’ve seen in Germany & Japan.

This makes me look to who will benefit in the next flood of liquidity while seeing what assets are out of whack. I think that precious metals could be a benefactor.

RIP Corporate Capitalism, The Potential Shifting Plates Beneath Us

TY: Lastly, you’ve put together 2-part piece for some of your premium clients titled, RIP Corporate Capitalism. The supporting factors of your thesis are going mainstream with the likes of AOC, De Blasio, et al. hitting the Overton Window of acceptable thought as you put it.

You argue that investors could continually see building cross-currents for corporate profits going forward due to the political divide of populism. Coming full circle, this globalization in search of ever-higher profits and stock prices seems to be a factor in falling inflation, and as a result, a declining middle class. If stocks are no longer THE Asset to build your portfolio around should these issues come to roost, what or where do you see (in knowing you do not have a crystal ball) as the cornerstone assets of the future?

JB: We typically do not write big-picture think pieces. We did in early 2016 on the inflation cycle where we thought a new inflationary cycle could be upon us.

Recently, in late last summer, we found that the China-US trade spat that was lying in plain view. You could look at the Council of Foreign Relations and other insights that showed that Military and Economic conflict could come to a head. We put together some of the ‘common sense’ views we hold, and within weeks, things started to unfold, and people looked at us like we knew something special when we were just putting pieces together as we saw them coming developing.

Well, we wrote a similar piece called, RIP corporate capitalism. We thought from the angle of The Fourth Turning or the Kondratieff wave; they show that we should be approaching the end of a cycle in 2021-2022. The end of the cycles tend to be super volatile and can see wars or revolutions, let’s hope we avoid that and maybe the central bank balance sheet can help us avoid that.

To my mind, as a true Thatcherist (Thatcher believed in the primacy of competition and a free market and possessed a fundamental distrust of the power of government) we are coming to the end of our run. We are about to hit a tipping point in global capitalism.

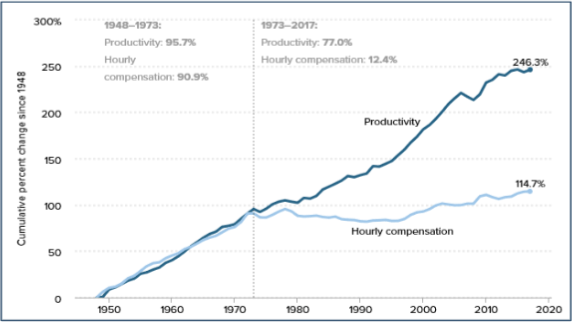

This would mean that the trends that Ronald Reagan and Margaret Thatcher originated in the early 1980s, which I served handily, of deregulation and globalization, which has taken the share, and this struck me, but the share of GDP by corporates from 1945-1989 never exceeded 2.5 times that of labor to recently 5x that of labor. That is purely unsustainable.

Who Took My (Potential) Income?

Source: Economic Policy Institute, Chart sourced from RIP Corporate Capitalism

The mirror image is the share of GDP by worker compensation. It’s going to end!

My bet is we’re going to see this reapportionment of wealth, which we see happening in the piece where you get from AOC (Alexandria Ocasio-Cortez) and the like favoring higher taxes and likely wealth taxes, the reposition of anti-trust regulations as well as de-globalization, which is linked to China.

We’ve told our clients we’re likely looking to an economy similar to pre-cold war. If you would’ve asked a company in the mid-80s before the fall of the Berlin Wall to build a factory in the Soviet Union, they would have looked at you like you lived on Mars!

This idea we had that we had a liberal, free, de-regulated and globalized world has all been a function of the collapse of the Berlin Wall. If we go back, and to what we would call a ‘silicon curtain,’ a technological divide between the US & China, and between friends and allies.

Then, a lot of the benefits of globalization would soon go away. I bet that we’re going to see both a weaker US Dollar based on higher deficit spending. Trump says he’s going to boost military spending, yet the Democrats haven’t blinked! Why? Because they see the tide shifting, and they are not giving him his cuts, and they want their programs too as they head into 2020.

I see the budget for 2019-2020, and it could be as big as the recent one a few years ago, that would lead to a much weaker dollar, which is hugely inflationary.

Remember, inflation is necessary for millennials. They need higher wages. They need to start taking some of the share of GDP that has been eaten by corporations and baby boomers. Those corporations are either going to get taxed, broken up, or something may happen to stop that trend where labor’s share has been crushed from growth.

It’s politically unsupportable at this point.

When I look at wealthy baby boomers, I see them as missing the point, as it isn’t’ for them to decide as the new generation (millennials) who will be the largest voting cohort need to come through. They have utterly different aspirations than seeing the market cap of larger corporations.

You’ll likely see them move to a single-payer system (healthcare) while sticking it to the Pharma’s and their profit margins. It’s necessary.

This is NOT socialism. Socialism is the control of the means of production. The Tories in the UK has believed in health care for all for ages. Americans need to get over this. This is simply the cycle turning.

Inflation is the only thing that will allow boomers to spend and kick-start the millennials getting on with their life as they saw their parents.

From an asset perspective, it’s disastrous to be in the bond market. Looking to 1966-1969, the foothills of inflation as I see it. You had fixed income investors losing a third of their money in five years in real terms (inflation adjusted.) That’s financial repression.

That only took inflation only going to 6%. We were close to 3% relatively recently. These things are not unthinkable.

The equity market would become much more difficult. It’d become a stock pickers market. You’d have rapid nominal GDP and companies with pricing power would do phenomenal. But the passive wave that has lifted all stocks will likely not last when companies that do not have pricing power and will succumb to their debt.

Politicians are super slow to move. They get it now though. Even conservatives are starting to see the need to support the millennials, and this will bring about inflation, a weaker US Dollar, and it will shape the way you invest and the decision you make.

Things Are Changing, I Hope This Conversation Shed Some Light On How

This far sweeping interview was a delight for me to peek into the mind of a global macro strategist at the height of global investing. Julian was incredibly kind to share his views with such details and patience with me, and it also helped me to see how investing is a cyclical world where the fundamentals often determine where capital is flowing, which thankfully leads to oscillating opportunities that active traders can benefit from over time.

I hope you enjoyed this as much as I did.

Keep up to date with the latest from Julian & MI2

Catch Julian alongside Raoul Pal with Real Vision’s Premium Service, Macro Insiders at a 25% Discount!

Macro Intelligence 2 Partners, LLC

Other Helpful Resources

- Take a look at our analysts’ trading forecasts for popular markets and the top trading opportunities in 2019.

- Link previous guest show notes [Podcast] Oil Trading Strategies with Futures Trader Tracy Shuchart | Podcast

If you found this article useful, you should follow our weekly podcasts.

Whether you are looking for market analysis, trading education or interviews with well-known industry professionals, we have you covered.

Follow our podcasts on a platform that suits you:

iTunes: https://itunes.apple.com/us/podcast/trading-global-markets-decoded/id1440995971

Stitcher: https://www.stitcher.com/podcast/trading-global-markets-decoded-with-dailyfx

Soundcloud: https://soundcloud.com/user-943631370

Google Play: https://play.google.com/music/listen?u=0

Written by Tyler Yell, CMT