FX Week Ahead Overview:

- The last week of the month brings about the usual smattering of event risk from around the globe.

- The US economy will be in particular focus over the coming days, with the first Federal Reserve rate decision of the Biden presidency and the initial Q4’20 US GDP report on the docket.

- Changes in retail trader positioning suggest that the US Dollar’s recent rebound may sputter.

For the full week ahead, please visit the DailyFX Economic Calendar.

01/26 TUESDAY | 07:00 GMT | GBP Employment Change (OCT) & Unemployment Rate (NOV)

The UK economy has been plagued by the emergence of the B117 strain of COVID-19, which UK public health officials have warned is not only more transmissible, but also has a higher rate of fatality. To no surprise, with surging infection rates in the fall and UK Prime Minister Boris Johnson pushing lockdowns at the onset of winter, UK economic data is entering a dark period.

The upcoming UK jobs report, which covers various aspects of the labor market in October, November, and December, point to a grim outlook. According to a Bloomberg News survey, the UK economy lost -100K jobs in the three months through October 2020, and the unemployment rate jumped to 5.1% from 4.9%. These numbers are likely to get worse in the coming reports, and a fly in the ointment for the British Pound, which has otherwise proved resilient post-Brexit.

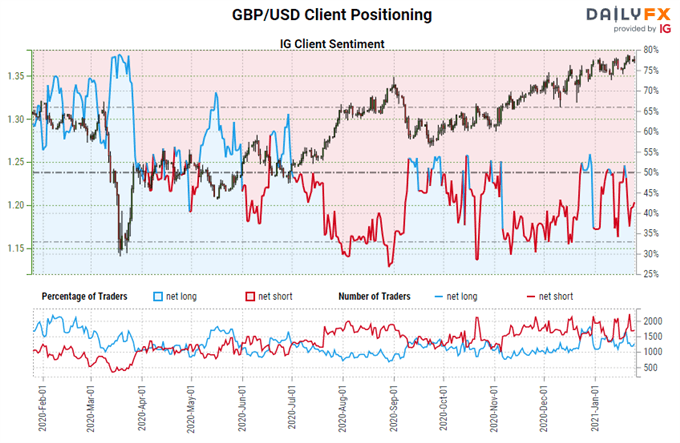

IG Client Sentiment Index: GBP/USD Rate Forecast (January 25, 2021) (Chart 1)

GBP/USD: Retail trader data shows 40.84% of traders are net-long with the ratio of traders short to long at 1.45 to 1. The number of traders net-long is 13.02% higher than yesterday and 20.65% lower from last week, while the number of traders net-short is 15.30% higher than yesterday and 32.13% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests GBP/USD prices may continue to rise.

Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger GBP/USD-bullish contrarian trading bias.

01/27 WEDNESDAY | 00:30 GMT | AUD Inflation Rate (CPI) (4Q)

Price pressures in Australia remain weak, in line with what other developed economies have been experiencing through the coronavirus pandemic. According to a Bloomberg News survey, the headline Australia inflation rate is due in at +0.7% (q/q) in 4Q’20, the same rate as in 3Q’20. The counterbalancing factors of rebounding base metal prices and a rallying Australian Dollar leave headline inflation below the lower end of Reserve Bank of Australia’s +1-3% target range. These data may be welcomed by the Reserve Bank of Australia, which has been complaining about the strength of the Aussie and its negative impact on exports.

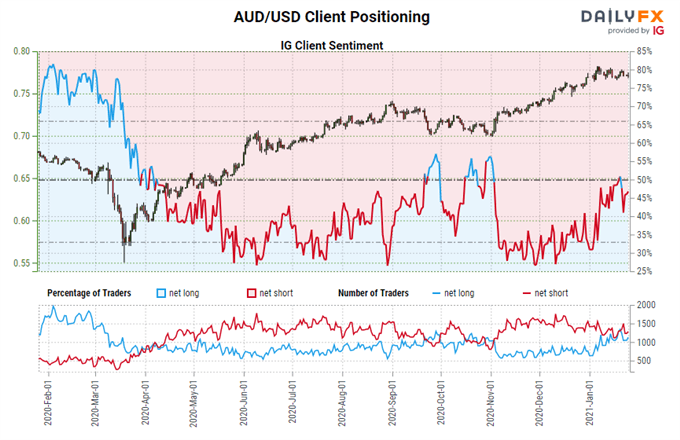

IG Client Sentiment Index: AUD/USD Rate Forecast (January 25, 2021) (Chart 2)

AUD/USD: Retail trader data shows 46.62% of traders are net-long with the ratio of traders short to long at 1.15 to 1. The number of traders net-long is 9.26% higher than yesterday and 8.70% lower from last week, while the number of traders net-short is 6.33% higher than yesterday and 1.55% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests AUD/USD prices may continue to rise.

