US Stock Market Key Points:

- TheS&P 500, Dow, and Nasdaq 100 finish in mixed territory despite better-than-expected economic data

- Indices remain vulnerable to US yields and US dollar as the 10 year note has just set a fresh high at 3.99%

- All eyes on Friday’s PCE price index for the next piece of inflation data

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Most Read: US Dollar Trims Losses Following Better-than-Expected US Consumer Confidence Data

After yesterday's sharp sell-off in the British Pound and UK bond markets which spilled over into the US and led investors to seek refuge in safe-haven assets, the risk off sentiment continued today even with some better-than-expected economic data.

The S&P 500, the Dow and Nasdaq 100 posted losses for the fifth consecutive day yesterday. The S&P hit a new low for the year, the Dow Jones officially entered a bear market while the Nasdaq grinded on an important support area. Investor risk appetite has been on edge as rising inflation and the resulting tightening of financial conditions are inducing an economic downturn that would imply poor fundamentals for stocks.

Today, and despite a show of bullish momentum in early trading, US indices surrendered gains and remain subdued to prices surge of the US dollar and US yields that run-higher. The S&P 500 and Dow Jones lost 0.42% and 0.20% respectively. The Nasdaq 100 showed a modest gain of 0.16%.

The overall negative sentiment comes despite better-than-expected economic data today. In August, capital goods orders excluding defense and air showed a strong reading, the highest since April 2021. New home sales also surprised to the upside, perhaps as a reflection of lower home prices, but despite rising interest rates. And finally, the Richmond Fed's manufacturing index and consumer confidence in September both beat expectations.

One could suggest that good news is bad news for the stock market as it could confirm room for the FOMC to maintain their aggressive tightening cycle. Thus, seven of the eleven S&P 500 sectors posted losses. The only sector to show gains was energy. Crude Oil prices rose today from a nine-month low to $78.59 at the time of writing as supply disruptions are expected due to the impact of Hurricane Ian in the Gulf of Mexico. On the other hand, OPEC+ is expected to cut production at its next meeting on October 5 to support the price.

On another note, it was interesting to hear a new round of Fed speakers today. While the Minneapolis, Chicago, and St. Louis Fed Presidents of all expressed their commitment to fight inflation, two of them raised concerns about “over-tightening,” while the other official emphasized that the FOMC is tracking and considering the effect of dollar strength on the economy and suggested that 4.5% Fed funds might be a maximum at which the FOMC could remain for some time.

TECHNICAL OUTLOOK

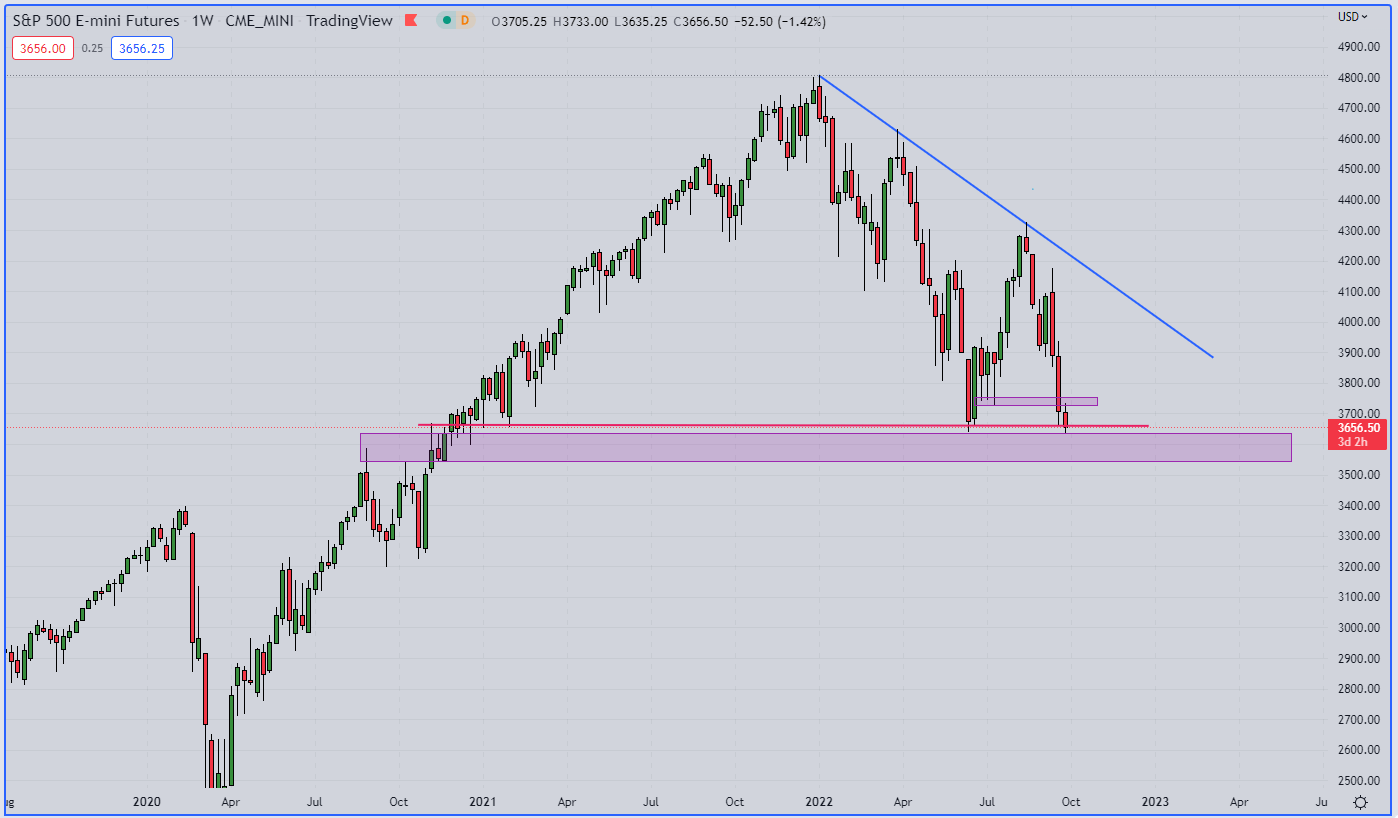

From a technical standpoint, after making a new low for the year yesterday, bears were able to push past the important support level of 3660 and it is now trading at 3655. Given that fundamentals have not changed, any move to the upside may be limited and, if volatility persists, a close below 3639 could open the door to a further fall towards 3540.

S&P 500 Mini Futures Weekly Chart

S&P 500 Mini Futures Chart. Prepared UsingTradingView

Looking ahead, the Fed’s preferred inflation measure, the PCE price index, will be released on Friday. July’s reading was 6.3% y/y up from a 6.8% in June. It will be of interest to see if a pivot is confirmed.

EDUCATION TOOLS FOR TRADERS

- Are you just getting started? Download thebeginners’ guide for FX traders

- Would you like to know more about your trading personality? Take theDailyFX quizand find out

- IG's client positioning data provides valuable information on market sentiment.Get your free guideon how to use this powerful trading indicator here.

---Written by Cecilia Sanchez-Corona, Research Team, DailyFX