Positioning is less net-short than yesterday but more net-short from last week. The combination of current sentiment and recent changes gives us a further mixed AUD/USD trading bias.

01/27 WEDNESDAY | 19:00 GMT | USD Federal Reserve Rate Decision & Press Conference

The week ahead is largely defined by none other than the first Federal Reserve policy meeting of the year, which should culminate in the FOMC keeping its main interest rate on hold. After much ado about a potential tapering of its QE program, Fed officials took to the airwaves in mid-January to hush a potential taper tantrum. The first meeting of the year, without a new Summary of Economic Projections, may offer little by way of tangible policy shifts to provoke volatility.

The Federal Reserve pushed back against rising expectations of a more hawkish central bank, tamping down taper tantrum concerns with a bevy of speeches in mid-January. As long as Fed Chair Jerome Powell is at the helm, the FOMC will stay the course, with the intent of keeping interest rates low through 2023. Fed funds futures are pricing in a 93% chance of no change in Fed rates in 2021. The January Fed meeting should come and go without much fanfare.

Read more: Central Bank Watch: Fed Speeches, Interest Rate Expectations Update

01/28 THURSDAY | 13:30 GMT | USD Growth Rate (GDP) (4Q)

A Bloomberg News survey is calling for US GDP to come in at +4% annualized in 4Q’20 after surging by a record +33.4% in 3Q’20. Depending upon where you look, estimates vary significantly. The New York Nowcast estimate for 4Q’20 GDP is at +2.58%, while the Atlanta Fed GDPNow model is pointing to loftier+7.5% growth.

But the fact of the matter is that Bloomberg consensus forecasts and the regional Fed bank forecasts have been coming down for the past several weeks, reflecting a deceleration in US growth as the coronavirus pandemic entered its darkest days. Even though the next tranche of US fiscal stimulus was agreed upon at the end of the Trump presidency, it is still possible that 1Q’21 US GDP comes out in negative territory (but we won’t find that out until April).

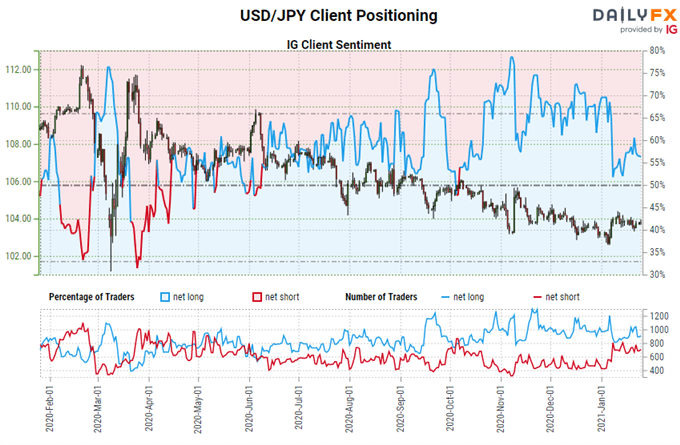

IG Client Sentiment Index: USD/JPY Rate Forecast (January 25, 2021) (Chart 3)

USD/JPY: Retail trader data shows 57.84% of traders are net-long with the ratio of traders long to short at 1.37 to 1. The number of traders net-long is 7.75% higher than yesterday and 6.26% lower from last week, while the number of traders net-short is 2.04% higher than yesterday and 3.85% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests USD/JPY prices may continue to fall.

Positioning is more net-long than yesterday but less net-long from last week. The combination of current sentiment and recent changes gives us a further mixed USD/JPY trading bias.

01/29 FRIDAY | 12:00 GMT | MXN Growth Rate (GDP) (4Q)

The Mexican economy is highly reliant on its North American trading partners, and as surging coronavirus infection rates in Canada and the United States crimped these economies, trading activity declined as the fourth quarter progressed (82% of Mexican exports go to Canada and the US, with the US accounting for 79% alone). According to a Bloomberg News survey, the Mexican economy contracted by -5.1% (y/y) in 4Q’20 after falling by -8.6% in 3Q’20. Having traded sideways for the past two months, and more recently towards the topside of its range, the upcoming Mexican GDP report may not be enough to send USD/MXN rates lower anew.

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist